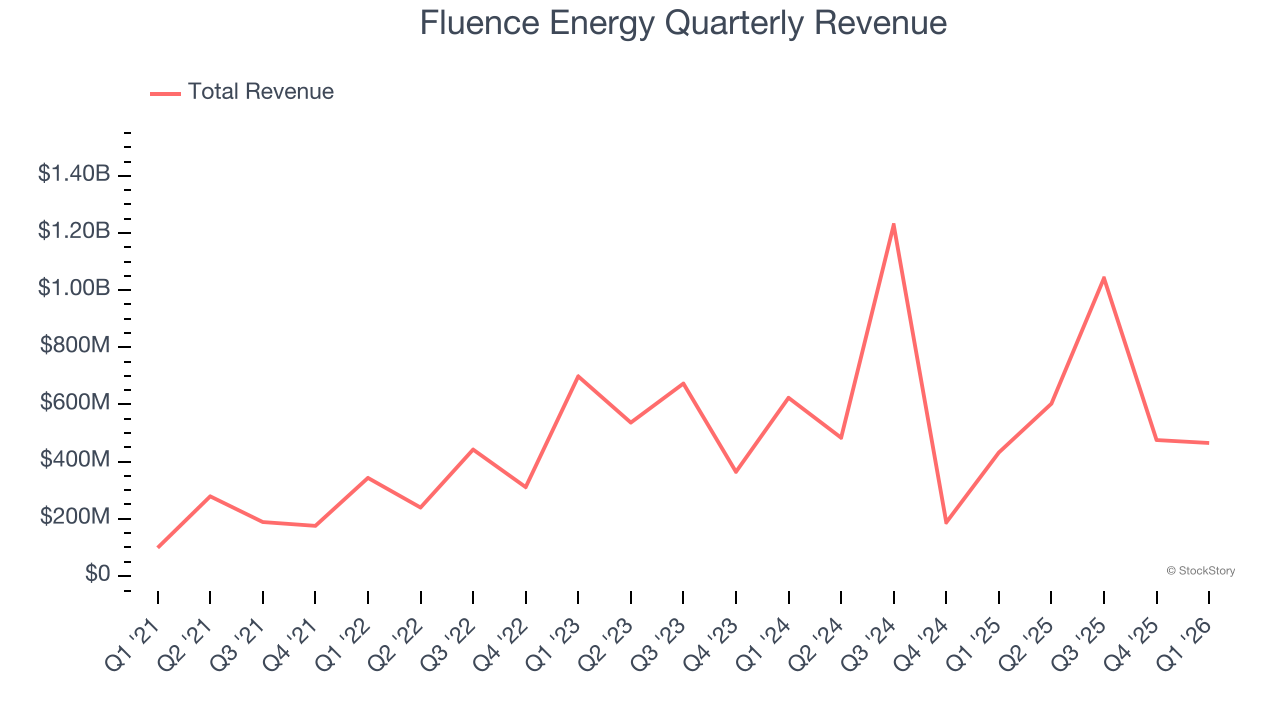

Electricity storage and software provider Fluence (NASDAQ:FLNC) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 7.7% year on year to $464.9 million. On the other hand, the company’s full-year revenue guidance of $3.4 billion at the midpoint came in 1.1% above analysts’ estimates. Its GAAP loss of $0.16 per share was in line with analysts’ consensus estimates.

Is now the time to buy Fluence Energy? Find out by accessing our full research report, it’s free.

Fluence Energy (FLNC) Q1 CY2026 Highlights:

