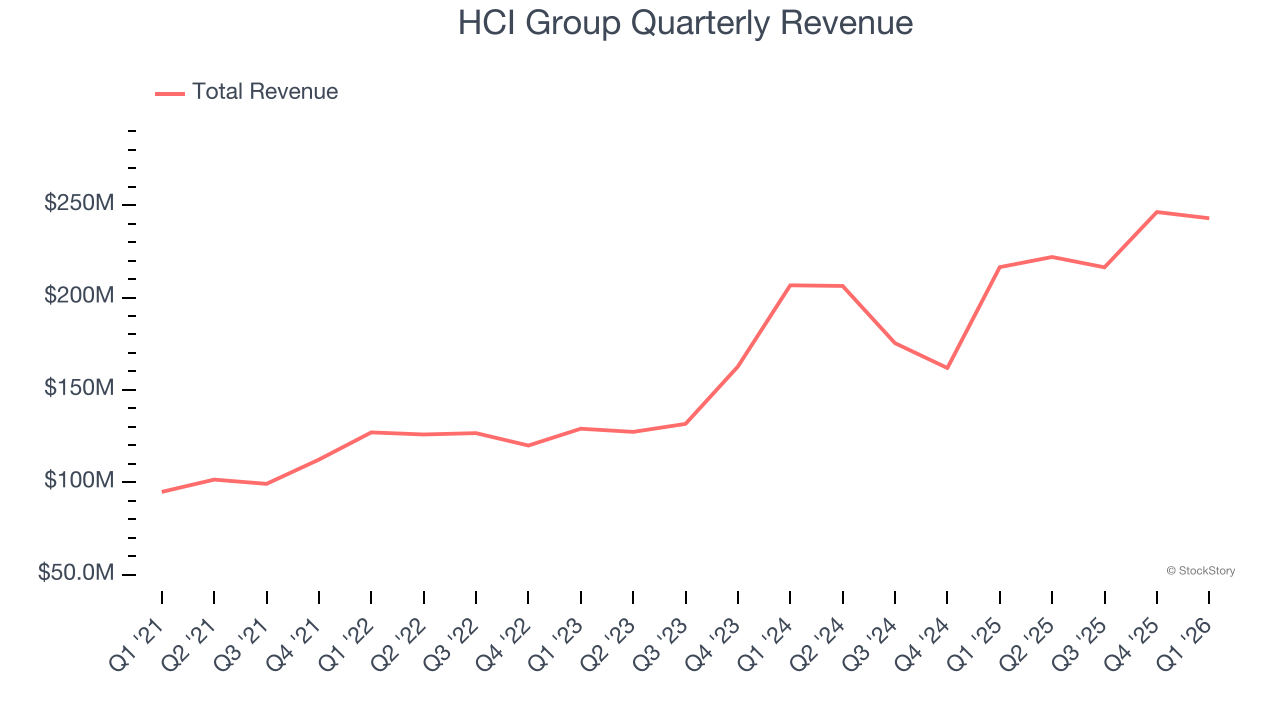

Insurance and technology company HCI Group (NYSE:HCI) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 12.2% year on year to $242.9 million. Its GAAP profit of $5.45 per share was 10.3% above analysts’ consensus estimates.

Is now the time to buy HCI Group? Find out by accessing our full research report, it’s free.

HCI Group (HCI) Q1 CY2026 Highlights:

