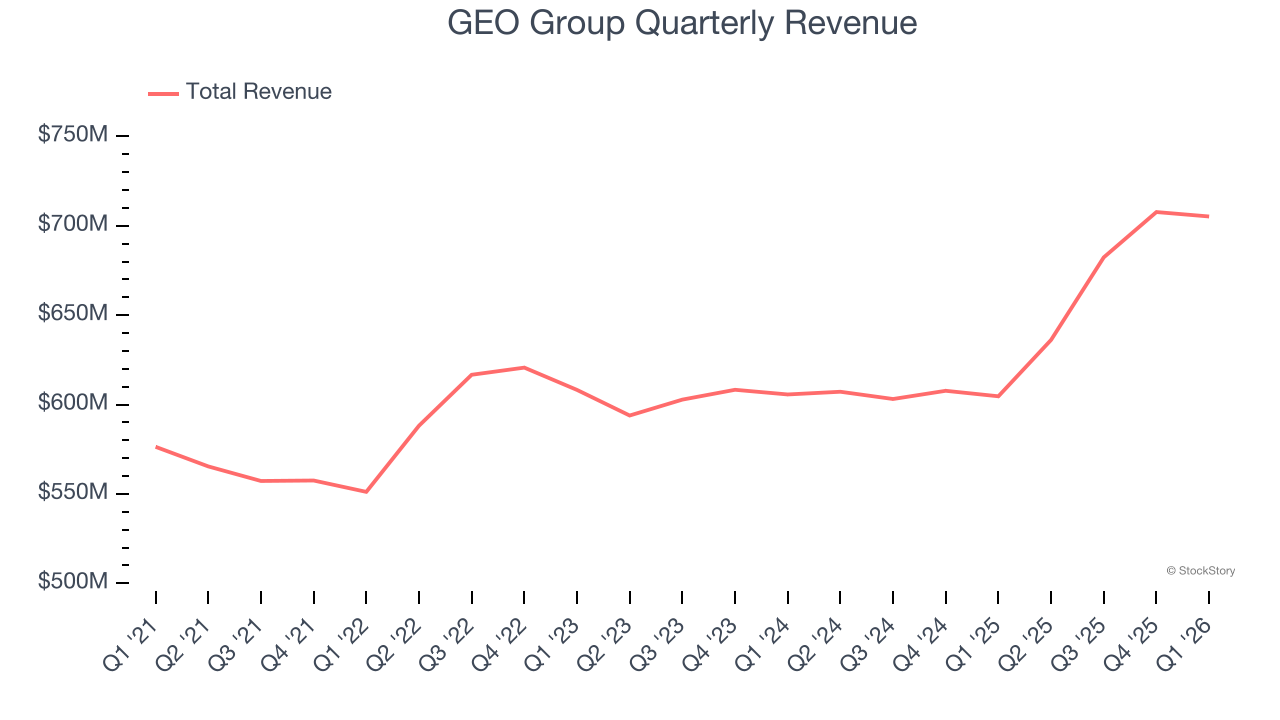

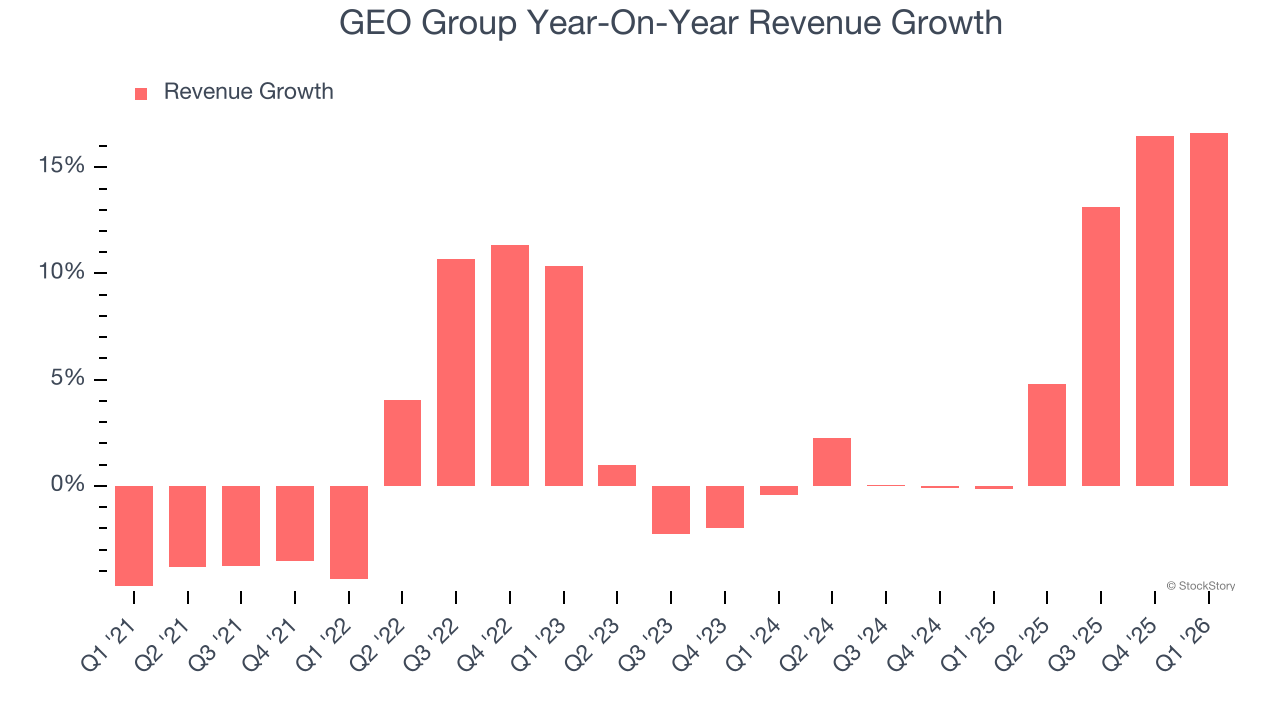

Private corrections company GEO Group (NYSE:GEO) announced better-than-expected revenue in Q1 CY2026, with sales up 16.6% year on year to $705.2 million. The company expects next quarter’s revenue to be around $720 million, close to analysts’ estimates. Its GAAP profit of $0.29 per share was 52.5% above analysts’ consensus estimates.

Is now the time to buy GEO Group? Find out by accessing our full research report, it’s free.

GEO Group (GEO) Q1 CY2026 Highlights:

- Revenue: $705.2 million vs analyst estimates of $692.7 million (16.6% year-on-year growth, 1.8% beat)

- EPS (GAAP): $0.29 vs analyst estimates of $0.19 (52.5% beat)

- Adjusted EBITDA: $131.4 million vs analyst estimates of $109.9 million (18.6% margin, 19.5% beat)

- The company slightly lifted its revenue guidance for the full year to $3.03 million at the midpoint from $3 million

- EPS (GAAP) guidance for the full year is $1.20 at the midpoint, beating analyst estimates by 3.2%

- EBITDA guidance for the full year is $535 million at the midpoint, above analyst estimates of $515.7 million

