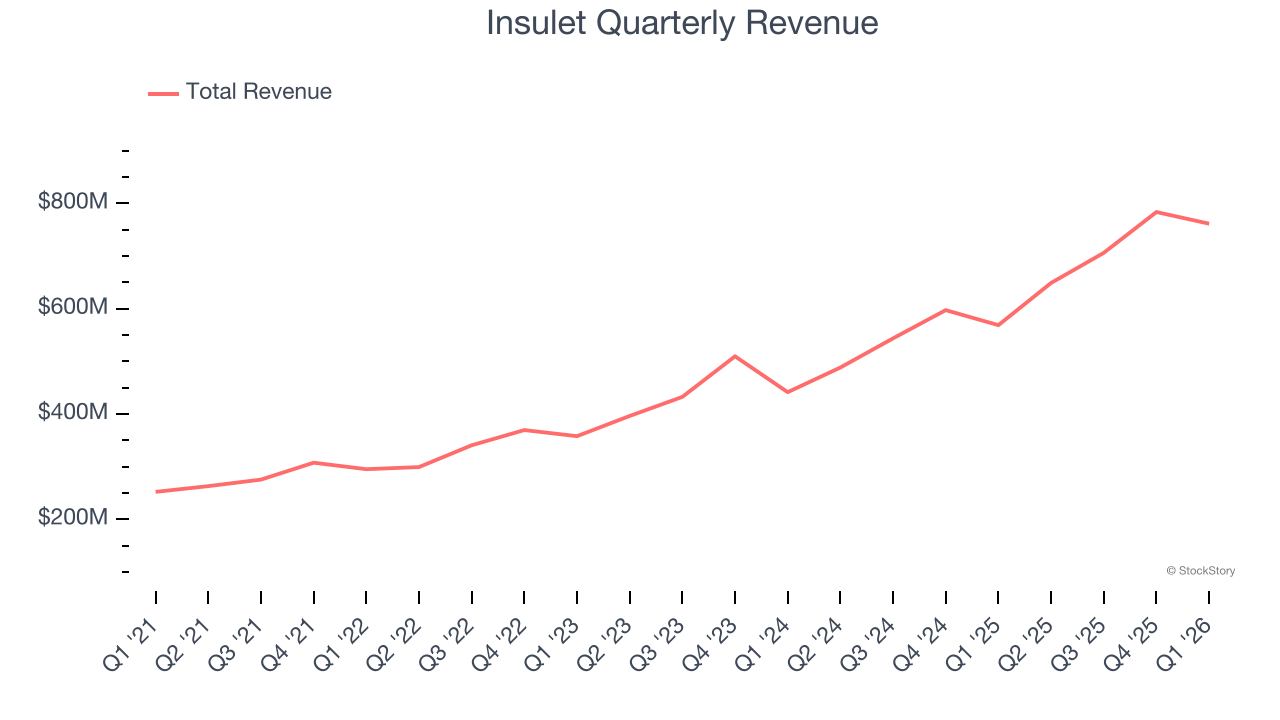

Insulin delivery company Insulet Corporation (NASDAQ:PODD) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 33.9% year on year to $761.7 million. On the other hand, next quarter’s revenue guidance of $785.4 million was less impressive, coming in 0.8% below analysts’ estimates. Its non-GAAP profit of $1.42 per share was 19.3% above analysts’ consensus estimates.

Is now the time to buy Insulet? Find out by accessing our full research report, it’s free.

Insulet (PODD) Q1 CY2026 Highlights:

- Revenue: $761.7 million vs analyst estimates of $730.9 million (33.9% year-on-year growth, 4.2% beat)

- Adjusted EPS: $1.42 vs analyst estimates of $1.19 (19.3% beat)

- Adjusted EBITDA: $181.7 million vs analyst estimates of $164.4 million (23.9% margin, 10.5% beat)

- Revenue Guidance for Q2 CY2026 is $785.4 million at the midpoint, below analyst estimates of $791.8 million