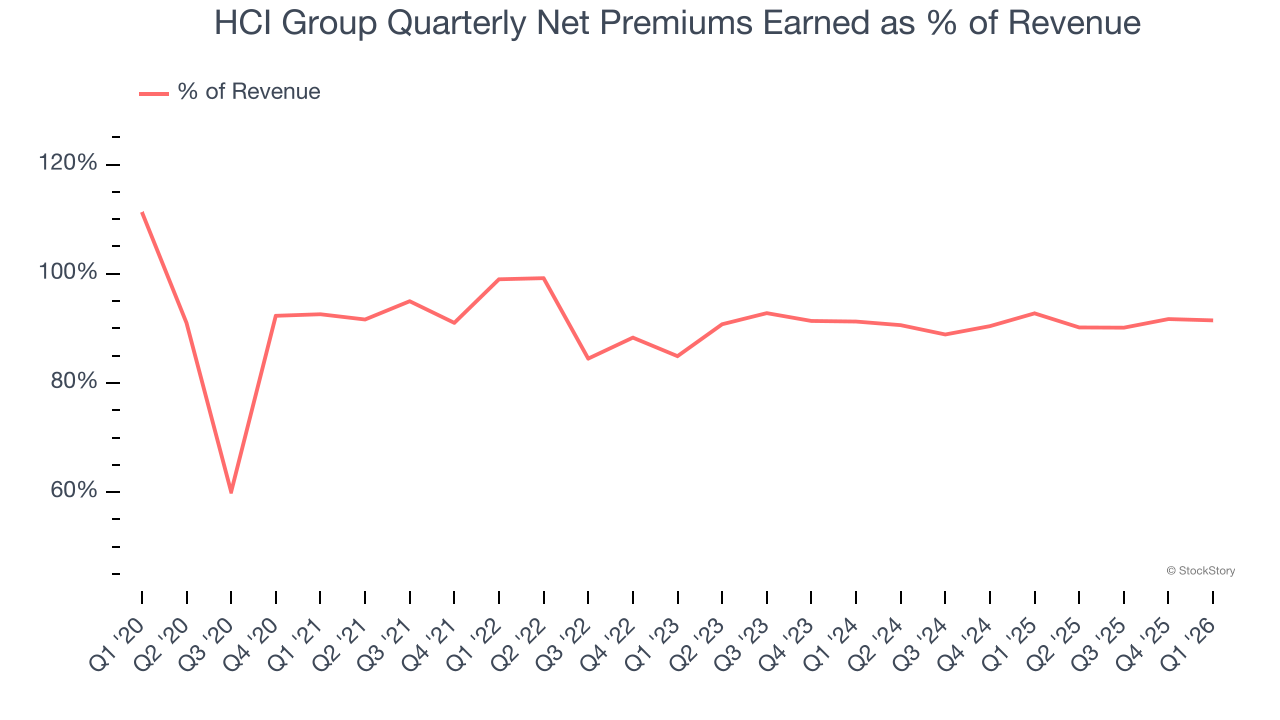

- Net Premiums Earned: $222.2 million vs analyst estimates of $218.9 million (10.7% year-on-year growth, 1.5% beat)

- Revenue: $242.9 million vs analyst estimates of $245.5 million (12.2% year-on-year growth, 1.1% miss)

- Pre-tax Profit: $115.4 million (47.5% margin)

- EPS (GAAP): $5.45 vs analyst estimates of $4.94 (10.3% beat)

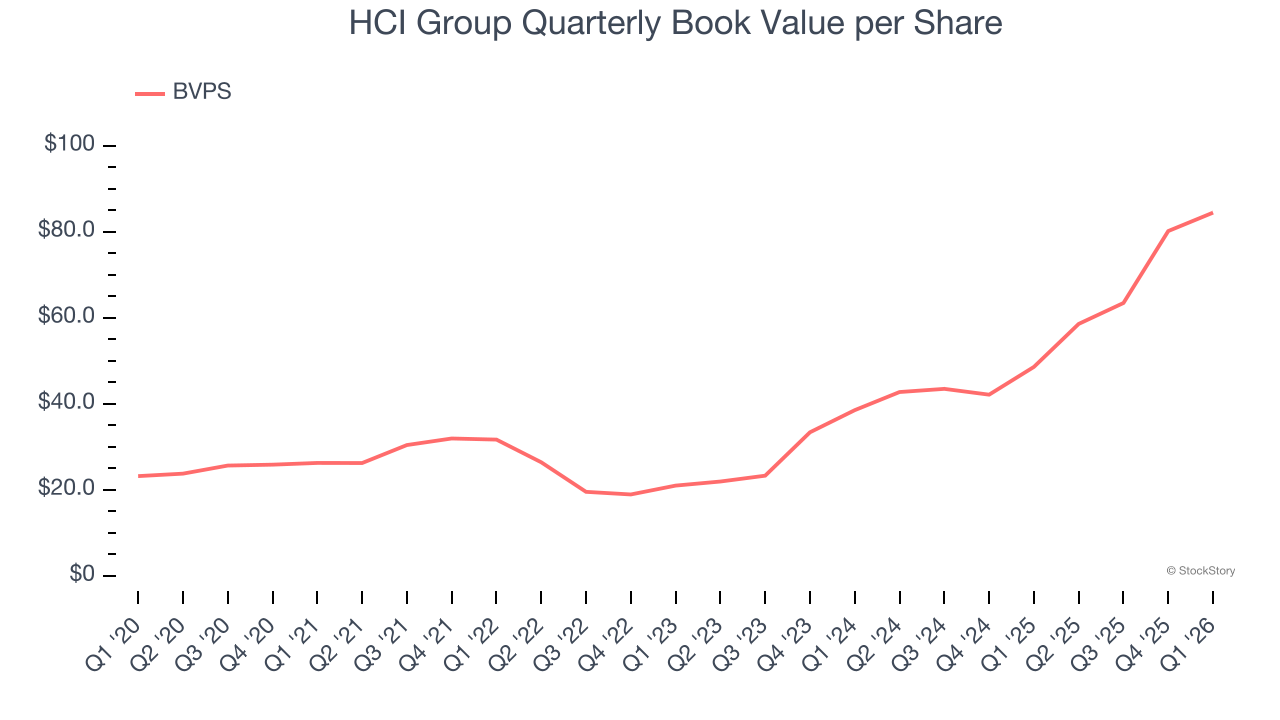

- Book Value per Share: $84.41 vs analyst estimates of $81.50 (73.9% year-on-year growth, 3.6% beat)

- Market Capitalization: $2.01 billion

Management Commentary“HCI Group had an excellent start to 2026, delivering record first quarter results for earned premiums, net income and earnings per share,” said HCI Group Chairman and Chief Executive Officer Paresh Patel.

