IT infrastructure services provider Kyndryl (NYSE:KD) met Wall Street’s revenue expectations in Q1 CY2026, but sales were flat year on year at $3.77 billion. Its non-GAAP profit of $0.18 per share was 61.6% below analysts’ consensus estimates.

Is now the time to buy Kyndryl? Find out by accessing our full research report, it’s free.

Kyndryl (KD) Q1 CY2026 Highlights:

- Revenue: $3.77 billion vs analyst estimates of $3.76 billion (flat year on year, in line)

- Adjusted EPS: $0.18 vs analyst expectations of $0.47 (61.6% miss)

- Adjusted EBITDA: $688 million vs analyst estimates of $670.6 million (18.3% margin, 2.6% beat)

- Operating Margin: 3.5%, in line with the same quarter last year

- Free Cash Flow Margin: 10.3%, up from 6.8% in the same quarter last year

- Market Capitalization: $3.31 billion

NEW YORK, May 6, 2026 /PRNewswire/ -- Kyndryl (NYSE: KD), a leading provider of mission-critical enterprise technology services, today released financial results for its 2026 fiscal year and the quarter ended March 31, 2026, the fourth quarter of its 2026 fiscal year. "With our mission-critical engineering expertise, we continue to support our customers' most complex IT environments while taking disciplined actions to strengthen our business," said Kyndryl Chairman and Chief Executive Officer Martin Schroeter.

Company Overview

Born from IBM's managed infrastructure services business in a 2021 spinoff, Kyndryl (NYSE:KD) is the world's largest IT infrastructure services provider that designs, builds, and manages technology environments for enterprise customers.

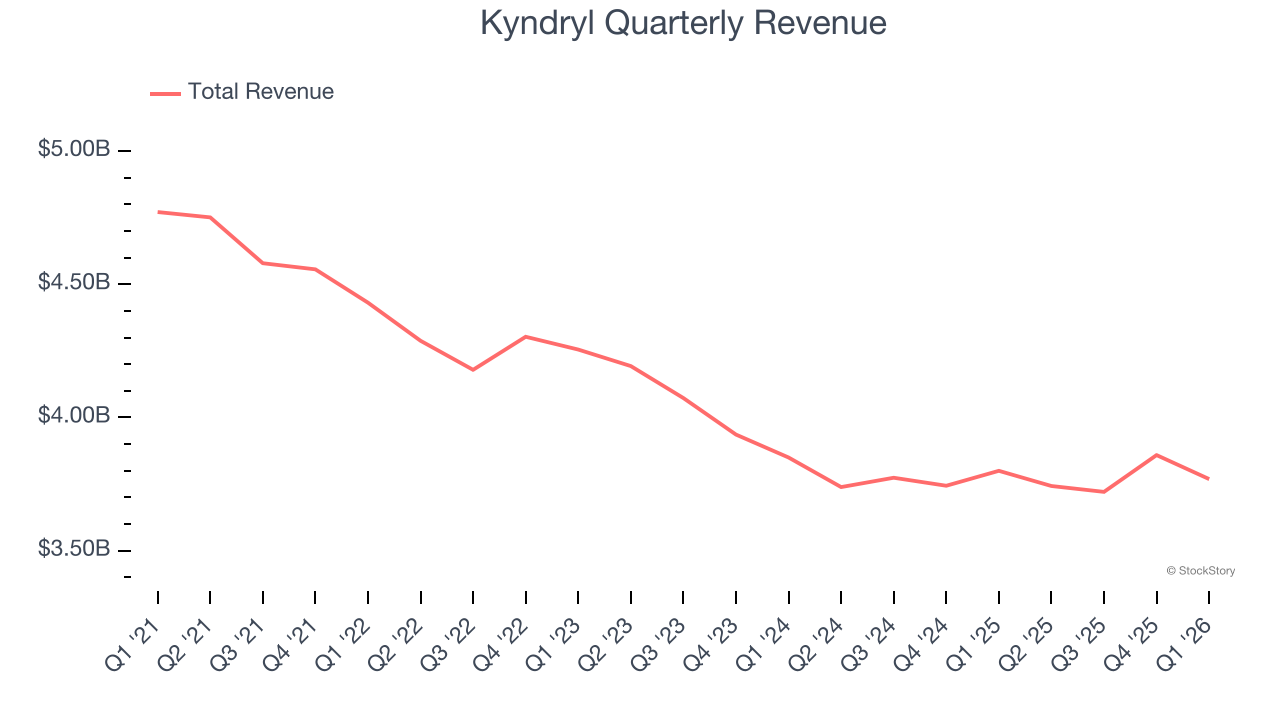

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $15.09 billion in revenue over the past 12 months, Kyndryl is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, Kyndryl likely needs to tweak its prices, innovate with new offerings, or enter new markets.

