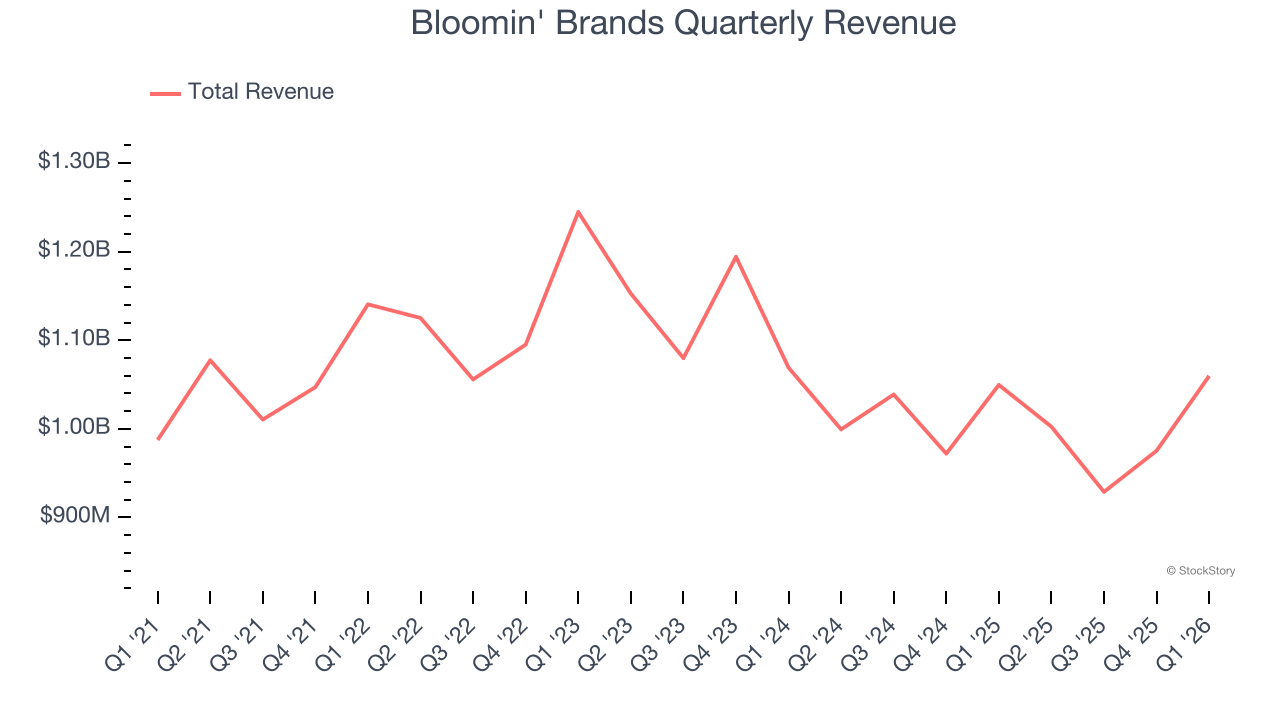

Restaurant company Bloomin’ Brands (NASDAQ:BLMN) reported Q1 CY2026 results exceeding the market’s revenue expectations, but sales were flat year on year at $1.06 billion. Its non-GAAP profit of $0.67 per share was 18.4% above analysts’ consensus estimates.

Is now the time to buy Bloomin' Brands? Find out by accessing our full research report, it’s free.

Bloomin' Brands (BLMN) Q1 CY2026 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $1.04 billion (flat year on year, 1.6% beat)

- Adjusted EPS: $0.67 vs analyst estimates of $0.57 (18.4% beat)

- Adjusted EBITDA: $105.4 million vs analyst estimates of $101.6 million (9.9% margin, 3.8% beat)

- Adjusted EPS guidance for Q2 CY2026 is $0.30 at the midpoint, above analyst estimates of $0.22

