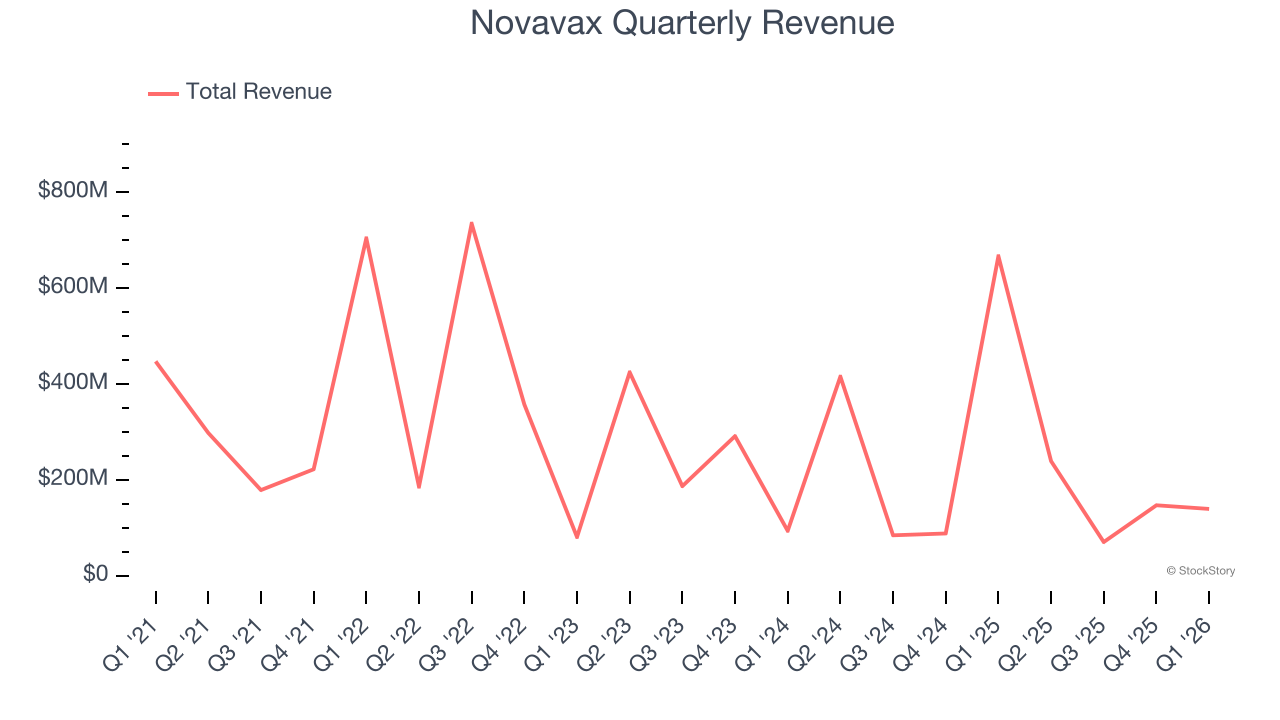

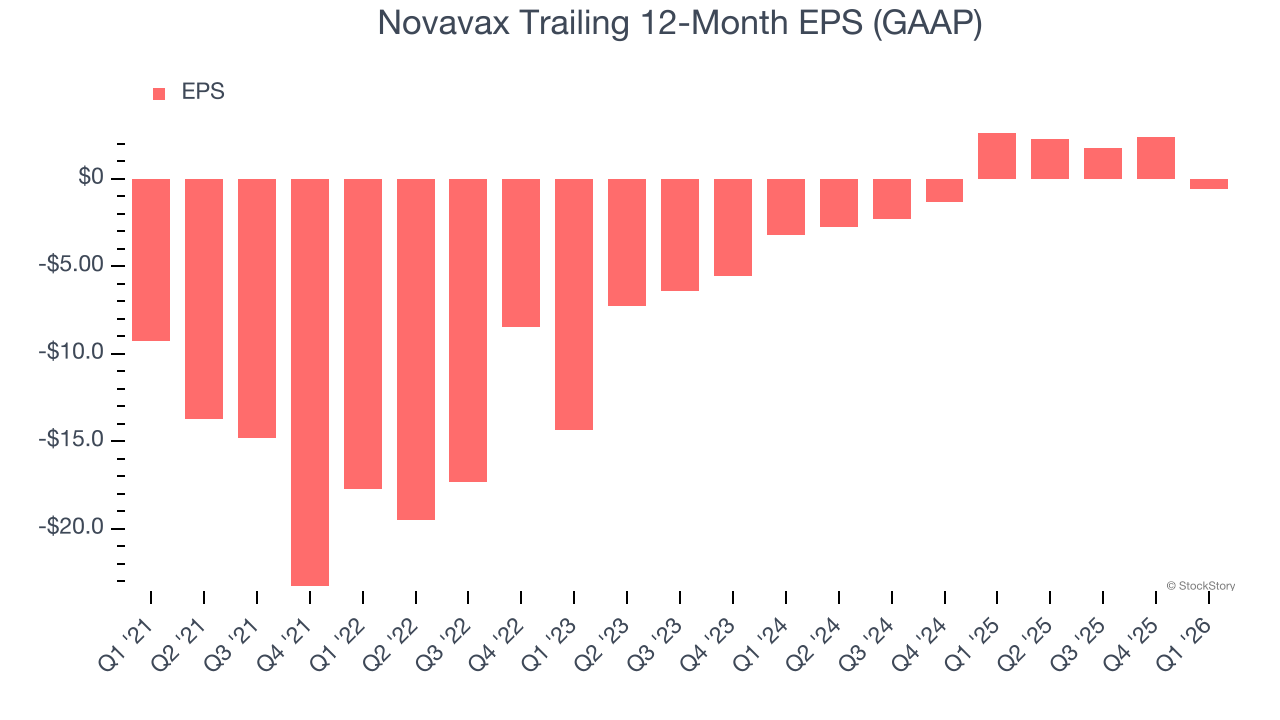

Vaccine biotechnology company Novavax (NASDAQ:NVAX) beat Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 79.1% year on year to $139.5 million. Its GAAP loss of $0.06 per share was 73.5% above analysts’ consensus estimates.

Is now the time to buy Novavax? Find out by accessing our full research report, it’s free.

Novavax (NVAX) Q1 CY2026 Highlights:

- Revenue: $139.5 million vs analyst estimates of $75.61 million (79.1% year-on-year decline, 84.5% beat)

- EPS (GAAP): -$0.06 vs analyst estimates of -$0.23 (73.5% beat)

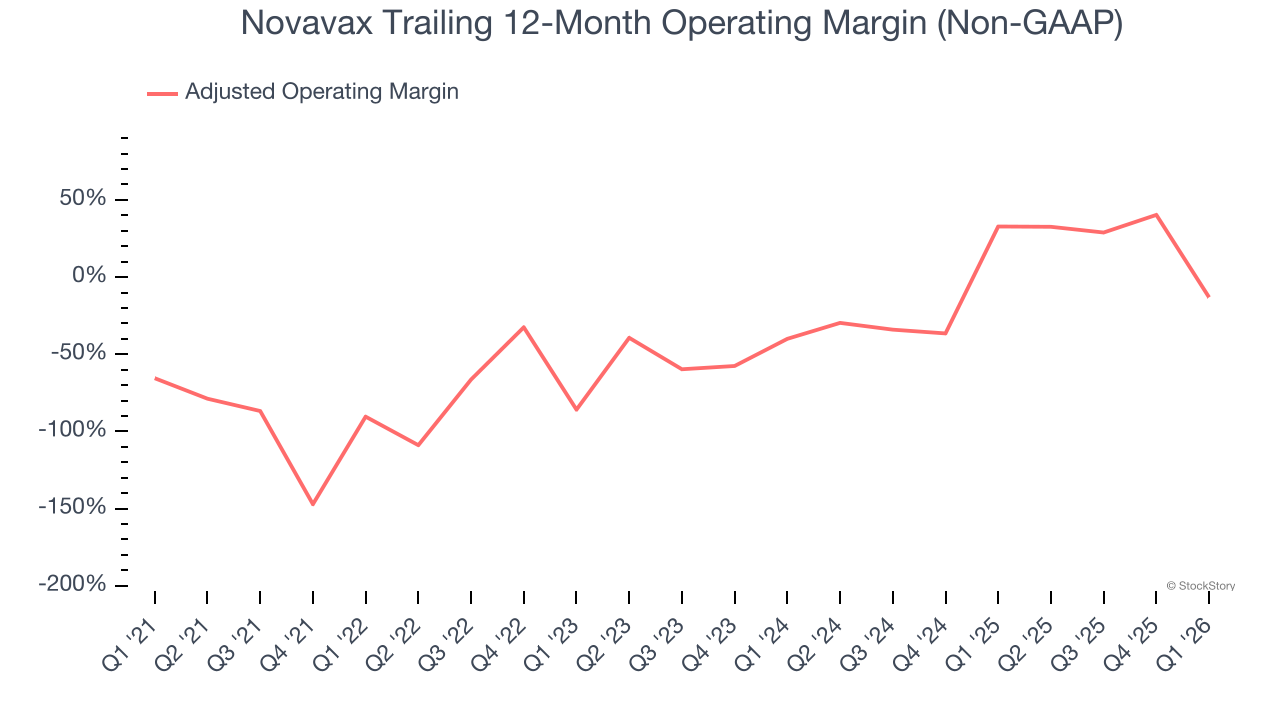

- Adjusted Operating Income: -$15.43 million vs analyst estimates of -$28.05 million (-11.1% margin, 45% beat)

- Operating Margin: -11.1%, down from 77.3% in the same quarter last year

- Market Capitalization: $1.33 billion

"Novavax continued to make significant progress executing our corporate strategy, which is comprised of partnering our technology, capital-efficient R&D innovation and a lean operating platform. In 2026, we signed a new, Matrix-M license with Pfizer for up to two vaccine candidates and secured four additional MTAs with a growing list of large pharmaceutical and innovative biotech companies," said John C. Jacobs, President and Chief Executive Officer, Novavax.

