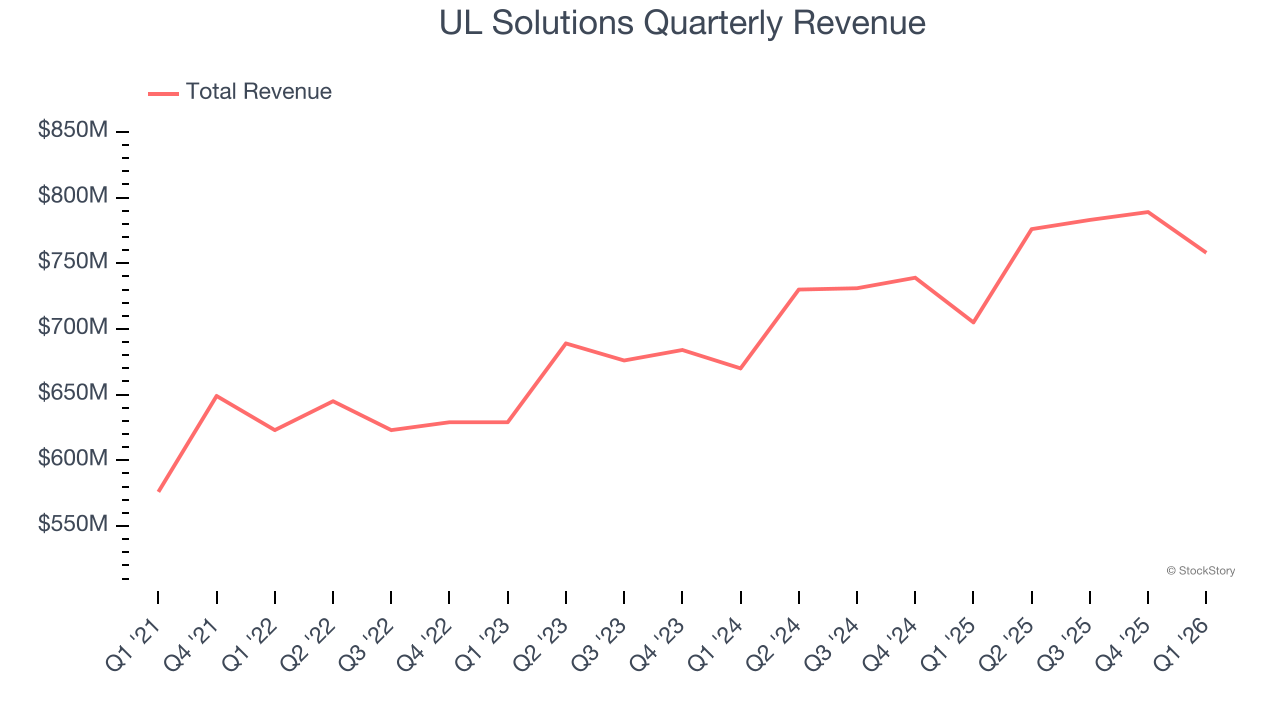

Safety certification company UL Solutions (NYSE:ULS) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 7.5% year on year to $758 million. Its non-GAAP profit of $0.50 per share was 21.4% above analysts’ consensus estimates.

Is now the time to buy UL Solutions? Find out by accessing our full research report, it’s free.

UL Solutions (ULS) Q1 CY2026 Highlights:

- Revenue: $758 million vs analyst estimates of $748.9 million (7.5% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.50 vs analyst estimates of $0.41 (21.4% beat)

- Adjusted EBITDA: $197 million vs analyst estimates of $177.5 million (26% margin, 11% beat)