- Operating Margin: 5.6%, in line with the same quarter last year

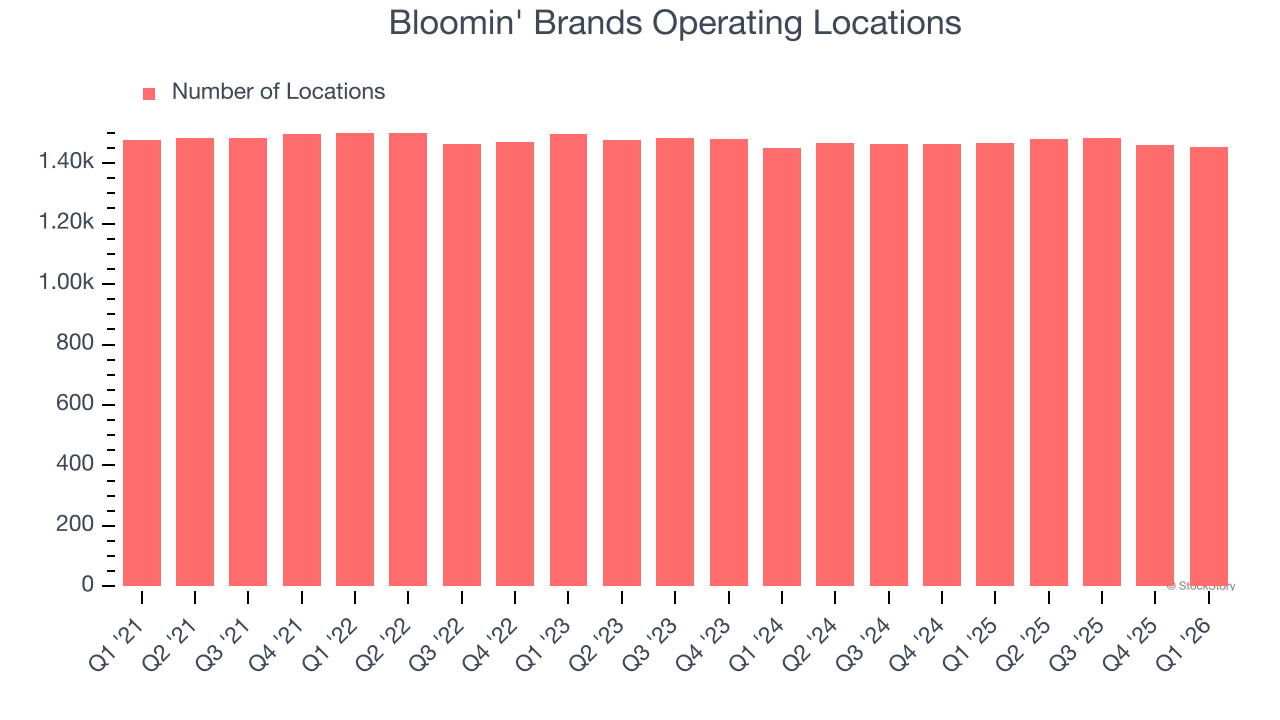

- Locations: 1,452 at quarter end, down from 1,465 in the same quarter last year

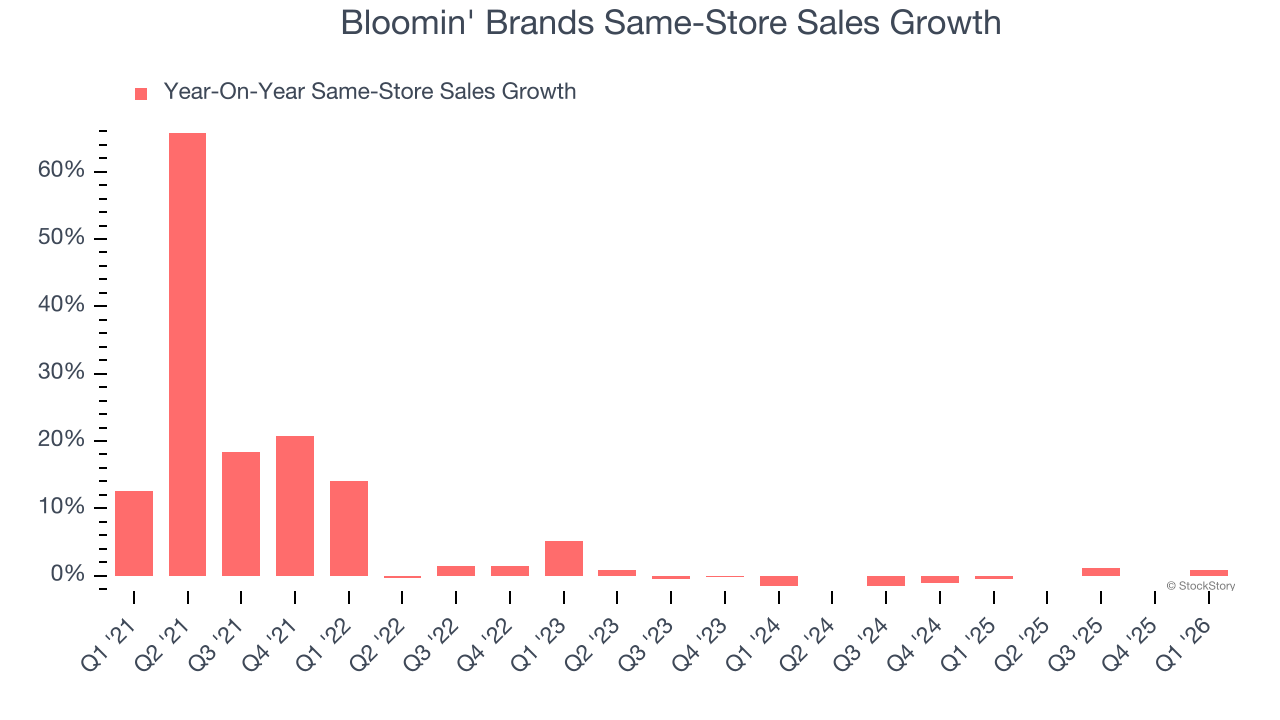

- Same-Store Sales were flat year on year (-0.5% in the same quarter last year)

- Market Capitalization: $491 million

Company Overview

Owner of the iconic Australian-themed Outback Steakhouse, Bloomin’ Brands (NASDAQ:BLMN) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $3.97 billion in revenue over the past 12 months, Bloomin' Brands is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing restaurant banners have penetrated most of the market. For Bloomin' Brands to boost its sales, it likely needs to adjust its prices, launch new chains, or lean into foreign markets.

As you can see below, Bloomin' Brands struggled to increase demand as its $3.97 billion of sales for the trailing 12 months was close to its revenue seven years ago. This was mainly because it didn’t open many new restaurants.

This quarter, Bloomin' Brands’s $1.06 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and suggests its newer menu offerings will not catalyze better top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Bloomin' Brands operated 1,452 locations in the latest quarter, and over the last two years, has kept its restaurant count flat while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Bloomin' Brands’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Bloomin' Brands starts opening new restaurants to artificially boost revenue growth.

In the latest quarter, Bloomin' Brands’s year on year same-store sales were flat. This performance was more or less in line with its historical levels.

Key Takeaways from Bloomin' Brands’s Q1 Results

We were impressed by Bloomin' Brands’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 5.4% to $6.07 immediately following the results.

Sure, Bloomin' Brands had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).