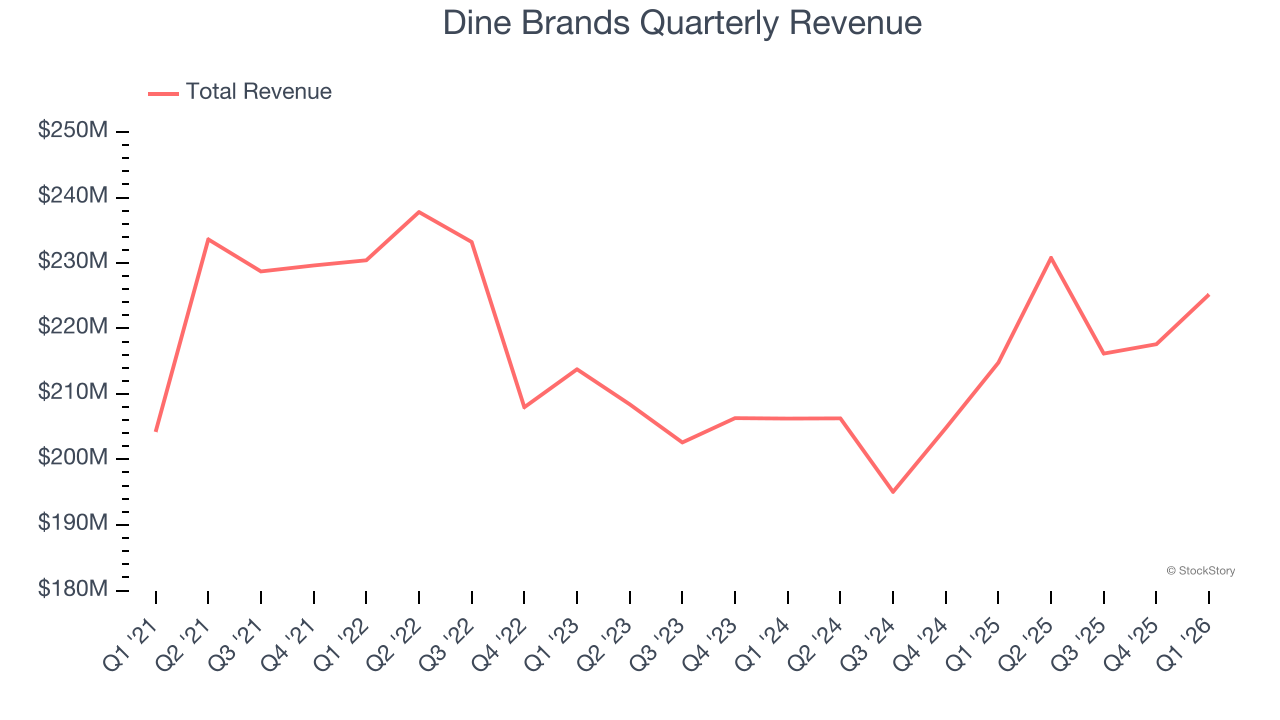

Casual restaurant chain Dine Brands (NYSE:DIN) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 4.9% year on year to $225.2 million. Its non-GAAP profit of $1.07 per share was 6.6% above analysts’ consensus estimates.

Is now the time to buy Dine Brands? Find out by accessing our full research report, it’s free.

Dine Brands (DIN) Q1 CY2026 Highlights:

- Revenue: $225.2 million vs analyst estimates of $221.2 million (4.9% year-on-year growth, 1.8% beat)

- Adjusted EPS: $1.07 vs analyst estimates of $1.00 (6.6% beat)

- Adjusted EBITDA: $50.8 million vs analyst estimates of $52.36 million (22.6% margin, 3% miss)

- EBITDA guidance for the full year is $225 million at the midpoint, above analyst estimates of $221.6 million

- Operating Margin: 62.4%, up from 18.1% in the same quarter last year

- Free Cash Flow was -$3 million, down from $12.81 million in the same quarter last year

