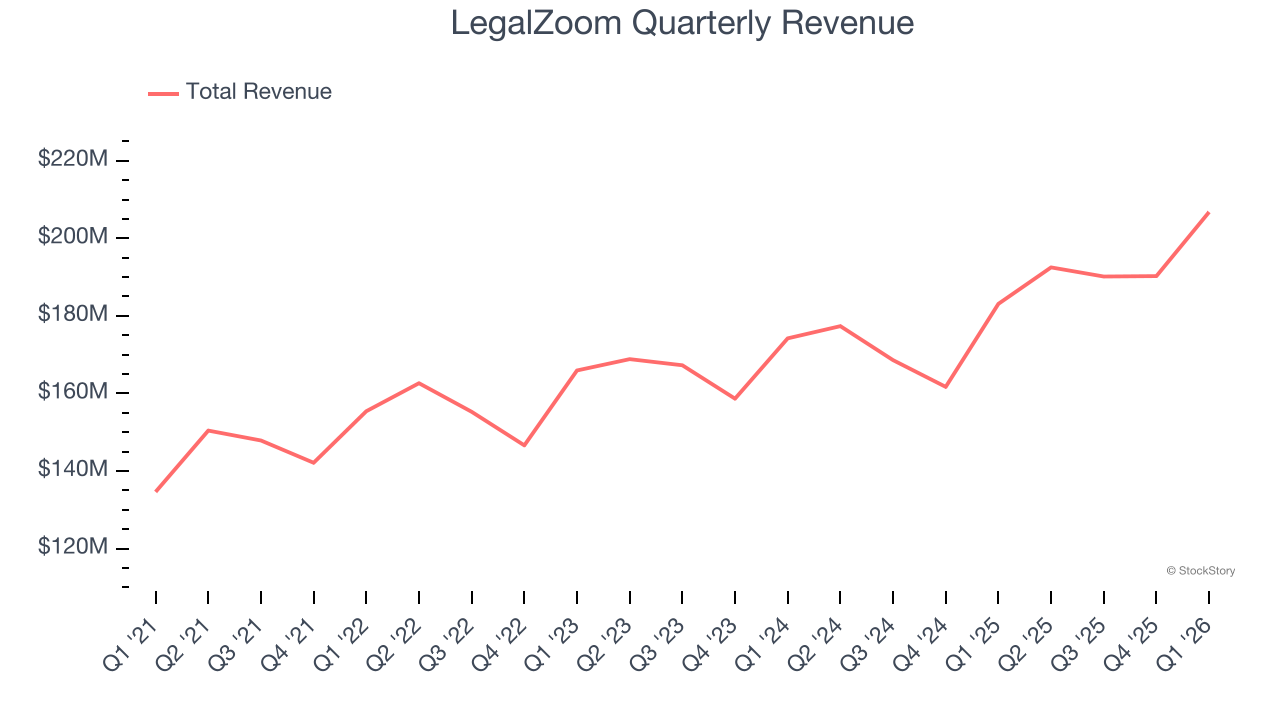

Online legal service provider LegalZoom (NASDAQ:LZ) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 12.9% year on year to $206.8 million. On the other hand, next quarter’s revenue guidance of $205 million was less impressive, coming in 1.1% below analysts’ estimates. Its GAAP profit of $0.01 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy LegalZoom? Find out by accessing our full research report, it’s free.

LegalZoom (LZ) Q1 CY2026 Highlights:

- Revenue: $206.8 million vs analyst estimates of $201.8 million (12.9% year-on-year growth, 2.5% beat)

- EPS (GAAP): $0.01 vs analyst estimates of $0 ($0.01 beat)

- Adjusted EBITDA: $36.46 million vs analyst estimates of $36.25 million (17.6% margin, 0.6% beat)

- The company slightly lifted its revenue guidance for the full year to $820 million at the midpoint from $815 million

- EBITDA guidance for the full year is $195 million at the midpoint, in line with analyst expectations

