Zurn Elkay trades at $50.19 and has moved in lockstep with the market. Its shares have returned 5.7% over the last six months while the S&P 500 has gained 8.9%.

Is now a good time to buy ZWS? Find out in our full research report, it’s free.

Why Does Zurn Elkay Spark Debate?

Claiming to have saved more than 30 billion gallons of water, Zurn Elkay (NYSE:ZWS) provides water management solutions to various industries.

Two Positive Attributes:

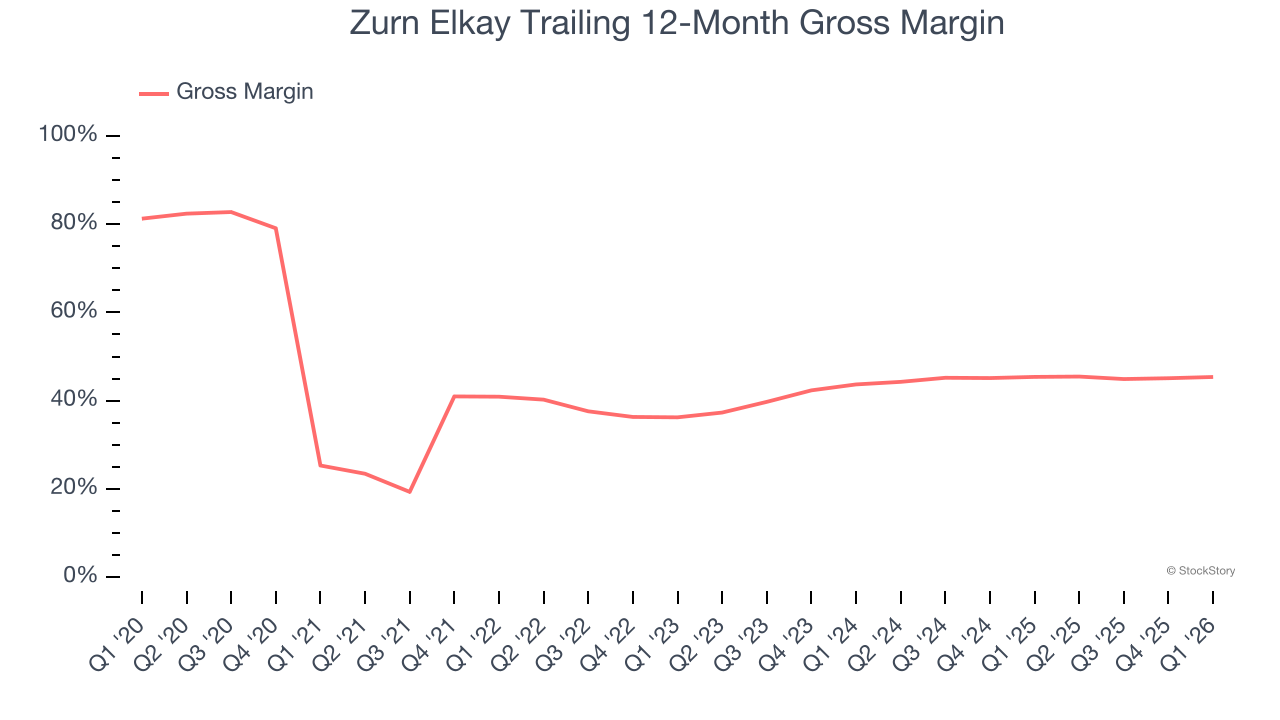

1. Elite Gross Margin Powers Best-In-Class Business Model

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

Zurn Elkay has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 42.6% gross margin over the last five years. Said differently, roughly $42.64 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

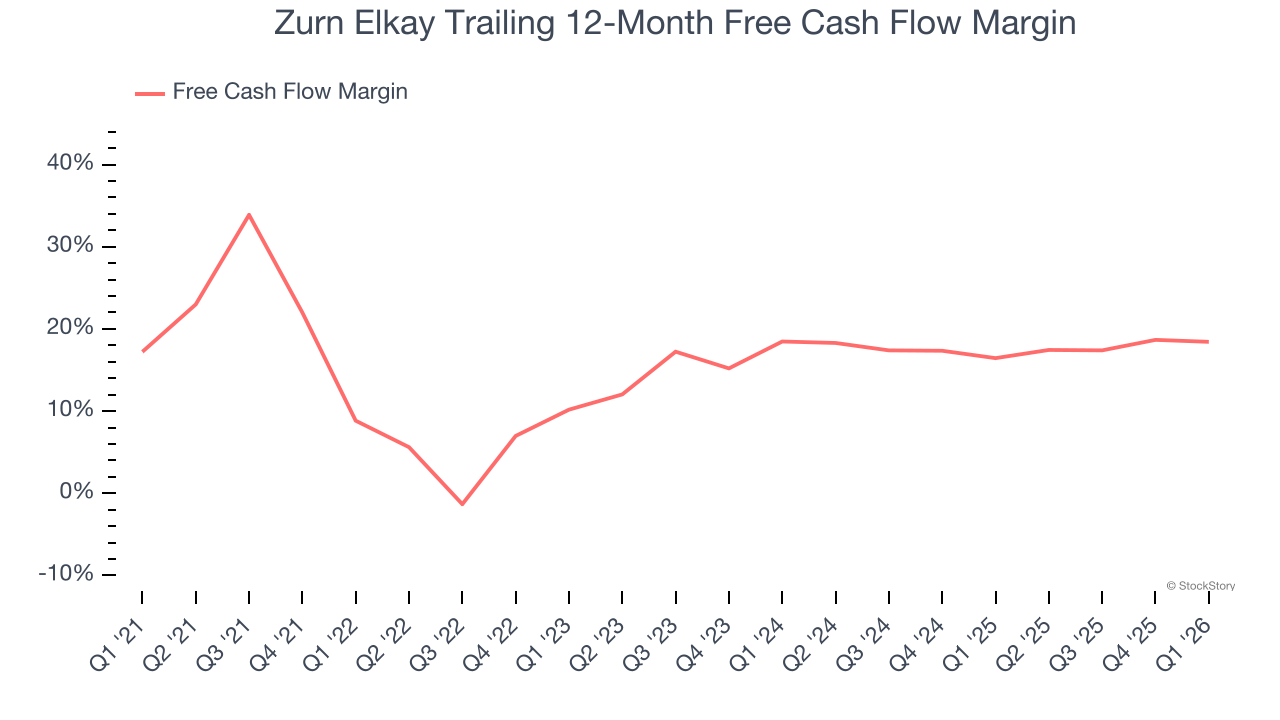

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Zurn Elkay has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 15.1% over the last five years.

One Reason to Be Careful:

Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand HVAC and Water Systems companies by analyzing their organic revenue. This metric gives visibility into Zurn Elkay’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Zurn Elkay’s organic revenue averaged 5.8% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

Zurn Elkay’s merits more than compensate for its flaws, but at $50.19 per share (or 27× forward P/E), is now the right time to buy the stock? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Zurn Elkay

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.