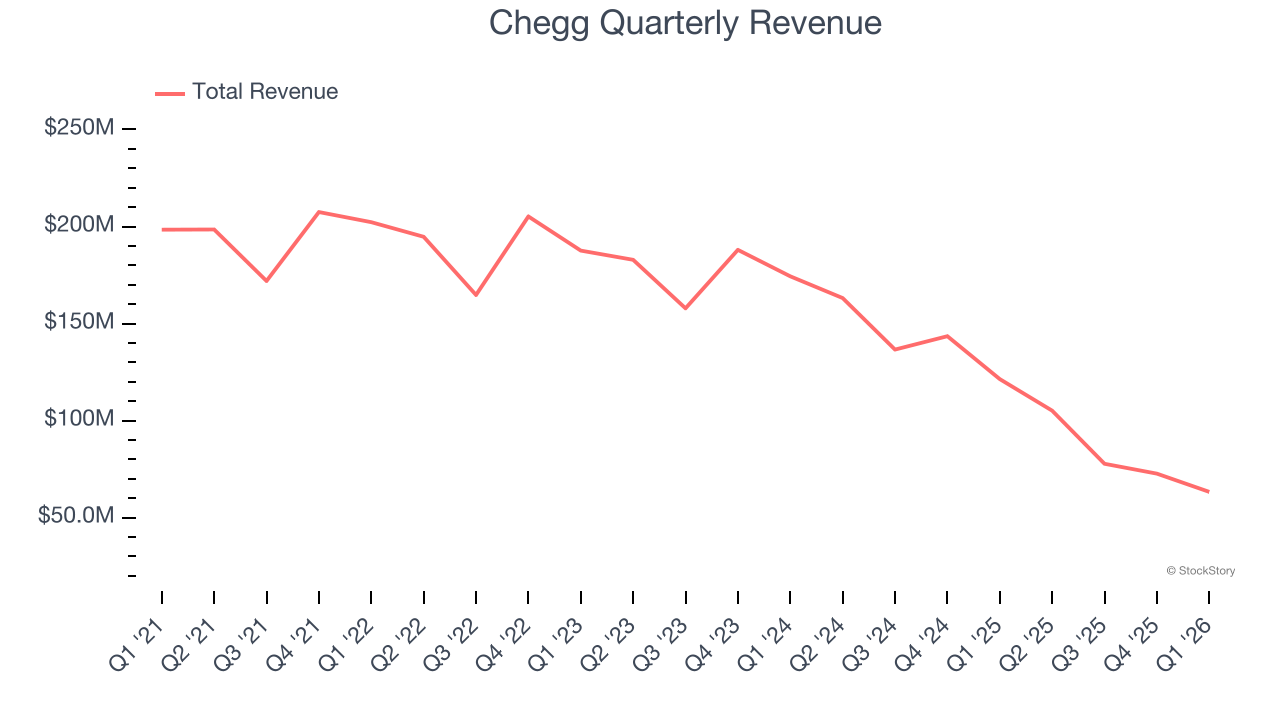

Online study and academic help platform Chegg (NYSE:CHGG) reported Q1 CY2026 results exceeding the market’s revenue expectations, but sales fell by 47.9% year on year to $63.26 million. On the other hand, next quarter’s revenue guidance of $49.5 million was less impressive, coming in 15.6% below analysts’ estimates. Its non-GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Chegg? Find out by accessing our full research report, it’s free.

Chegg (CHGG) Q1 CY2026 Highlights:

- Revenue: $63.26 million vs analyst estimates of $61 million (47.9% year-on-year decline, 3.7% beat)

- Adjusted EPS: $0.03 vs analyst estimates of -$0.02 (significant beat)

- Adjusted EBITDA: $15.46 million vs analyst estimates of $11.75 million (24.4% margin, 31.5% beat)

- Revenue Guidance for Q2 CY2026 is $49.5 million at the midpoint, below analyst estimates of $58.64 million

- EBITDA guidance for Q2 CY2026 is $5.5 million at the midpoint, below analyst estimates of $8.85 million

- Operating Margin: -1.6%, up from -6.5% in the same quarter last year

- Free Cash Flow was $3.06 million, up from -$15.48 million in the previous quarter

- Market Capitalization: $138.6 million

Company Overview

Started as a physical textbook rental service, Chegg (NYSE:CHGG) is now a digital platform addressing student pain points by providing study and academic assistance.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Chegg struggled to consistently generate demand over the last three years as its sales dropped at a 24.9% annual rate. This wasn’t a great result and is a sign of poor business quality.