Company Overview

Pioneering a nanoparticle technology that mimics the molecular structure of disease pathogens, Novavax (NASDAQ:NVAX) develops and commercializes protein-based vaccines for infectious diseases, with a primary focus on its COVID-19 vaccine and combination respiratory vaccine candidates.

Revenue Growth

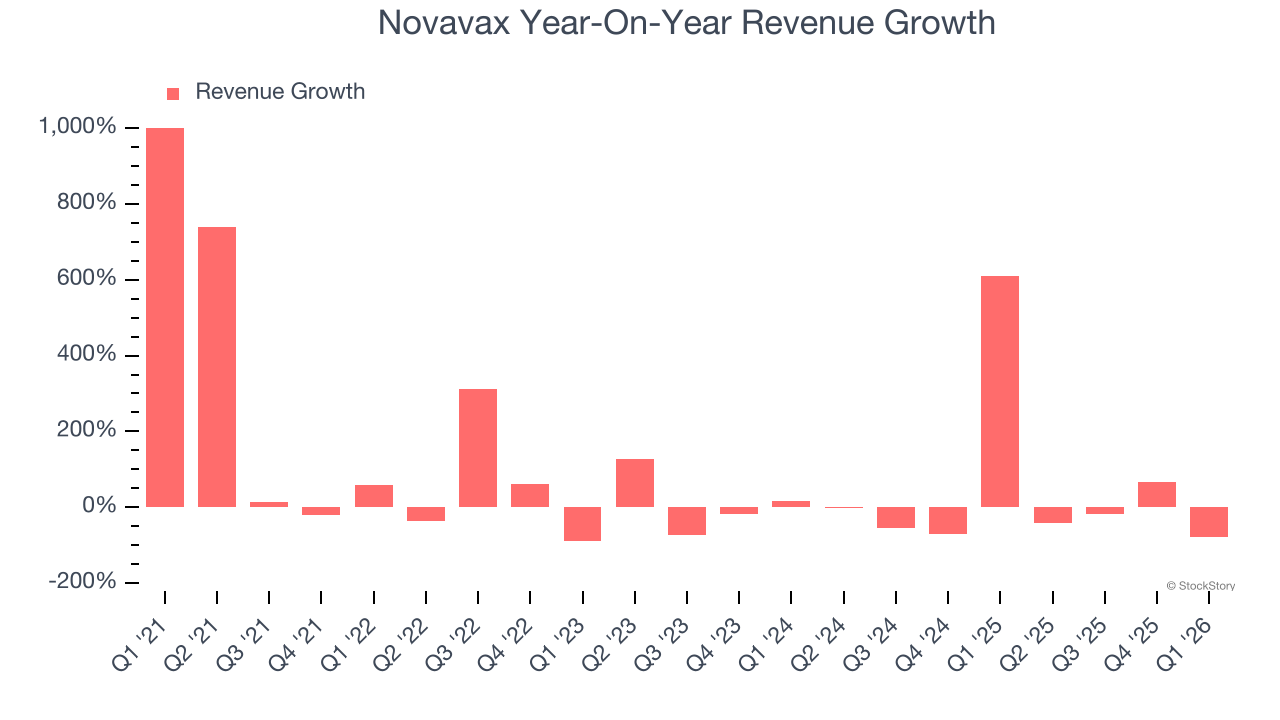

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Novavax’s demand was weak over the last five years as its sales fell at a 8.3% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Novavax’s recent performance shows its demand remained suppressed as its revenue has declined by 22.6% annually over the last two years.

This quarter, Novavax’s revenue fell by 79.1% year on year to $139.5 million but beat Wall Street’s estimates by 84.5%.

Looking ahead, sell-side analysts expect revenue to decline by 37.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Novavax’s high expenses have contributed to an average adjusted operating margin of negative 44.6% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Novavax’s adjusted operating margin rose by 77.3 percentage points over the last five years. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 26.9 percentage points on a two-year basis.

Novavax’s adjusted operating margin was negative 11.1% this quarter. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Novavax’s full-year earnings are still negative, it reduced its losses and improved its EPS by 42.2% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, Novavax reported EPS of negative $0.06, down from $2.92 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Novavax’s Q1 Results

It was good to see Novavax beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 7% to $8.62 immediately following the results.

Novavax put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).