- Operating Margin: 1.3%, down from 4.9% in the same quarter last year

- Free Cash Flow Margin: 19.8%, up from 14.7% in the previous quarter

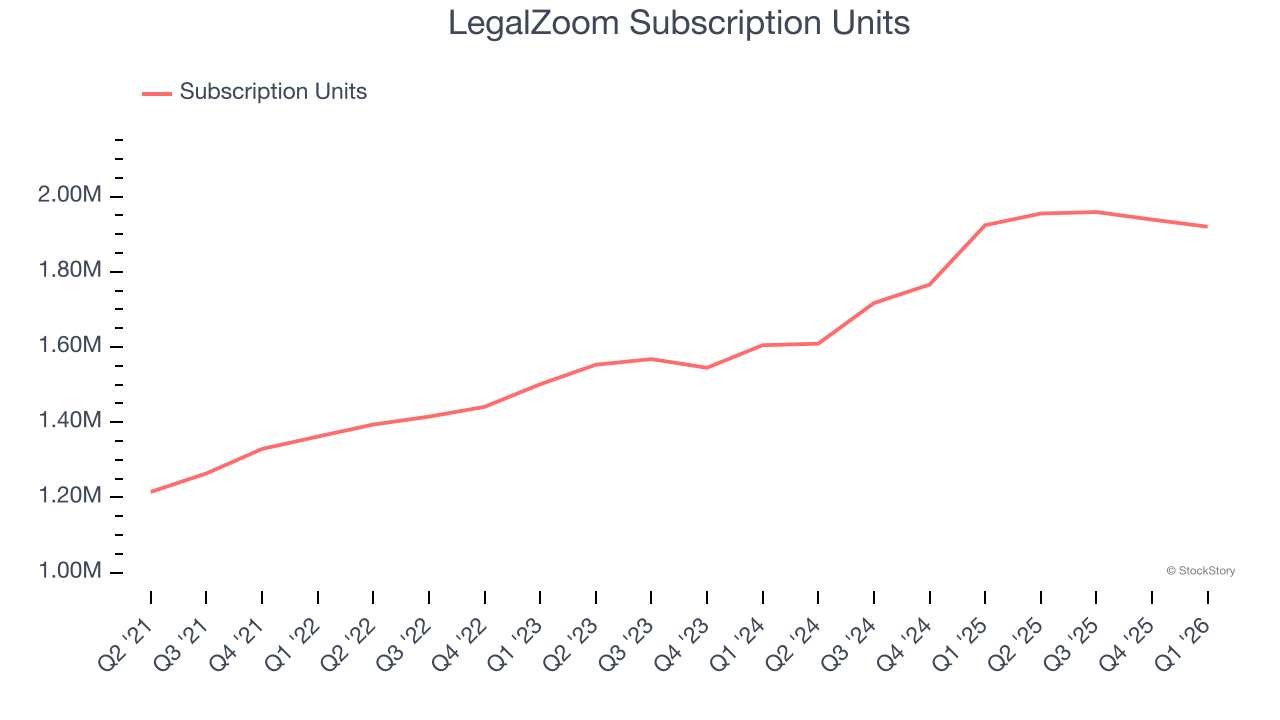

- Subscription Units: 1.92 million, in line with the same quarter last year

- Market Capitalization: $1.16 billion

“LegalZoom delivered another strong quarter, clearly illustrating that our strategy is working,” said Jeff Stibel, Chairman and Chief Executive Officer of LegalZoom.

Company Overview

Founded by famous lawyer Robert Shapiro, LegalZoom (NASDAQ:LZ) offers online legal services and documentation assistance for individuals and businesses.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, LegalZoom’s 7.3% annualized revenue growth over the last three years was tepid. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about LegalZoom.