- Operating Margin: 16%, in line with the same quarter last year

- Free Cash Flow Margin: 11.8%, up from 9.1% in the same quarter last year

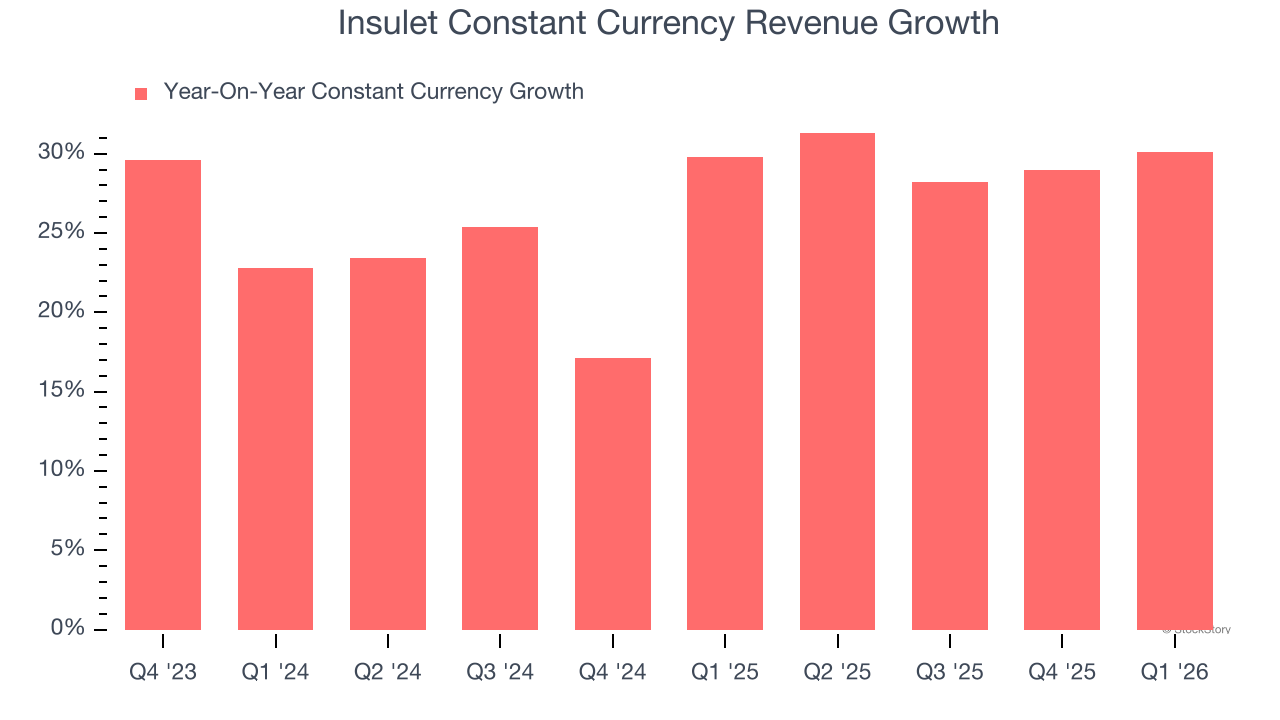

- Constant Currency Revenue rose 30.1% year on year, in line with the same quarter last year

- Market Capitalization: $11.6 billion

Company Overview

Revolutionizing diabetes care with its tubeless "Pod" technology, Insulet (NASDAQ:PODD) develops and manufactures innovative insulin delivery systems for people with diabetes, primarily through its Omnipod product line.