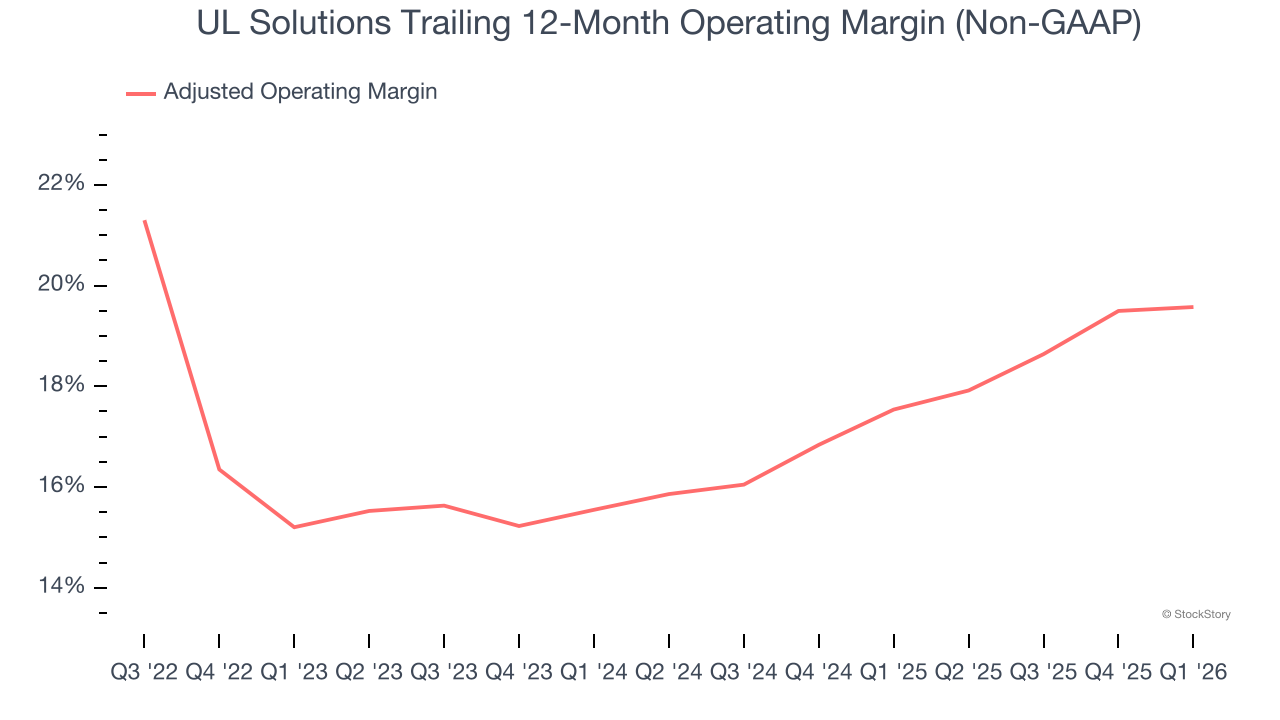

- Operating Margin: 18.2%, up from 15.5% in the same quarter last year

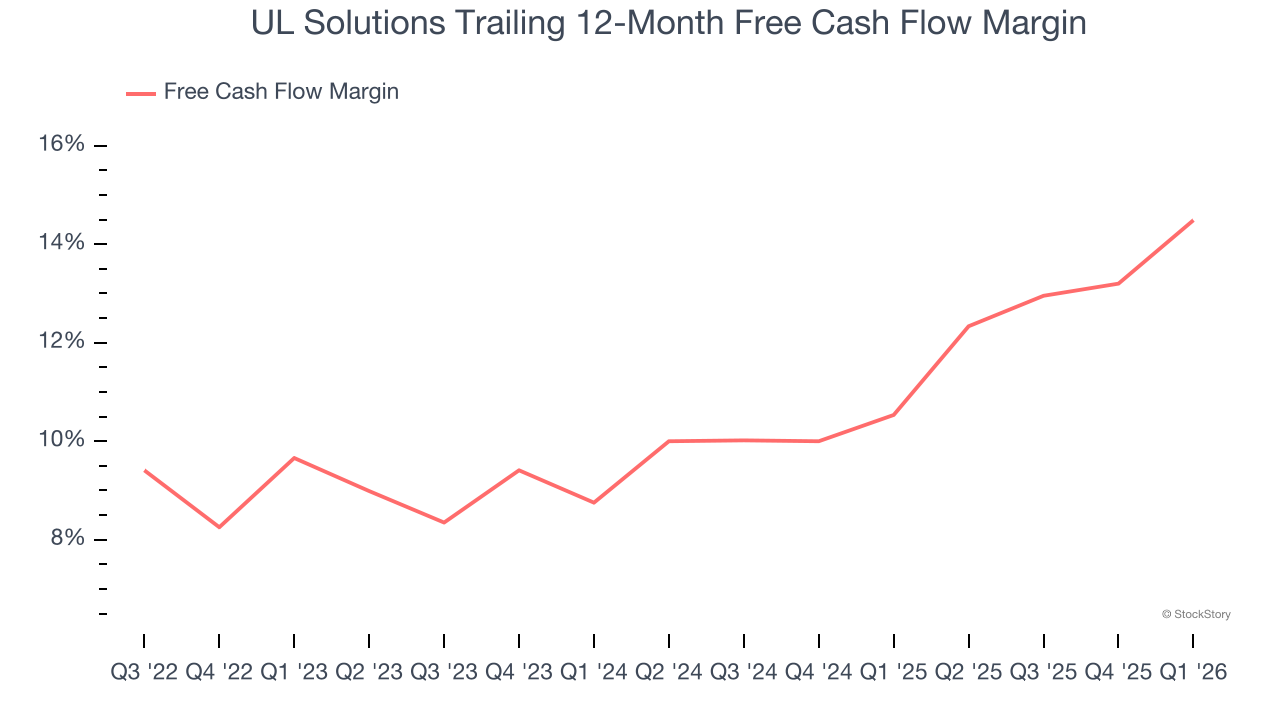

- Free Cash Flow Margin: 19.8%, up from 14.6% in the same quarter last year

- Market Capitalization: $18.13 billion

Company Overview

Founded in 1894 as a response to the growing dangers of electricity in American homes and businesses, UL Solutions (NYSE:ULS) provides testing, inspection, and certification services that help companies ensure their products meet safety, security, and sustainability standards.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $3.11 billion in revenue over the past 12 months, UL Solutions is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

