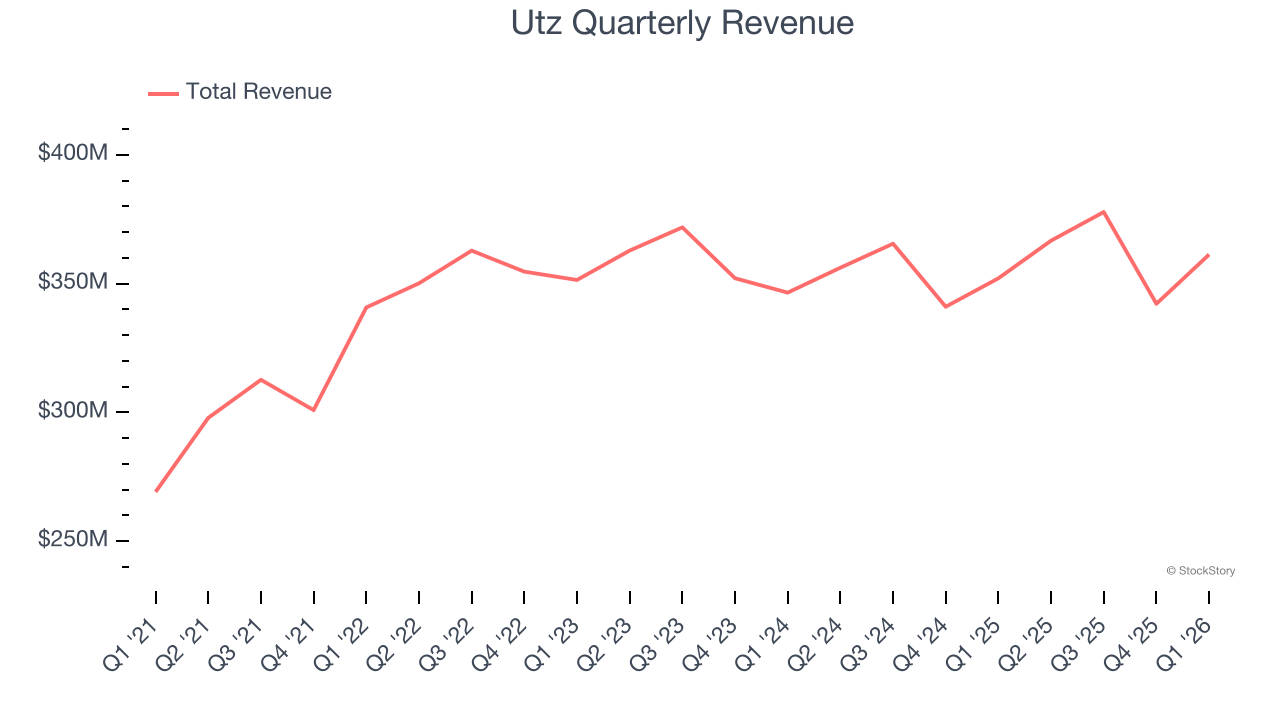

Snack food company Utz Brands (NYSE:UTZ) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 2.6% year on year to $361.3 million. Its non-GAAP profit of $0.15 per share was 7.7% above analysts’ consensus estimates.

Is now the time to buy Utz? Find out by accessing our full research report, it’s free.

Utz (UTZ) Q1 CY2026 Highlights:

- Revenue: $361.3 million vs analyst estimates of $361.8 million (2.6% year-on-year growth, in line)

- Adjusted EPS: $0.15 vs analyst estimates of $0.14 (7.7% beat)

- Adjusted EBITDA: $47.9 million vs analyst estimates of $47.34 million (13.3% margin, 1.2% beat)

- Operating Margin: 2.2%, in line with the same quarter last year

- Free Cash Flow was -$26 million compared to -$59.01 million in the same quarter last year