This quarter, LegalZoom reported year-on-year revenue growth of 12.9%, and its $206.8 million of revenue exceeded Wall Street’s estimates by 2.5%. Company management is currently guiding for a 6.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7% over the next 12 months, similar to its three-year rate. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet. At least the company is tracking well in other measures of financial health.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Subscription Units

User Growth

As an online marketplace, LegalZoom generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, LegalZoom’s subscription units, a key performance metric for the company, increased by 11.6% annually to 1.92 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

Unfortunately, LegalZoom’s subscription units were flat year on year in Q1. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for users yet.

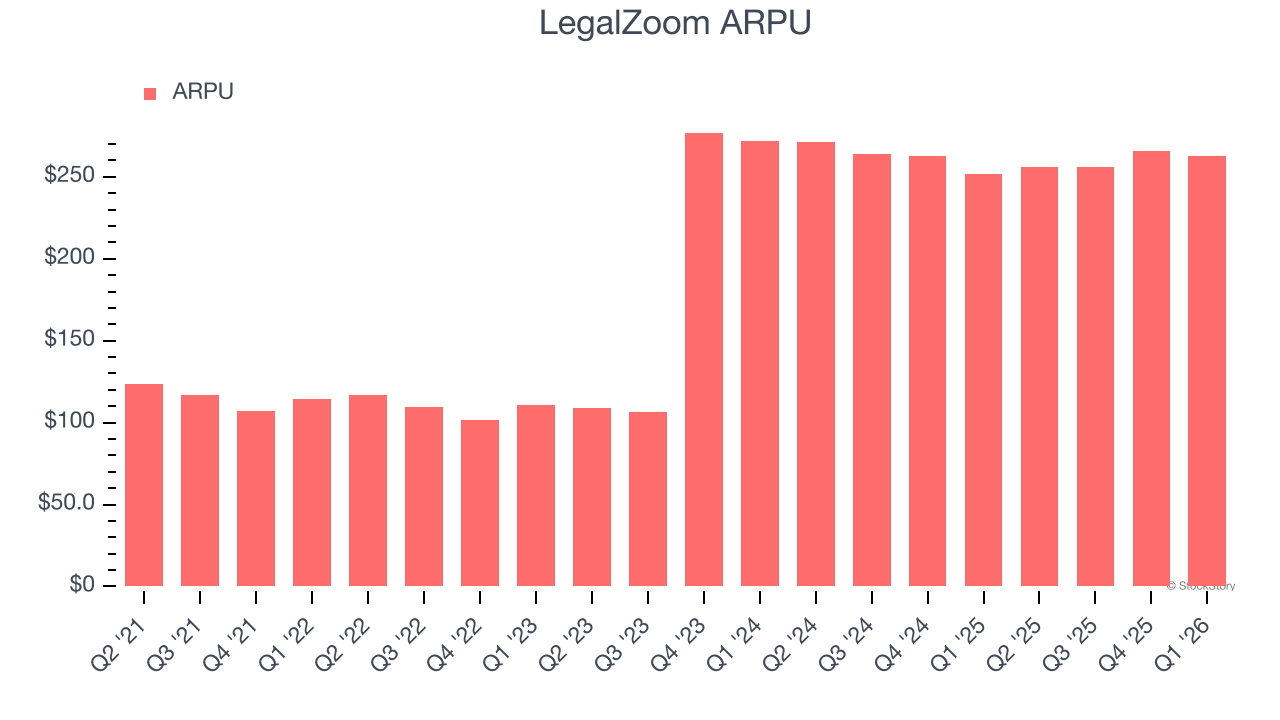

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and LegalZoom’s take rate, or "cut", on each order.

LegalZoom’s ARPU growth has been exceptional over the last two years, averaging 35.2%. Its ability to increase monetization while growing its subscription units at an impressive rate reflects the strength of its platform, as its users are spending significantly more than last year.

This quarter, LegalZoom’s ARPU clocked in at $263. It grew by 4.4% year on year, faster than its subscription units.

Key Takeaways from LegalZoom’s Q1 Results

It was encouraging to see LegalZoom beat analysts’ revenue expectations this quarter. On the other hand, its revenue guidance for next quarter slightly missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.8% to $6.16 immediately after reporting.

LegalZoom didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).