Revenue Growth

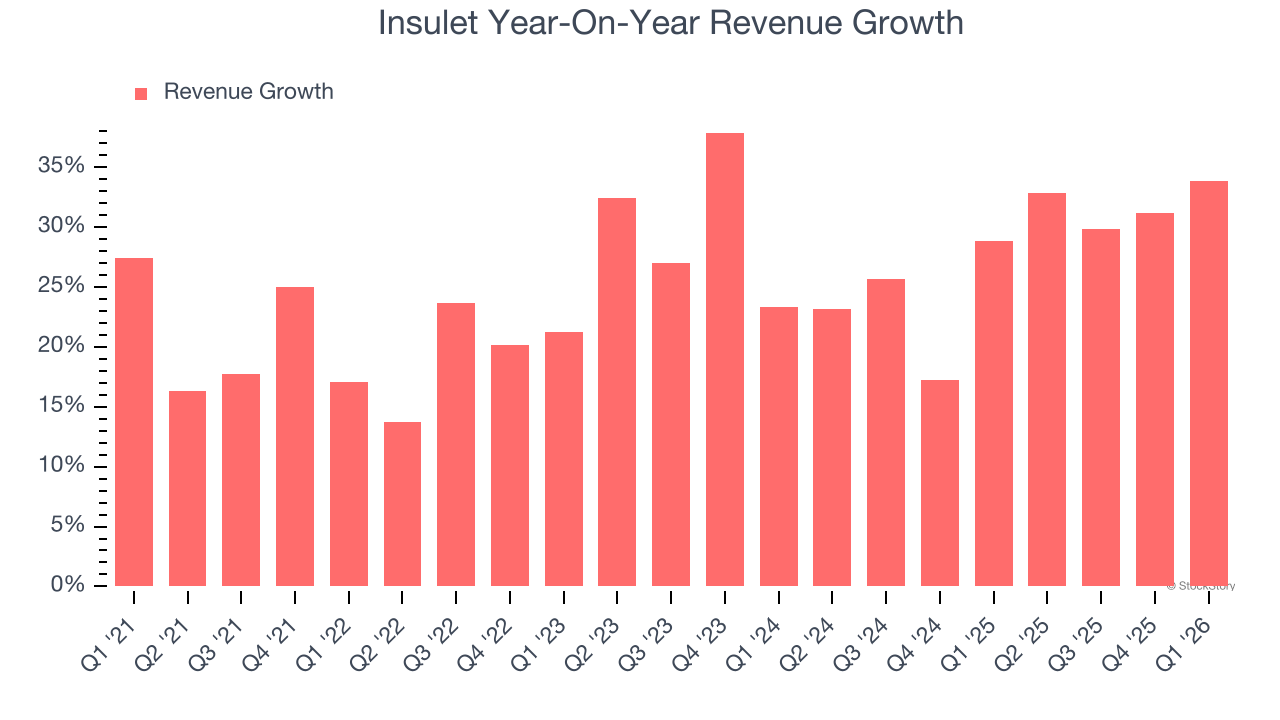

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Insulet’s sales grew at an excellent 24.8% compounded annual growth rate over the last five years. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Insulet’s annualized revenue growth of 27.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

Insulet also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 26.8% year-on-year growth. Because this number aligns with its reported revenue growth, we can see that foreign exchange has not had a meaningful impact on topline.

This quarter, Insulet reported wonderful year-on-year revenue growth of 33.9%, and its $761.7 million of revenue exceeded Wall Street’s estimates by 4.2%. Company management is currently guiding for a 21% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 19.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and implies the market is baking in success for its products and services.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

