Life sciences company Bio-Techne (NASDAQ:TECH) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 1.5% year on year to $311.4 million. Its non-GAAP profit of $0.53 per share was in line with analysts’ consensus estimates.

Is now the time to buy Bio-Techne? Find out by accessing our full research report, it’s free.

Bio-Techne (TECH) Q1 CY2026 Highlights:

- Revenue: $311.4 million vs analyst estimates of $316.4 million (1.5% year-on-year decline, 1.6% miss)

- Adjusted EPS: $0.53 vs analyst estimates of $0.53 (in line)

- Adjusted EBITDA: $116.7 million vs analyst estimates of $115.4 million (37.5% margin, 1.1% beat)

- Operating Margin: 24.2%, up from 12.2% in the same quarter last year

- Free Cash Flow Margin: 24.9%, up from 9.8% in the same quarter last year

- Organic Revenue fell 2% year on year (miss)

- Market Capitalization: $8.87 billion

"The Bio‑Techne team delivered solid execution amid a mixed end‑market environment," said Kim Kelderman, President and Chief Executive Officer of Bio-Techne.

Company Overview

With a catalog of hundreds of thousands of specialized biological products used in laboratories worldwide, Bio-Techne (NASDAQ:TECH) develops and manufactures specialized reagents, instruments, and services that help researchers study biological processes and enable diagnostic testing and cell therapy development.