Company Overview

Starting as a Florida "take-out" insurer that assumed policies from the state-backed Citizens Property Insurance Corporation, HCI Group (NYSE:HCI) provides property and casualty insurance, primarily homeowners coverage, while leveraging proprietary technology to improve underwriting and claims processing.

Revenue Growth

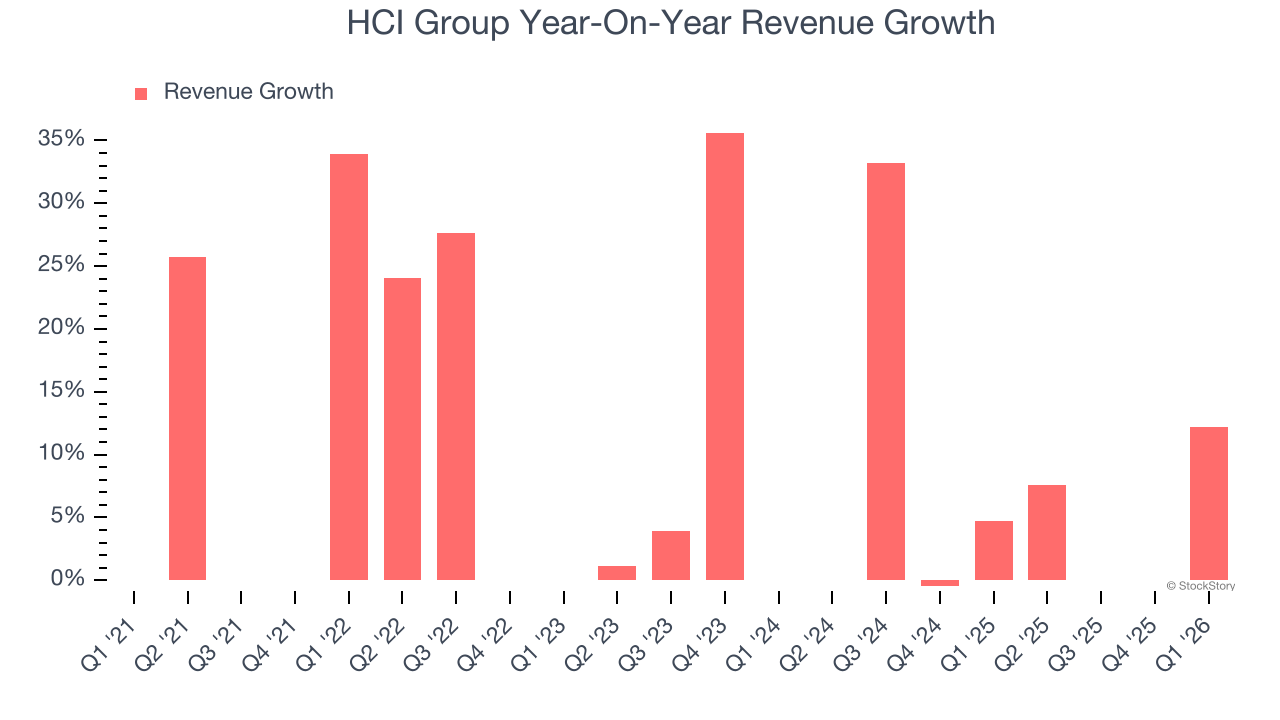

Big picture, insurers generate revenue from three key sources. The first is the core business of underwriting policies. The second source is income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services. Luckily, HCI Group’s revenue grew at an incredible 21.5% compounded annual growth rate over the last five years. Its growth surpassed the average insurance company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. HCI Group’s annualized revenue growth of 21.5% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, HCI Group’s revenue grew by 12.2% year on year to $242.9 million but fell short of Wall Street’s estimates.

Net premiums earned made up 91.2% of the company’s total revenue during the last five years, meaning HCI Group lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Our experience and research show the market cares primarily about an insurer’s net premiums earned growth as investment and fee income are considered more susceptible to market volatility and economic cycles.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

HCI Group’s BVPS grew at an incredible 26.3% annual clip over the last five years. BVPS growth has also accelerated recently, growing by 48.1% annually over the last two years from $38.50 to $84.41 per share.

Over the next 12 months, Consensus estimates call for HCI Group’s BVPS to grow by 15.5% to $81.50, top-notch growth rate.

Key Takeaways from HCI Group’s Q1 Results

We enjoyed seeing HCI Group beat analysts’ book value per share expectations this quarter. We were also glad its net premiums earned outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $154.07 immediately after reporting.

Sure, HCI Group had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).