Old Second Bancorp has been treading water for the past six months, recording a small return of 3.9% while holding steady at $21.66. The stock also fell short of the S&P 500’s 10.9% gain during that period.

Does this present a buying opportunity for OSBC? Or is its underperformance reflective of its story and business quality? Find out in our full research report, it’s free.

Why Does Old Second Bancorp Spark Debate?

Dating back to 1871 as one of the Chicago area's longest-standing financial institutions, Old Second Bancorp (NASDAQ:OSBC) is an Illinois-based community bank offering deposit services, commercial and consumer loans, wealth management, and mortgage products through its 53 branch locations.

Two Positive Attributes:

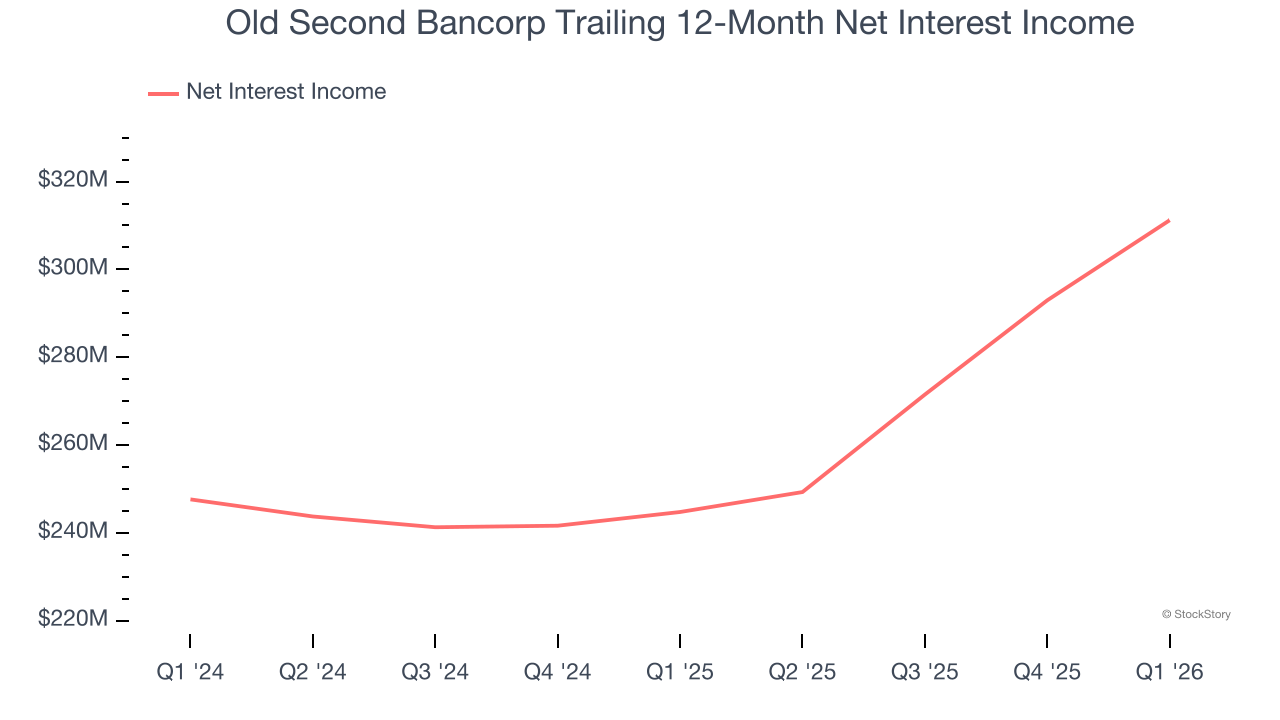

1. Net Interest Income Skyrockets, Fueling Growth Opportunities

While banks generate revenue from multiple sources, investors view net interest income as a cornerstone — its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Old Second Bancorp’s net interest income has grown at a 27.4% annualized rate over the last five years, much better than the broader banking industry and faster than its total revenue. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