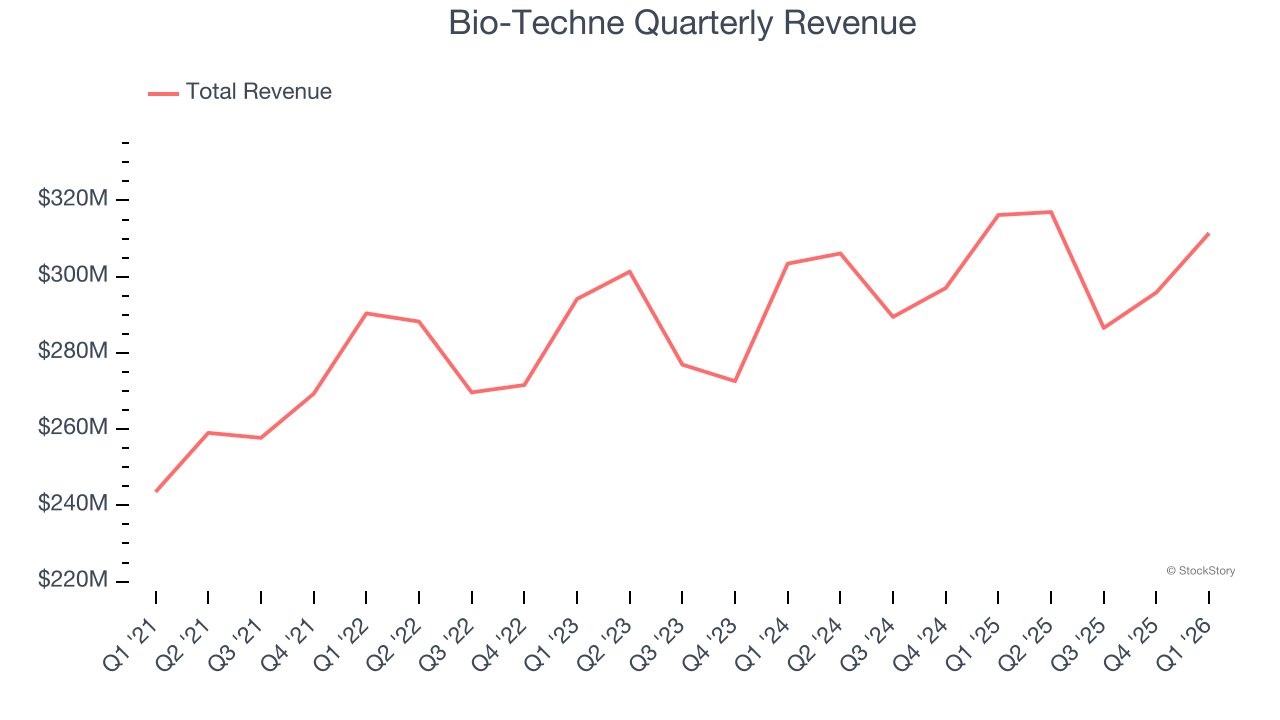

Revenue Growth

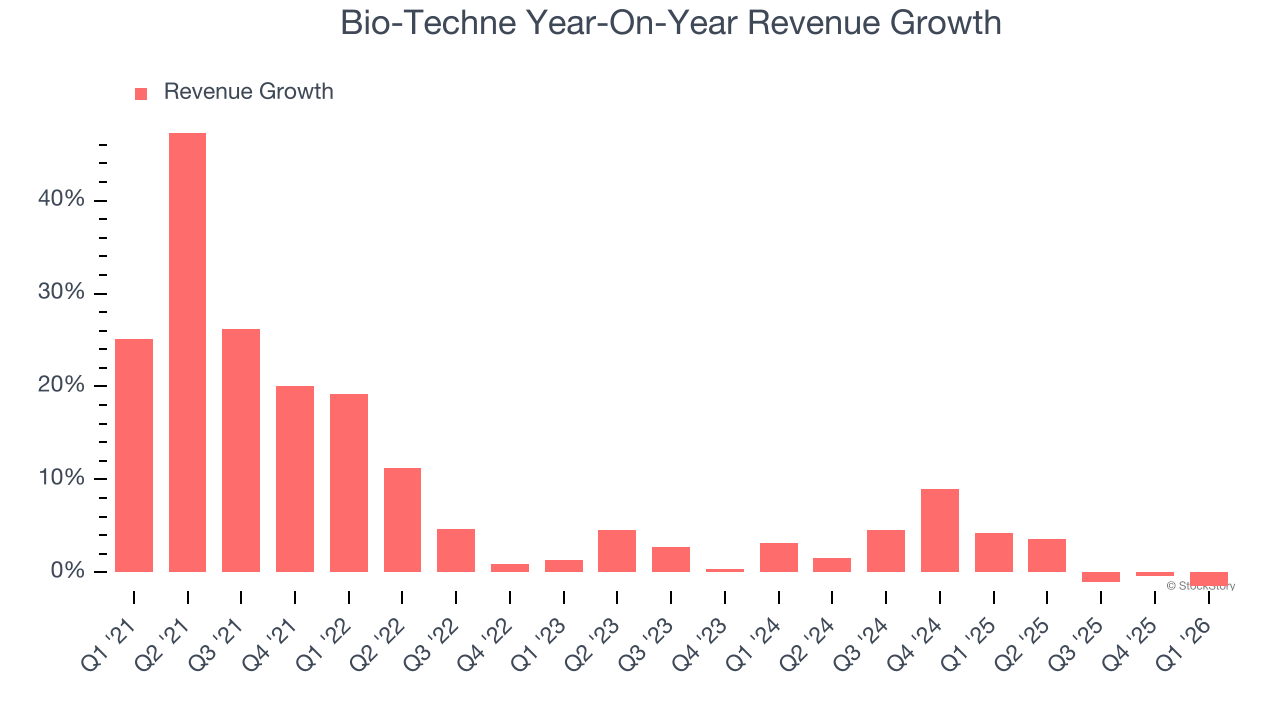

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Bio-Techne’s sales grew at a mediocre 7.4% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Bio-Techne’s recent performance shows its demand has slowed as its annualized revenue growth of 2.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