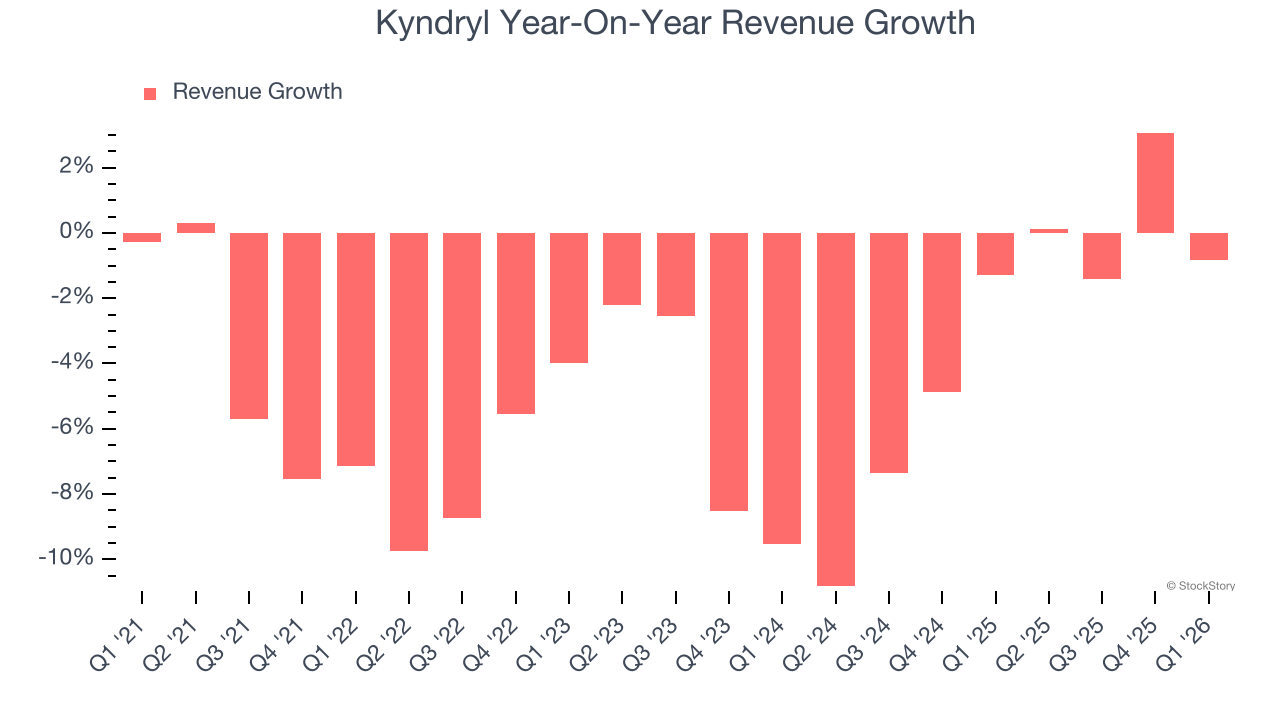

As you can see below, Kyndryl struggled to generate demand over the last five years. Its sales dropped by 4.8% annually, a poor baseline for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Kyndryl’s annualized revenue declines of 3% over the last two years suggest its demand continued shrinking.

This quarter, Kyndryl’s $3.77 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