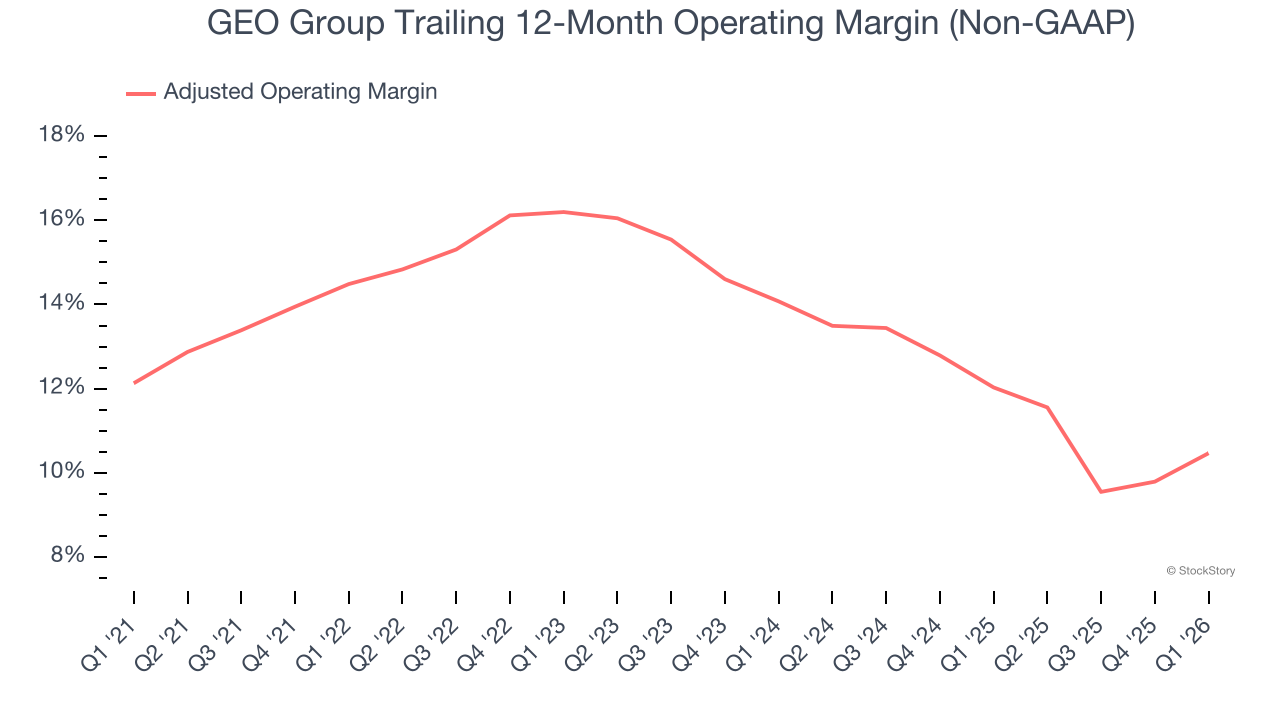

- Operating Margin: 12.7%, up from 10.1% in the same quarter last year

- Market Capitalization: $2.44 billion

Company Overview

With a global footprint spanning three continents and approximately 81,000 beds across 100 facilities, GEO Group (NYSE:GEO) operates secure facilities, processing centers, and reentry services for government agencies in the United States, Australia, and South Africa.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $2.73 billion in revenue over the past 12 months, GEO Group is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, GEO Group’s sales grew at a tepid 3.3% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. GEO Group’s annualized revenue growth of 6.4% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, GEO Group reported year-on-year revenue growth of 16.6%, and its $705.2 million of revenue exceeded Wall Street’s estimates by 1.8%. Company management is currently guiding for a 13.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.6% over the next 12 months, an improvement versus the last two years. This projection is admirable and suggests its newer products and services will spur better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

GEO Group has managed its cost base well over the last five years. It demonstrated solid profitability for a business services business, producing an average adjusted operating margin of 13.4%.