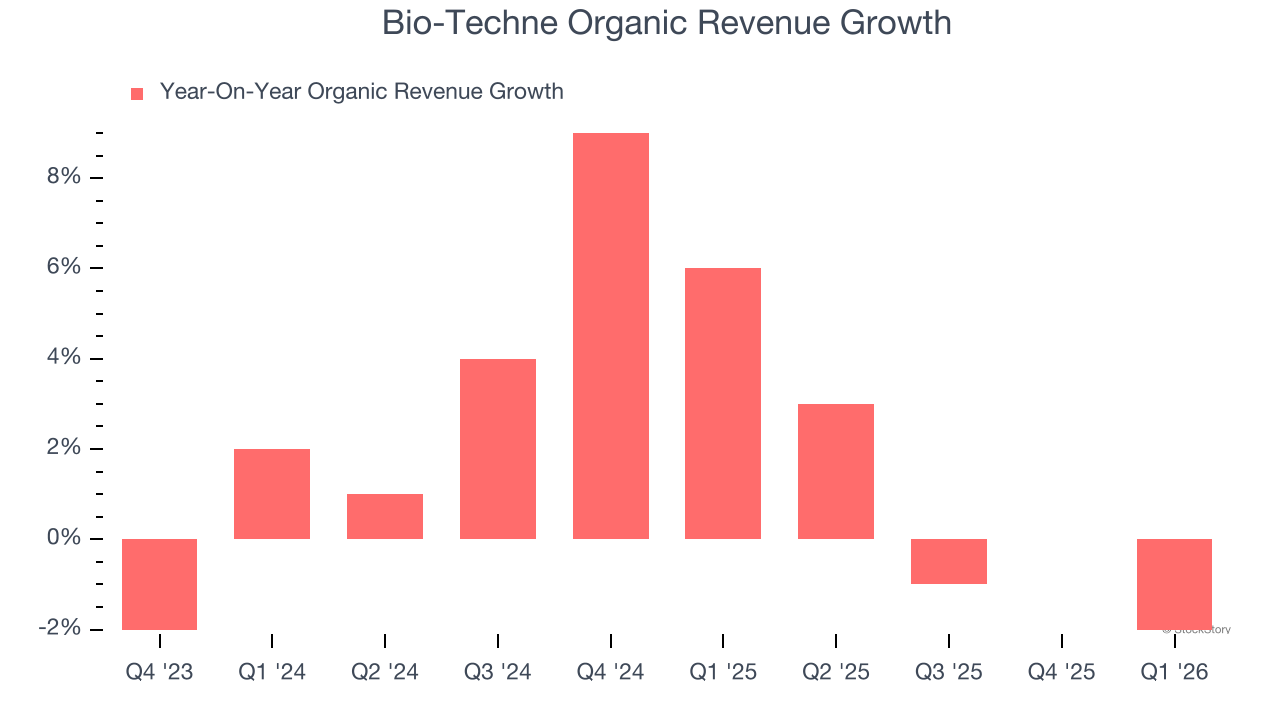

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Bio-Techne’s organic revenue averaged 2.5% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Bio-Techne missed Wall Street’s estimates and reported a rather uninspiring 1.5% year-on-year revenue decline, generating $311.4 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and indicates its newer products and services will spur better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