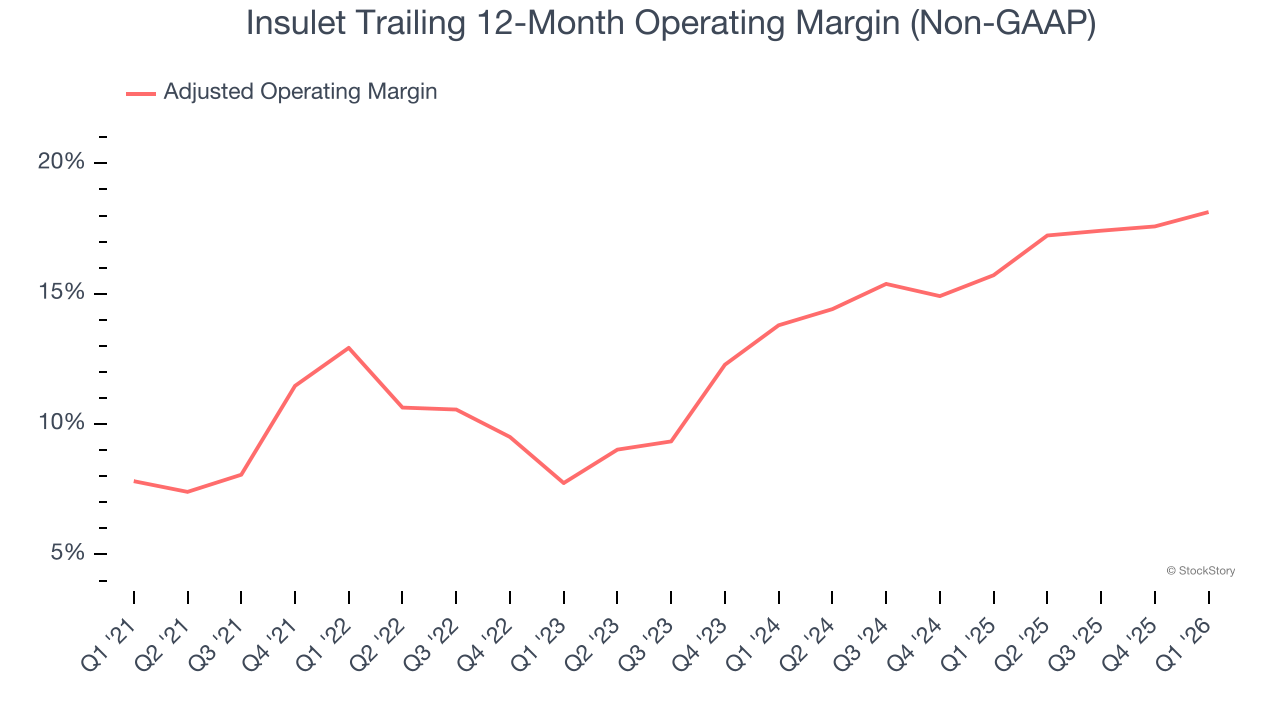

Insulet has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 14.6%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Insulet’s adjusted operating margin rose by 5.2 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements. These data points are very encouraging and show momentum is on its side.

This quarter, Insulet generated an adjusted operating margin profit margin of 18.8%, up 2.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

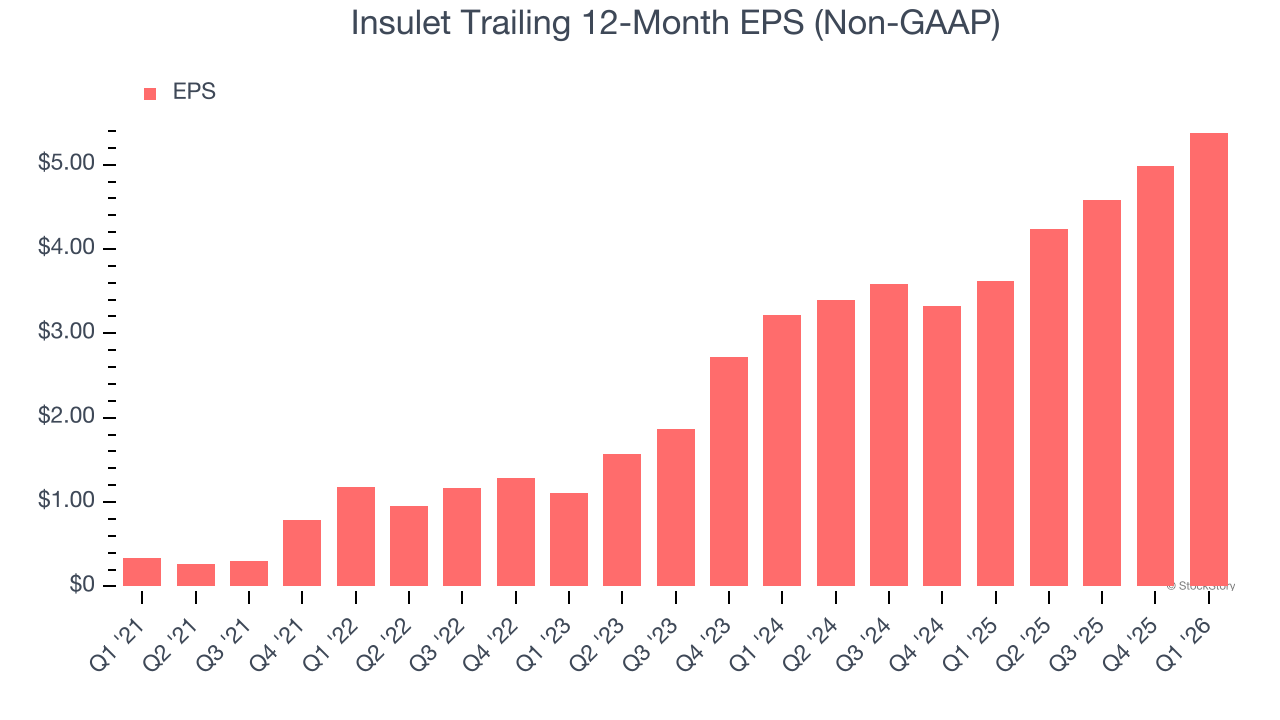

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Insulet’s EPS grew at 74.2% compounded annual growth rate over the last five years, higher than its 24.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Insulet’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Insulet’s adjusted operating margin expanded by 5.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Insulet reported adjusted EPS of $1.42, up from $1.02 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Insulet’s full-year EPS of $5.38 to grow 24.1%.

Key Takeaways from Insulet’s Q1 Results

We enjoyed seeing Insulet beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed. Zooming out, we think this was a solid print. The stock traded up 8.8% to $182.29 immediately following the results.

Insulet had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).