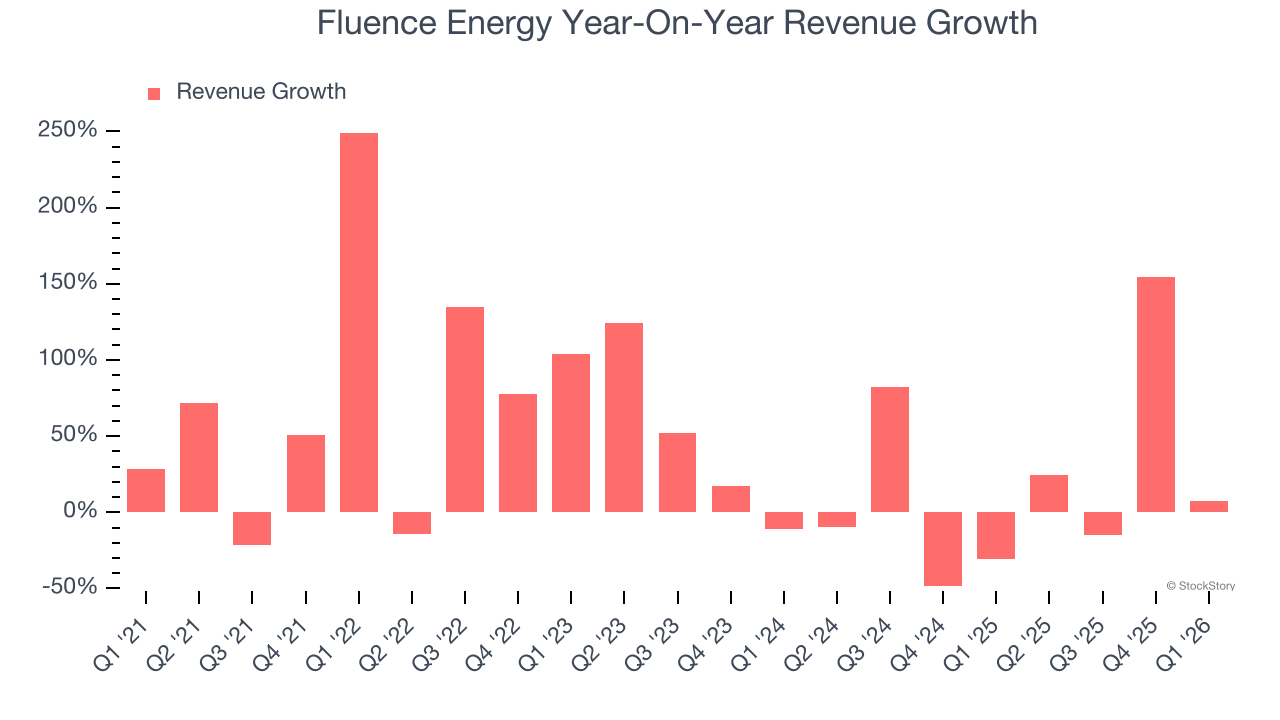

- Revenue: $464.9 million vs analyst estimates of $611.5 million (7.7% year-on-year growth, 24% miss)

- EPS (GAAP): -$0.16 vs analyst estimates of -$0.17 (in line)

- Adjusted EBITDA: -$9.44 million (-2% margin, 69% year-on-year growth)

- The company reconfirmed its revenue guidance for the full year of $3.4 billion at the midpoint

- EBITDA guidance for the full year is $50 million at the midpoint, above analyst estimates of $48.4 million

- Adjusted EBITDA Margin: -2%, up from -7% in the same quarter last year

- Free Cash Flow was -$127.9 million compared to -$53.76 million in the same quarter last year