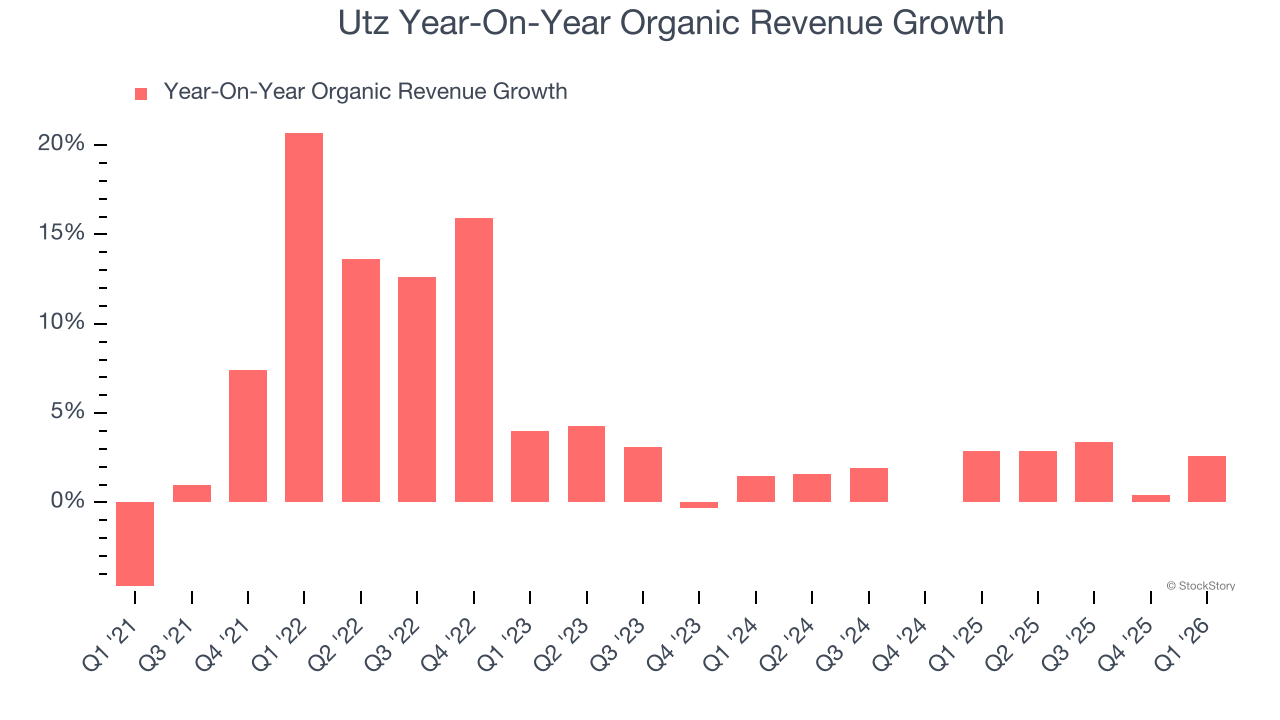

- Organic Revenue rose 2.6% year on year (miss)

- Sales Volumes were down 1.1% year on year

- Market Capitalization: $680 million

“I’m pleased with our solid start to the year, as we delivered 2.6% Net Sales growth and 5.2% Branded Salty Snacks growth, gained dollar share in the Salty Snacks category(2), and continued to expand Adjusted EBITDA margins,” said Howard Friedman, Chief Executive Officer of Utz.

Company Overview

Tracing its roots back to 1921 when Bill and Salie Utz began making potato chips in their kitchen, Utz Brands (NYSE:UTZ) offers salty snacks such as potato chips, tortilla chips, pretzels, cheese snacks, and ready-to-eat popcorn, among others.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.45 billion in revenue over the past 12 months, Utz is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Utz struggled to increase demand as its $1.45 billion of sales for the trailing 12 months was close to its revenue three years ago. To its credit, however, consumers bought more of its products - we’ll explore what this means in the "Volume Growth" section.

This quarter, Utz grew its revenue by 2.6% year on year, and its $361.3 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. Although this projection implies its newer products will catalyze better top-line performance, it is still below average for the sector.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Utz’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 2%.

In the latest quarter, Utz’s organic sales rose by 2.6% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Utz’s Q1 Results

It was good to see Utz beat analysts’ EPS expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed and its gross margin fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded up 3.3% to $7.95 immediately following the results.

Is Utz an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).