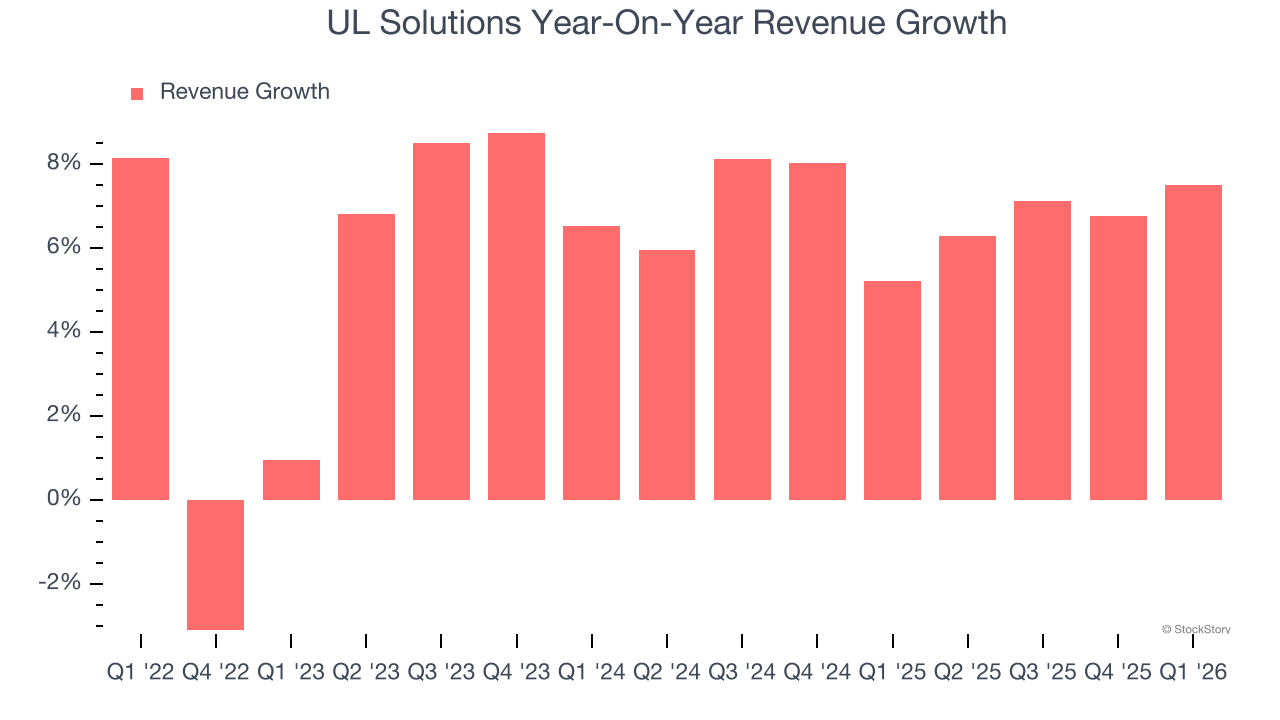

As you can see below, UL Solutions’s sales grew at a decent 5% compounded annual growth rate over the last four years. This shows its offerings generated slightly more demand than the average business services company, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. UL Solutions’s annualized revenue growth of 6.9% over the last two years is above its four-year trend, suggesting some bright spots.

This quarter, UL Solutions reported year-on-year revenue growth of 7.5%, and its $758 million of revenue exceeded Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

UL Solutions has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average adjusted operating margin of 17.9%.

Analyzing the trend in its profitability, UL Solutions’s adjusted operating margin decreased by 7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, UL Solutions generated an adjusted operating margin profit margin of 17%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

UL Solutions has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.9% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that UL Solutions’s margin expanded by 5.3 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

UL Solutions’s free cash flow clocked in at $150 million in Q1, equivalent to a 19.8% margin. This result was good as its margin was 5.2 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from UL Solutions’s Q1 Results

It was good to see UL Solutions beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 2.3% to $92.25 immediately after reporting.

Indeed, UL Solutions had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).