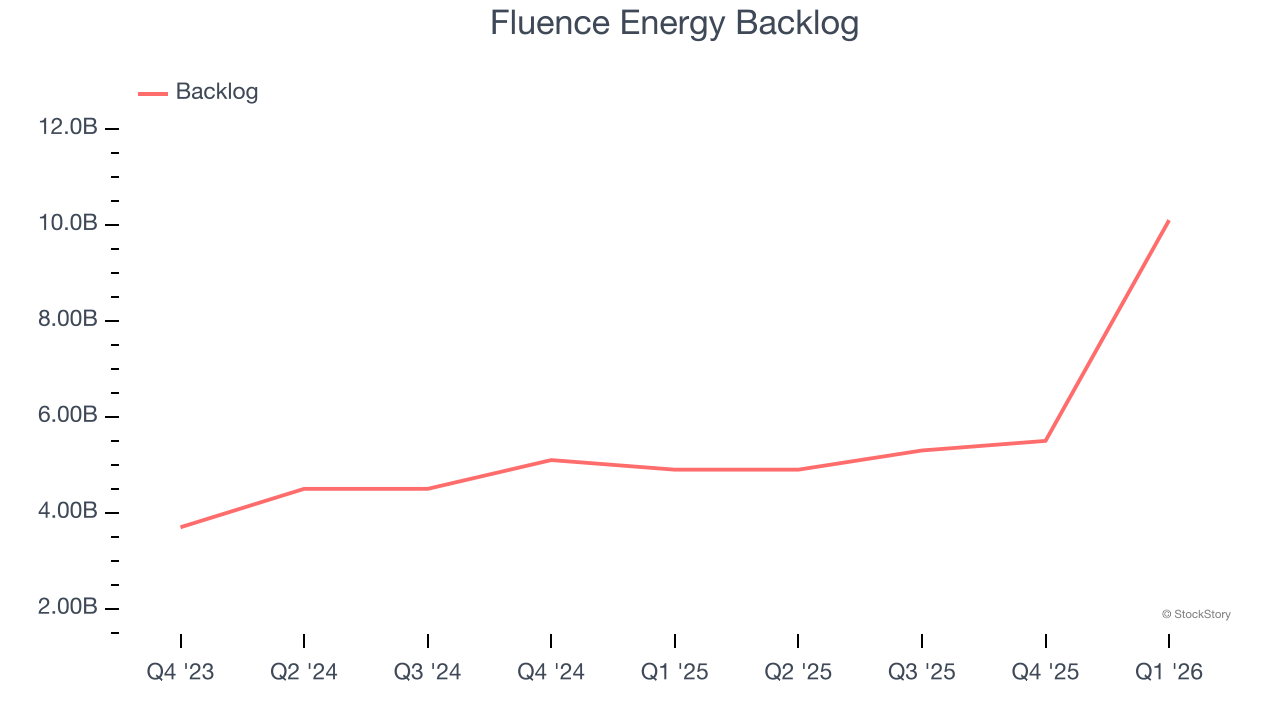

- Backlog: $10.1 billion at quarter end, up 106% year on year

- Market Capitalization: $1.68 billion

"We are beginning to see the benefit of our pipeline growth with an acceleration of orders over the past few months and backlog reaching another record level. We also reached substantial completion on our first delivery of Smartstack and affirmed access to our domestic content offering in the U.S.," said Julian Nebreda, the Company's President and Chief Executive Officer.

Company Overview

Pioneering the use of lithium-ion batteries for grid storage, Fluence (NASDAQ:FLNC) helps store renewable energy sources with battery systems.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Fluence Energy’s sales grew at an incredible 33.2% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Fluence Energy’s annualized revenue growth of 8.5% over the last two years is below its five-year trend, but we still think the results were respectable.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Fluence Energy’s backlog reached $10.1 billion in the latest quarter and averaged 35.7% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Fluence Energy’s products and services but raises concerns about capacity constraints.

This quarter, Fluence Energy’s revenue grew by 7.7% year on year to $464.9 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 42.7% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will fuel better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

