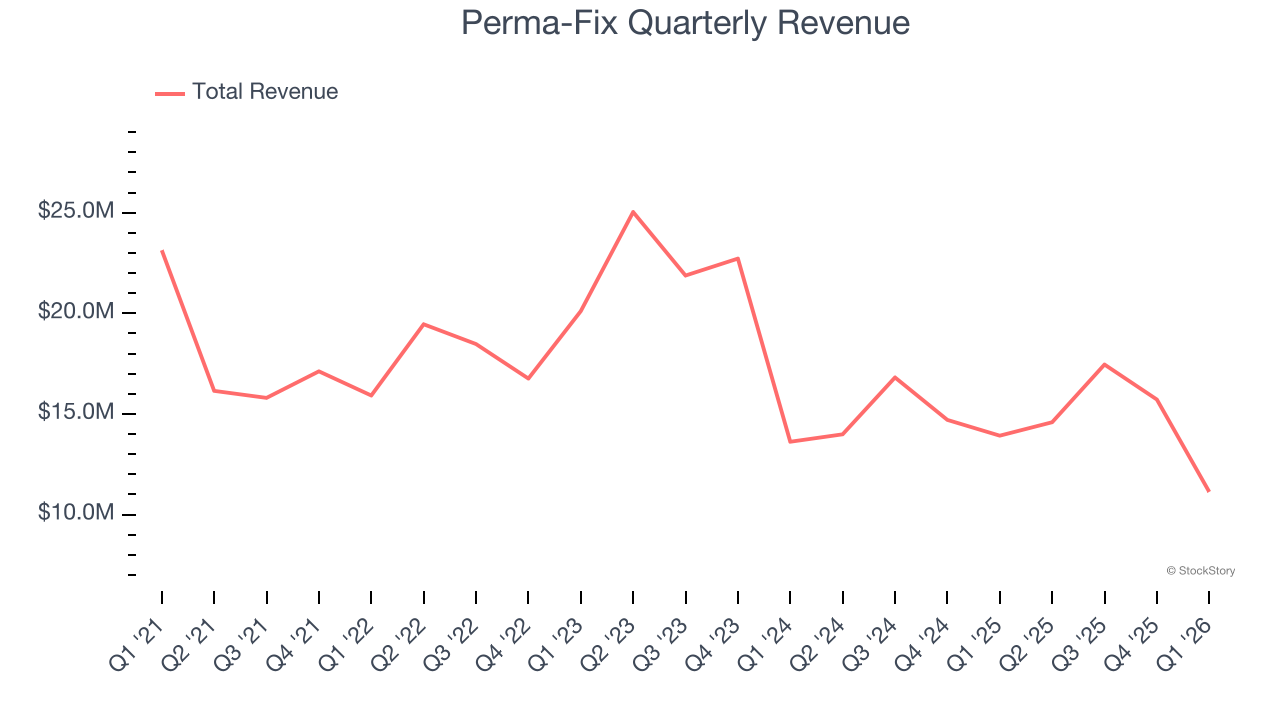

Environmental waste treatment and services provider Perma-Fix (NASDAQ:PESI) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 20.1% year on year to $11.13 million. Its GAAP loss of $0.40 per share was 66.7% below analysts’ consensus estimates.

Is now the time to buy Perma-Fix? Find out by accessing our full research report, it’s free.

Perma-Fix (PESI) Q1 CY2026 Highlights:

- Revenue: $11.13 million vs analyst estimates of $13 million (20.1% year-on-year decline, 14.4% miss)

- EPS (GAAP): -$0.40 vs analyst expectations of -$0.24 (66.7% miss)

- Adjusted EBITDA: -$6.99 million (-62.8% margin, 114% year-on-year decline)

- Adjusted EBITDA Margin: -62.8%, down from -23.5% in the same quarter last year

- Market Capitalization: $239.8 million

“As expected, the first quarter represented a transitional period as we deliberately positioned the Company for what we believe will be a significant step-up in activity beginning in the second quarter,” commented Mark Duff, President and Chief Executive Officer of Perma-Fix.

Company Overview

Tackling hazardous waste challenges since 1990, Perma-Fix (NASDAQ:PESI) provides environmental waste treatment services.