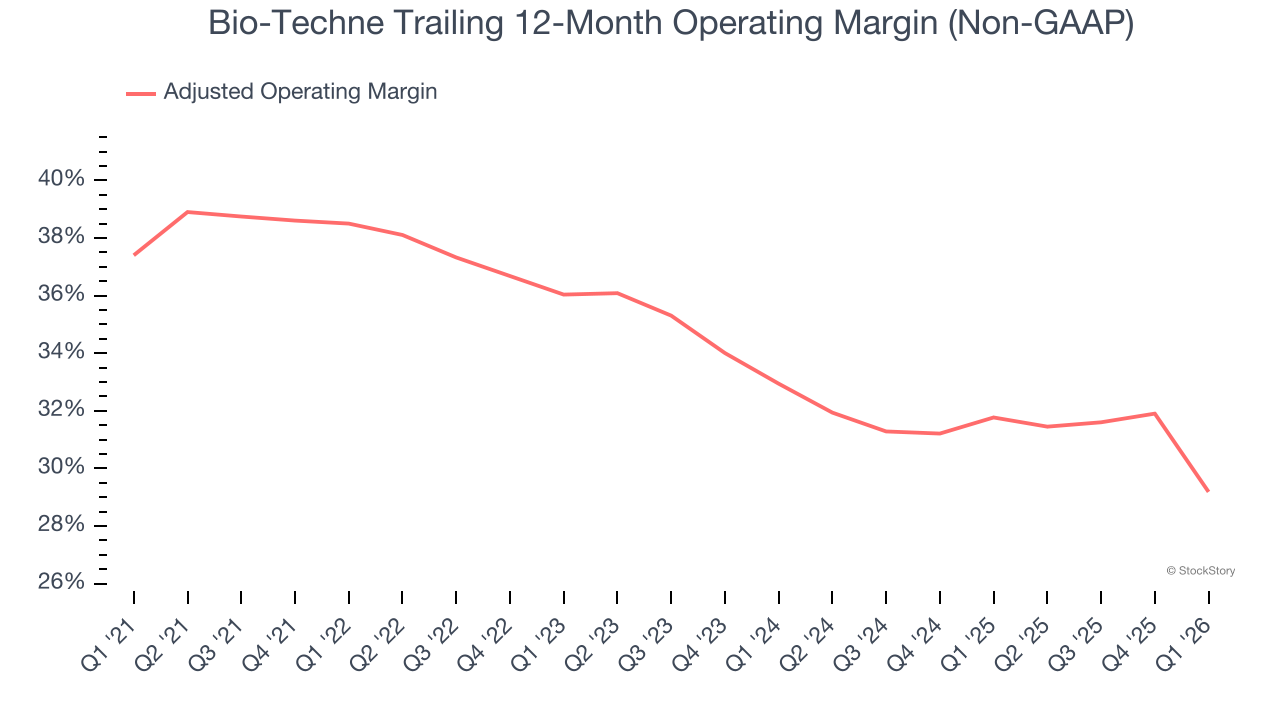

Adjusted Operating Margin

Bio-Techne has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 33.5%.

Analyzing the trend in its profitability, Bio-Techne’s adjusted operating margin decreased by 9.3 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.8 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Bio-Techne generated an adjusted operating margin profit margin of 24.4%, down 10.5 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

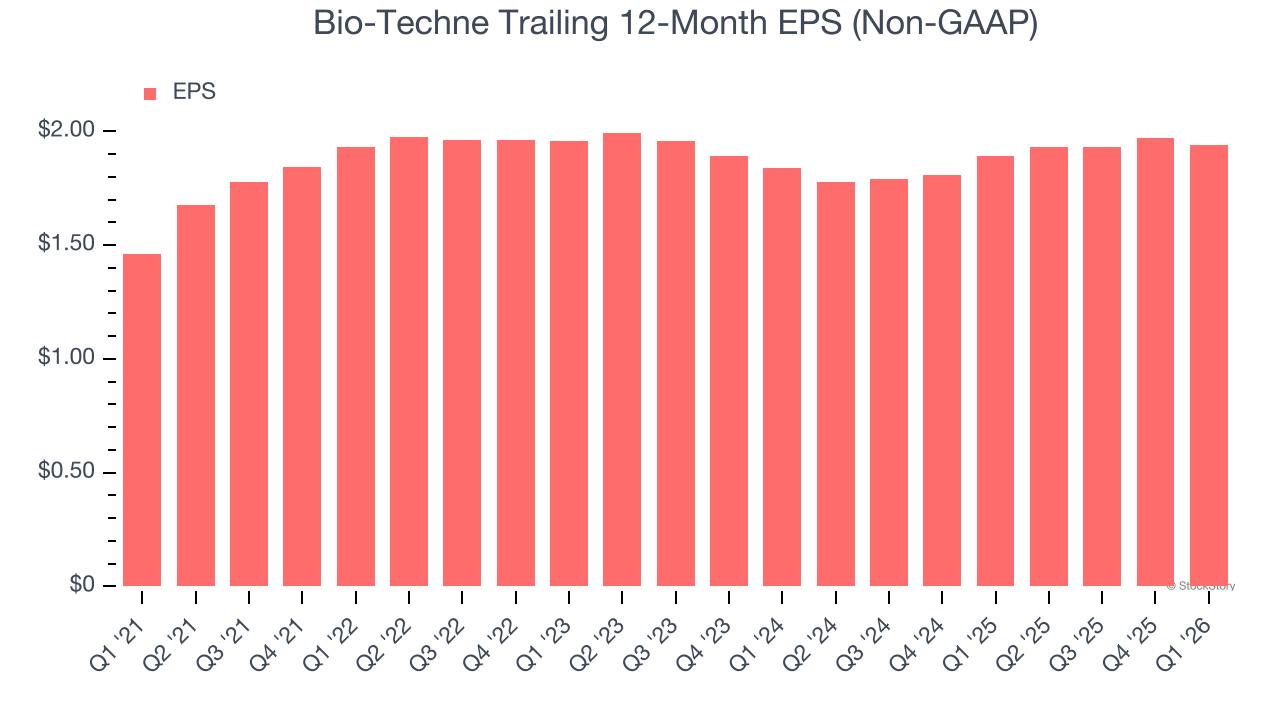

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Bio-Techne’s decent 5.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Bio-Techne reported adjusted EPS of $0.53, down from $0.56 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Bio-Techne’s full-year EPS of $1.94 to grow 8.9%.

Key Takeaways from Bio-Techne’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its organic revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.8% to $55.12 immediately following the results.

Bio-Techne’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).