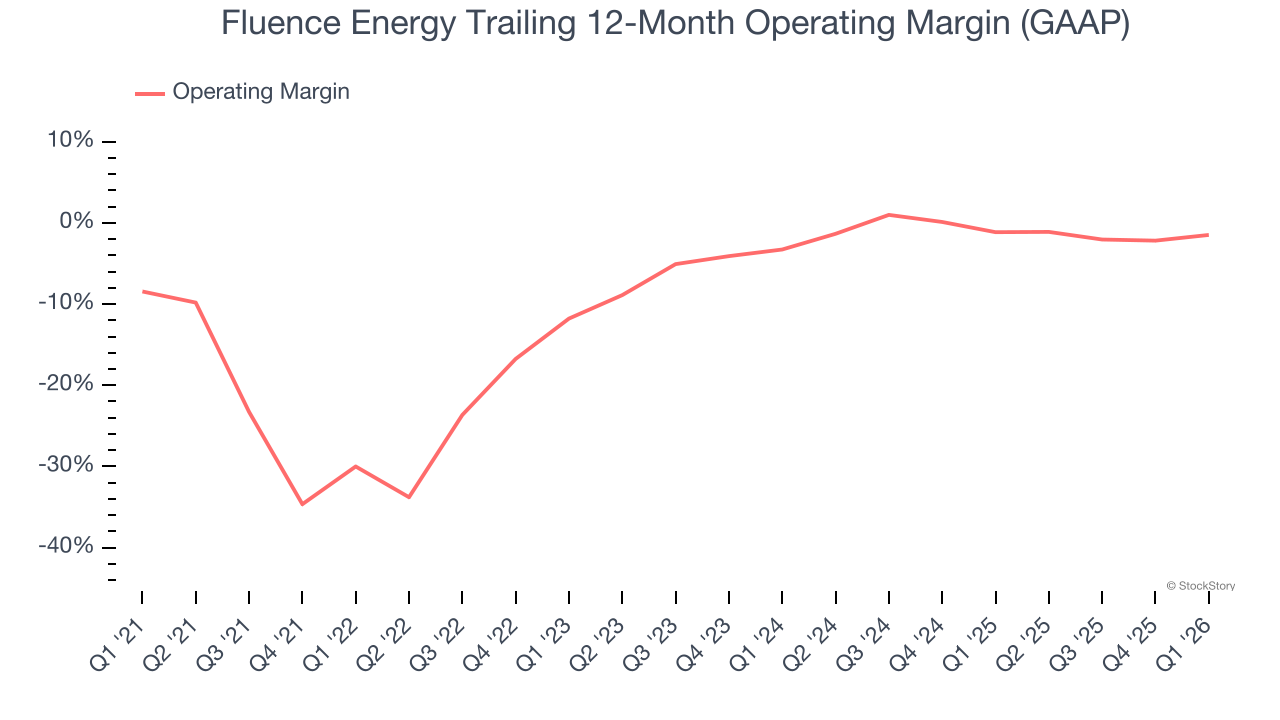

Fluence Energy’s high expenses have contributed to an average operating margin of negative 6.5% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Fluence Energy’s operating margin rose by 28.5 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q1, Fluence Energy generated a negative 6% operating margin.

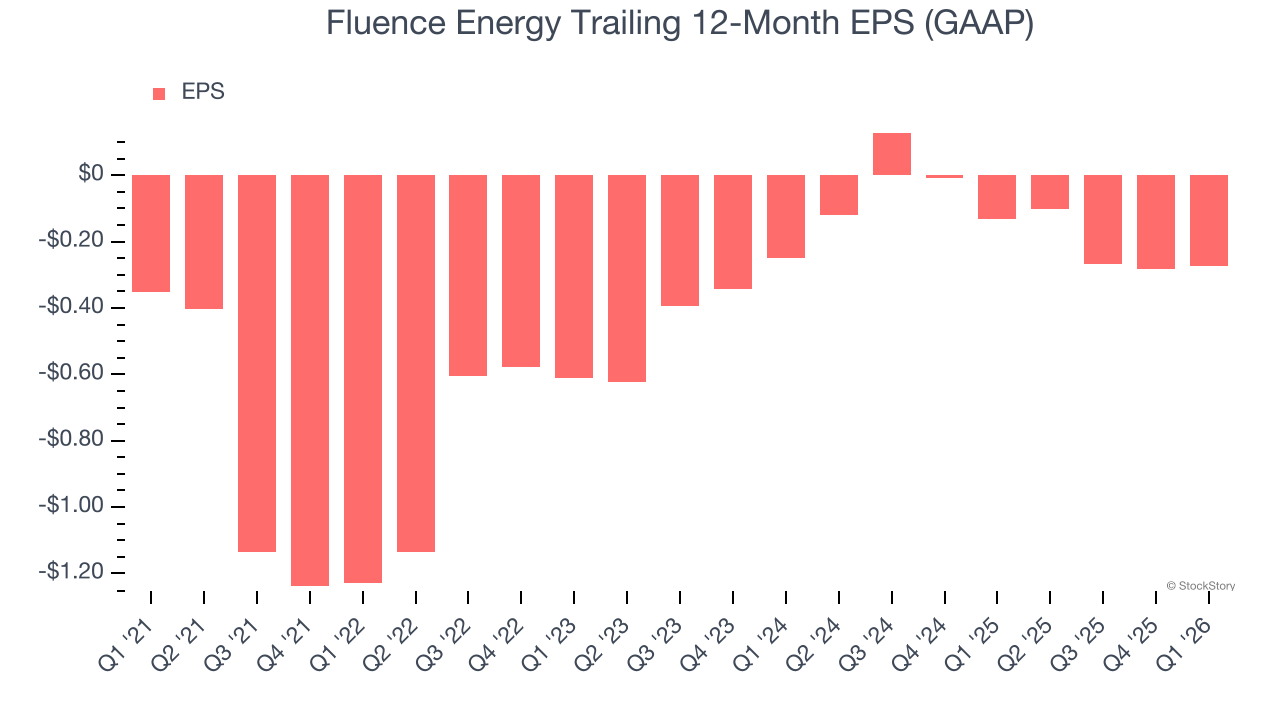

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Fluence Energy’s full-year earnings are still negative, it reduced its losses and improved its EPS by 5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Fluence Energy, its two-year annual EPS declines of 4.5% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, Fluence Energy reported EPS of negative $0.16, up from negative $0.17 in the same quarter last year. This print beat analysts’ estimates by 3.5%. Over the next 12 months, Wall Street is optimistic. Analysts forecast Fluence Energy’s full-year EPS of negative $0.27 will flip to positive $0.08.

Key Takeaways from Fluence Energy’s Q1 Results

We were impressed by how significantly Fluence Energy blew past analysts’ EBITDA expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 20.6% to $16.41 immediately after reporting.

Fluence Energy may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).