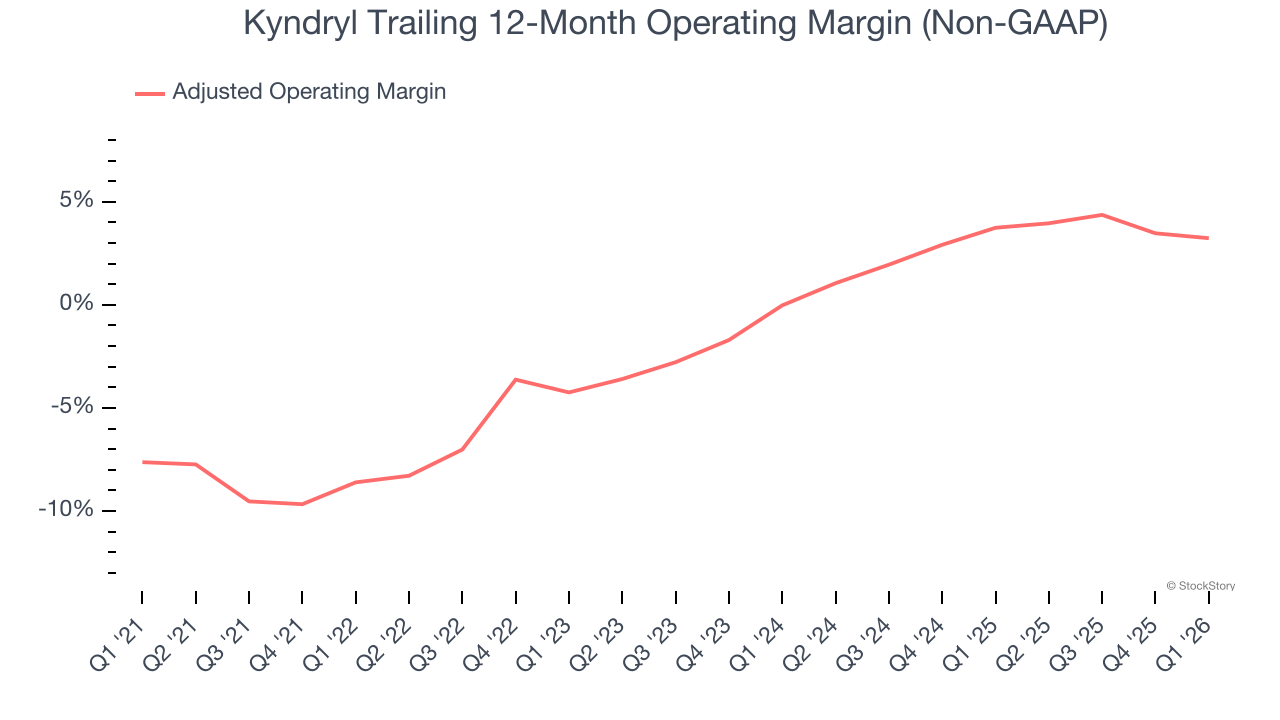

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Although Kyndryl was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average adjusted operating margin of negative 1.5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Kyndryl’s adjusted operating margin rose by 11.8 percentage points over the last five years. Still, it will take much more for the company to show consistent profitability.

In Q1, Kyndryl generated an adjusted operating margin profit margin of 3.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

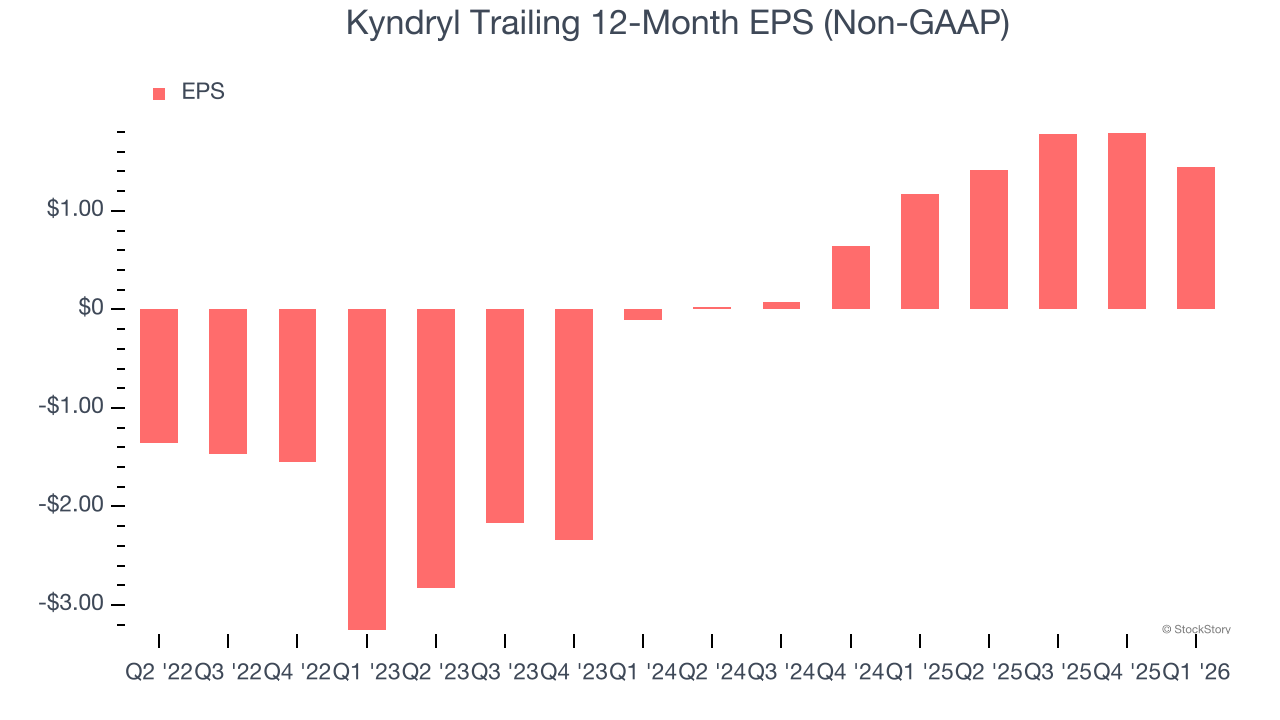

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Kyndryl’s full-year EPS flipped from negative to positive over the last four years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Kyndryl, its two-year annual EPS growth of 290% was higher than its four-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Kyndryl reported adjusted EPS of $0.18, down from $0.52 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Kyndryl’s full-year EPS of $1.45 to grow 54.2%.

Key Takeaways from Kyndryl’s Q1 Results

We struggled to find many positives in these results. Overall, this was a softer quarter. The stock remained flat at $14.82 immediately following the results.

Big picture, is Kyndryl a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).