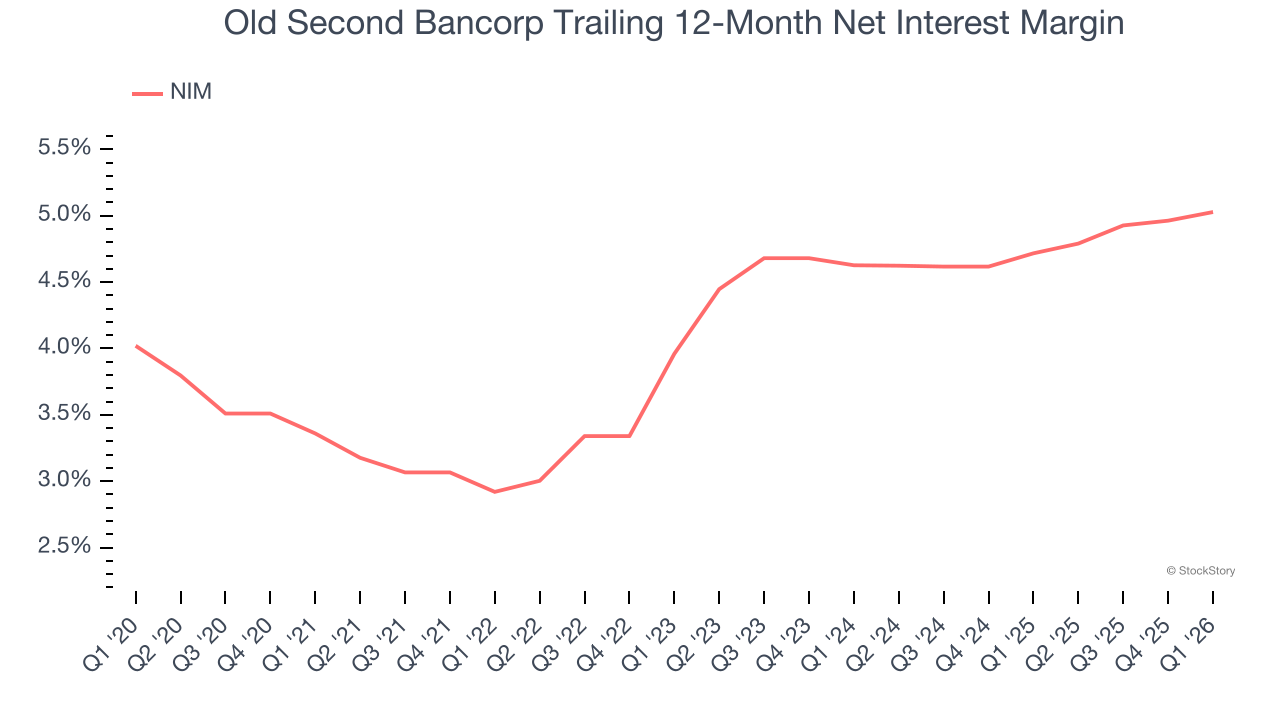

2. Elite Net Interest Margin Powers Best-In-Class Loan Book

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It’s one of the most important metrics to track because it shows how a bank’s loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that Old Second Bancorp’s net interest margin averaged an elite 4.9%, indicating the company has a high-yielding loan book and a low cost of funds.

One Reason to Be Careful:

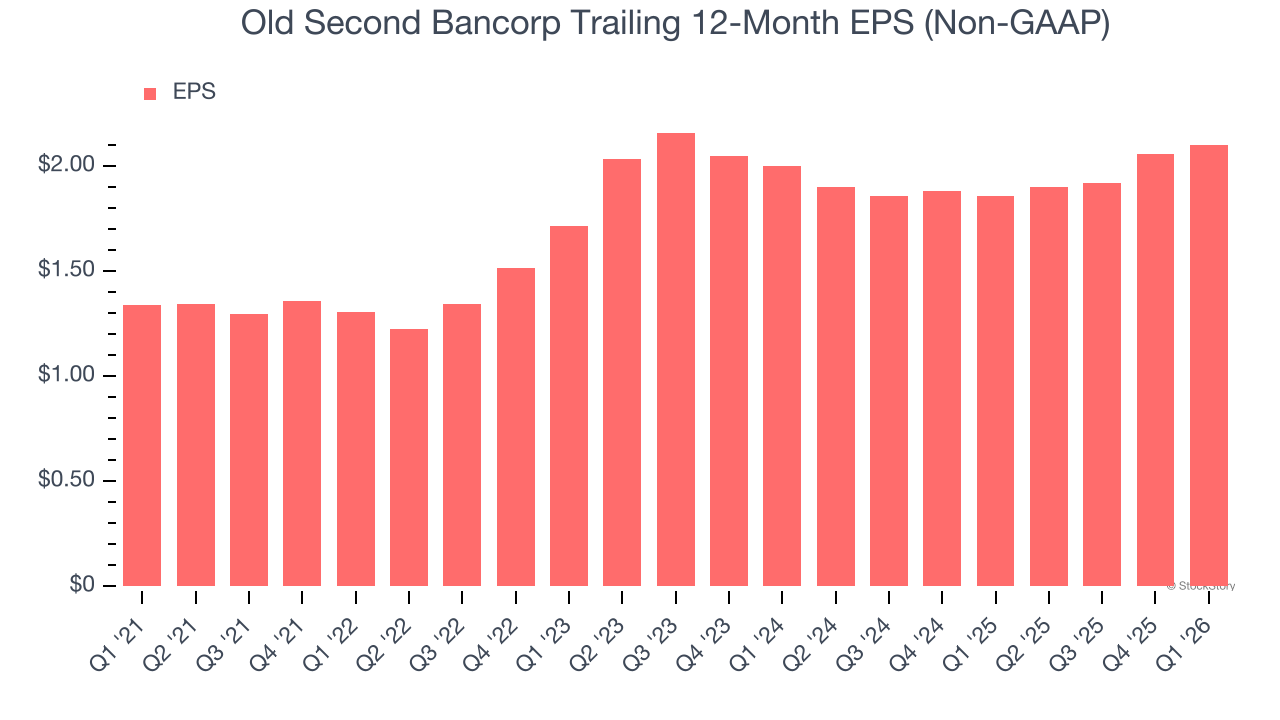

EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Old Second Bancorp’s EPS grew at an unimpressive 9.4% compounded annual growth rate over the last five years, lower than its 21.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Old Second Bancorp has huge potential even though it has some open questions. With its shares lagging the market recently, the stock trades at 1.2× forward P/B (or $21.66 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Old Second Bancorp

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.