Revenue Growth

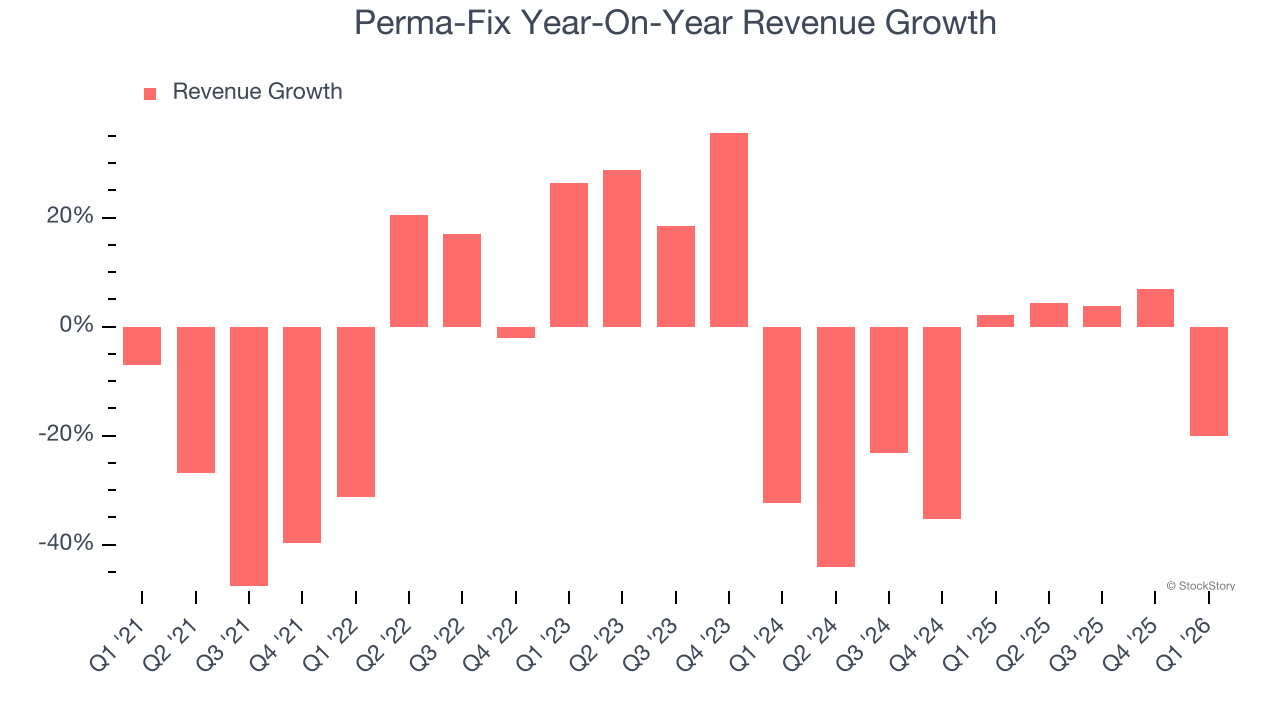

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Perma-Fix struggled to consistently generate demand over the last five years as its sales dropped at a 10.7% annual rate. This wasn’t a great result and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Perma-Fix’s recent performance shows its demand remained suppressed as its revenue has declined by 15.9% annually over the last two years.

This quarter, Perma-Fix missed Wall Street’s estimates and reported a rather uninspiring 20.1% year-on-year revenue decline, generating $11.13 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 67.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