This quarter, Chegg’s revenue fell by 47.9% year on year to $63.26 million but beat Wall Street’s estimates by 3.7%. Company management is currently guiding for a 52.9% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 36.9% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

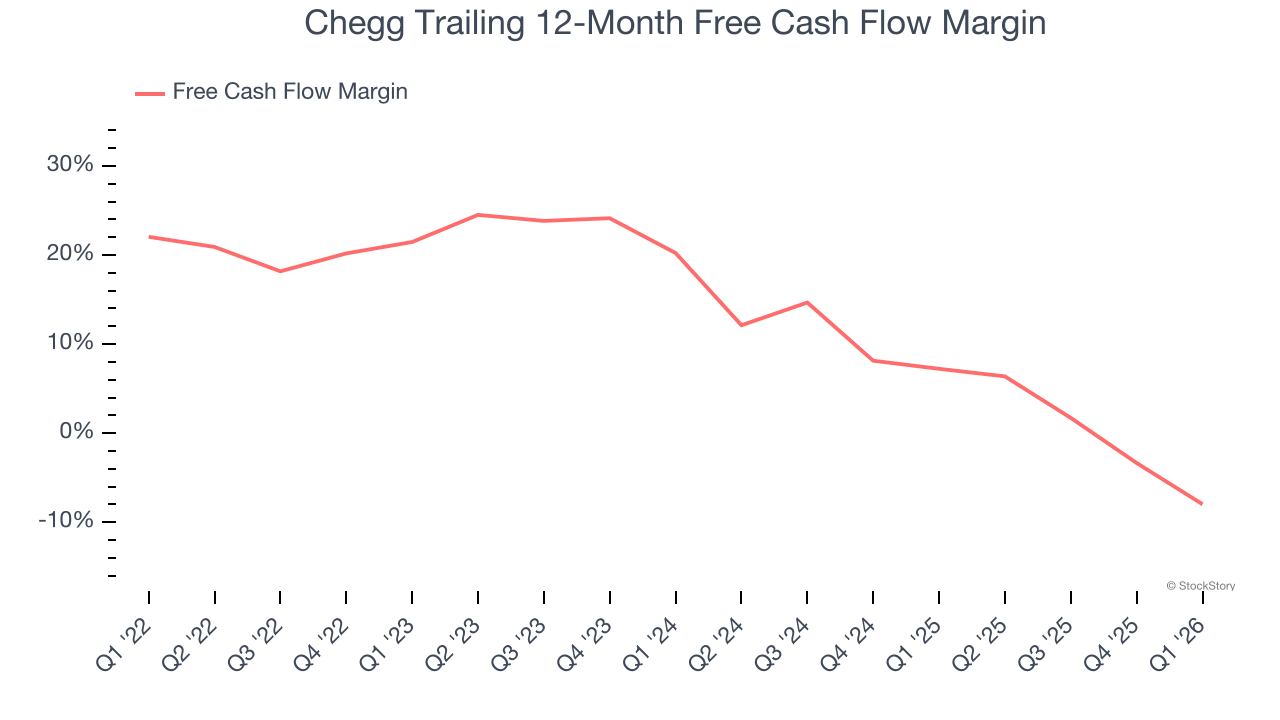

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Chegg has shown weak cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.7%, below what we’d expect for a consumer internet business. The divergence from its good EBITDA margin stems from its capital-intensive business model, which requires Chegg to make large cash investments in working capital (i.e., stocking inventories) and capital expenditures (i.e., building new facilities).

Taking a step back, we can see that Chegg’s margin dropped by 29.4 percentage points over the last few years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Chegg’s free cash flow clocked in at $3.06 million in Q1, equivalent to a 4.8% margin. The company’s cash profitability regressed as it was 8.2 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

Key Takeaways from Chegg’s Q1 Results

We were impressed by how significantly Chegg blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 11.6% to $1.03 immediately following the results.

Chegg’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).