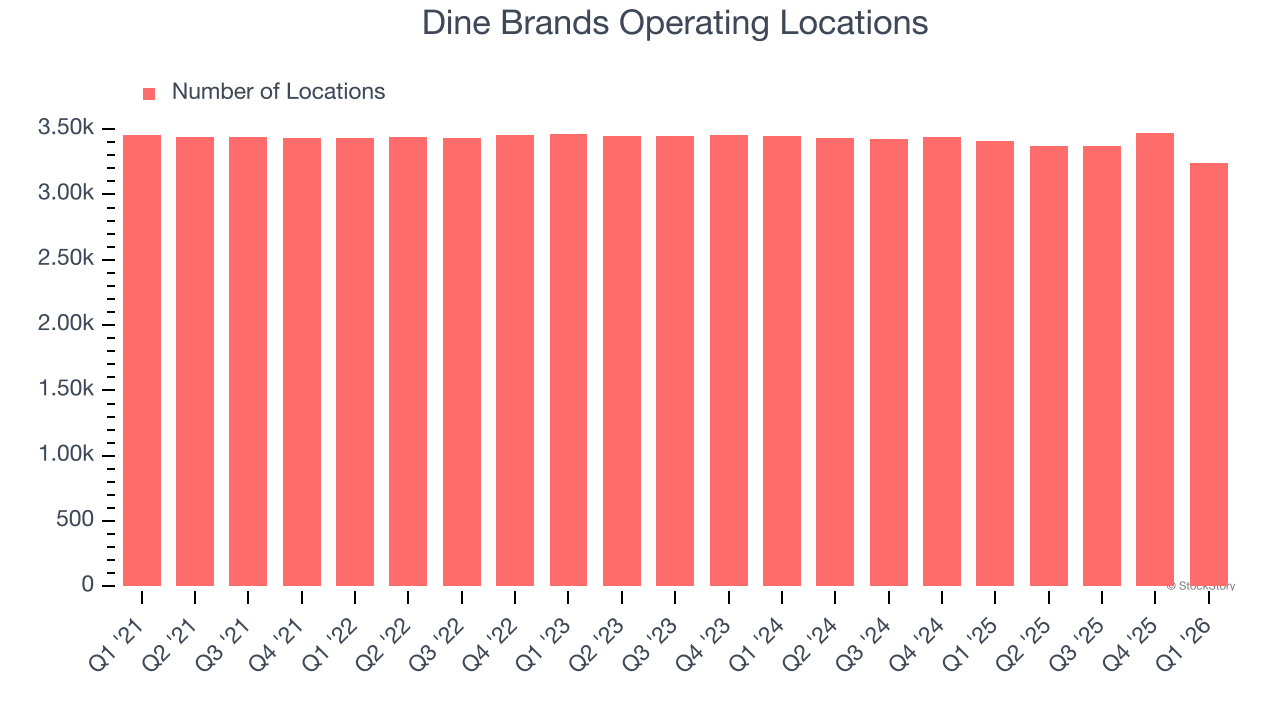

- Locations: 3,243 at quarter end, down from 3,408 in the same quarter last year

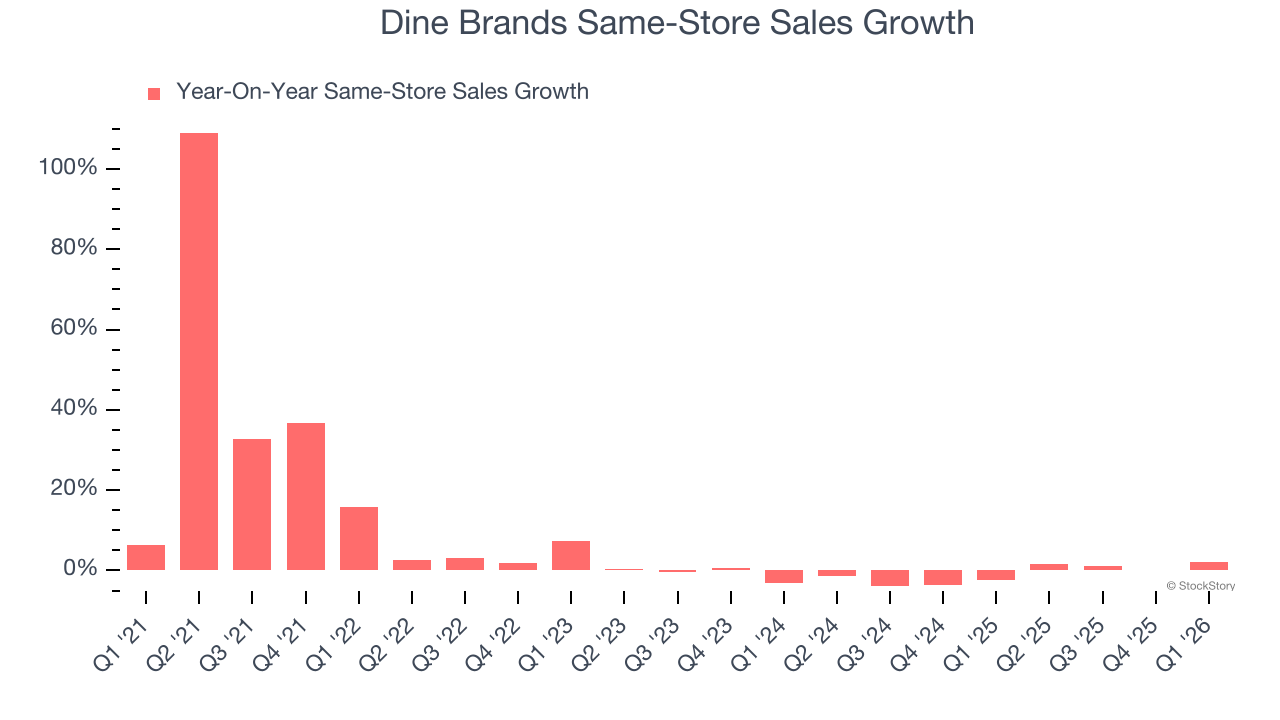

- Same-Store Sales rose 1.9% year on year (-2.4% in the same quarter last year)

- Market Capitalization: $365.4 million

Company Overview

Operating a franchise model, Dine Brands (NYSE:DIN) is a casual restaurant chain that owns the Applebee’s and IHOP banners.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $889.8 million in revenue over the past 12 months, Dine Brands is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Dine Brands struggled to increase demand as its $889.8 million of sales for the trailing 12 months was close to its revenue seven years ago. This was mainly because it closed restaurants.

This quarter, Dine Brands reported modest year-on-year revenue growth of 4.9% but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 1.4% over the next 12 months, similar to its seven-year rate. This projection doesn't excite us and indicates its newer menu offerings will not catalyze better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Dine Brands listed 3,243 locations in the latest quarter and has generally closed its restaurants over the last two years, averaging 1.2% annual declines.

When a chain shutters restaurants, it usually means demand for its meals is waning, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Dine Brands’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Dine Brands is attempting to boost same-store sales by closing restaurants (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Dine Brands’s same-store sales rose 1.9% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

Key Takeaways from Dine Brands’s Q1 Results

We were impressed by how significantly Dine Brands blew past analysts’ same-store sales expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EBITDA missed. Overall, this print had some key positives. The stock traded up 1.2% to $28.50 immediately following the results.

Sure, Dine Brands had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).