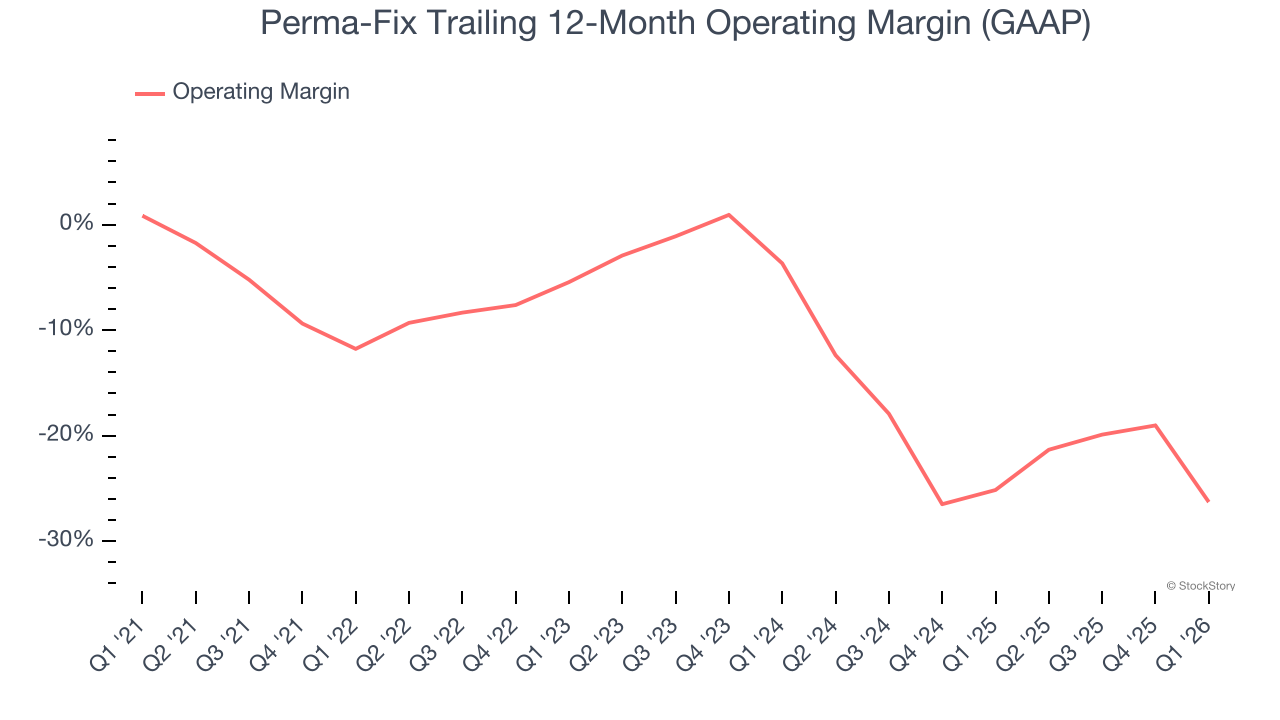

Perma-Fix’s high expenses have contributed to an average operating margin of negative 13.2% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Perma-Fix’s operating margin decreased by 14.5 percentage points over the last five years. Perma-Fix’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Perma-Fix’s operating margin was negative 67.3% this quarter. The company's consistent lack of profits raise a flag.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

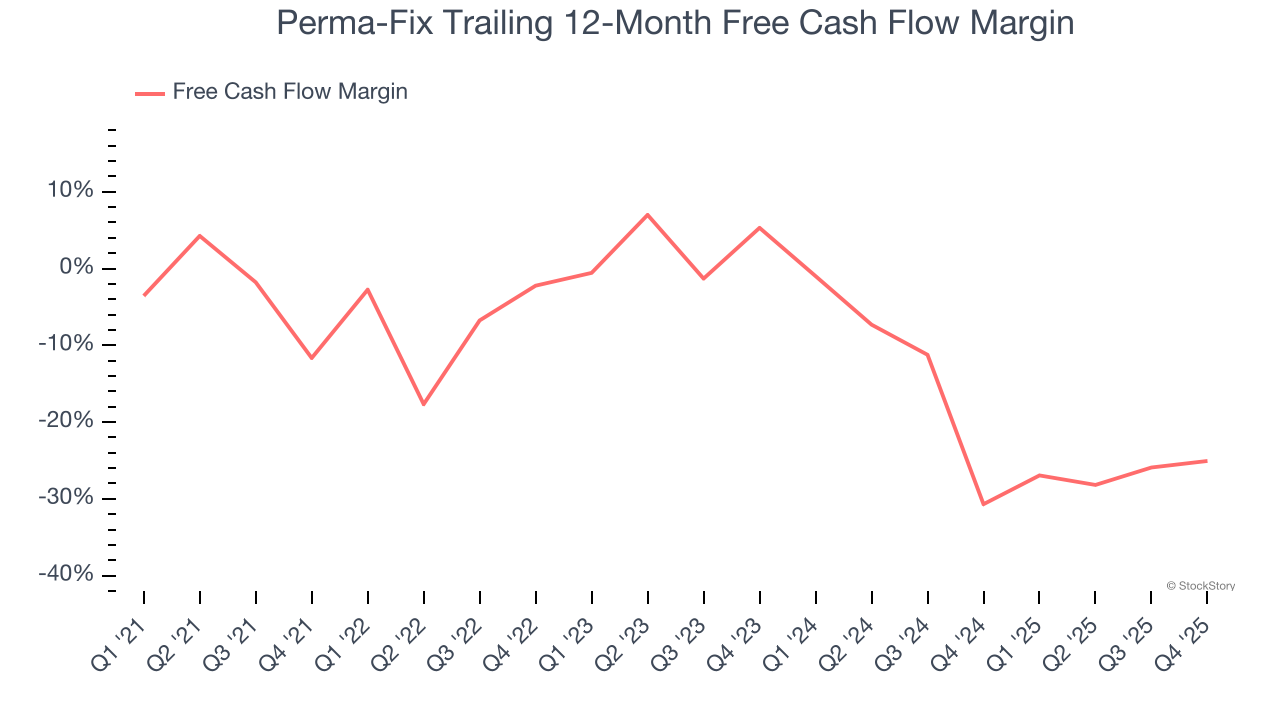

Perma-Fix’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 9.7%, meaning it lit $9.65 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Perma-Fix’s margin dropped by 23.9 percentage points during that time. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Key Takeaways from Perma-Fix’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its adjusted operating income fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.2% to $12.28 immediately following the results.

The latest quarter from Perma-Fix’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).