Analyzing the trend in its profitability, GEO Group’s adjusted operating margin decreased by 4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, GEO Group generated an adjusted operating margin profit margin of 12.7%, up 2.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

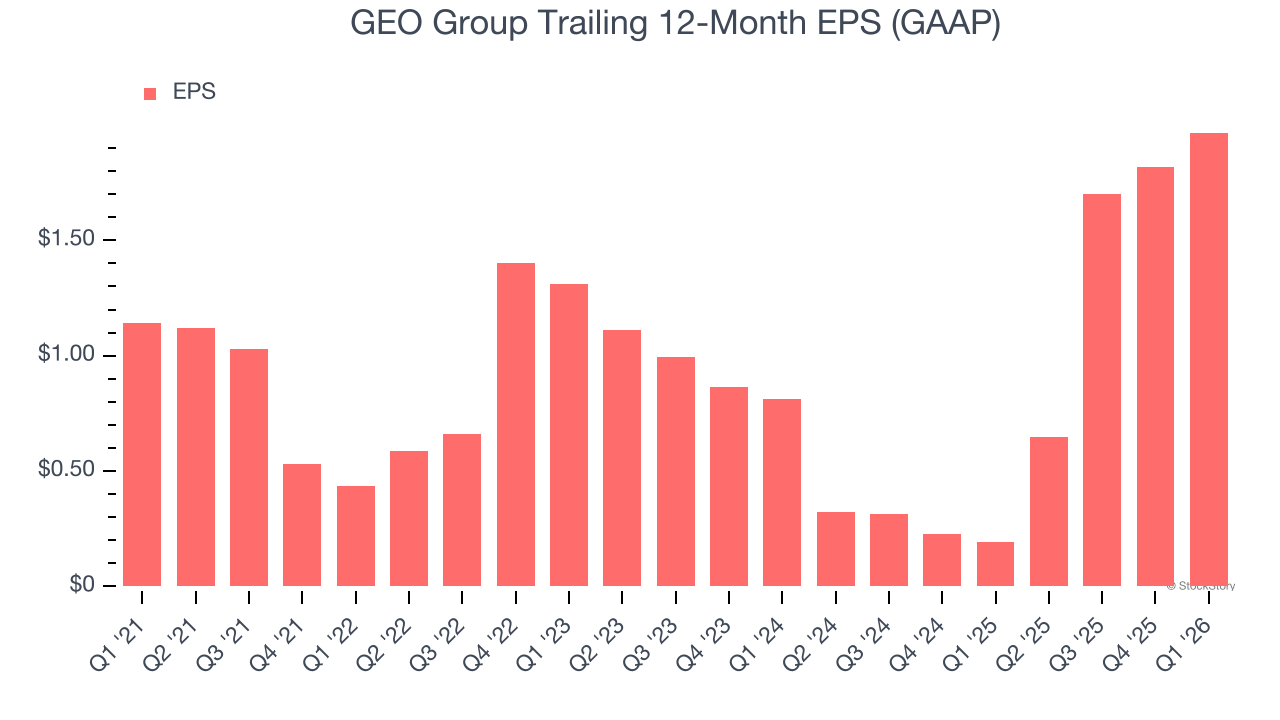

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

GEO Group’s EPS grew at 11.5% compounded annual growth rate over the last five years, higher than its 3.3% annualized revenue growth. However, we take this with a grain of salt because its adjusted operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For GEO Group, its two-year annual EPS growth of 55.5% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, GEO Group reported EPS of $0.29, up from $0.14 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from GEO Group’s Q1 Results

It was good to see GEO Group beat analysts’ EPS expectations this quarter. We were also glad its full-year EPS guidance outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its revenue guidance for next quarter was in line with Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 14.3% to $20.99 immediately following the results.

Is GEO Group an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).