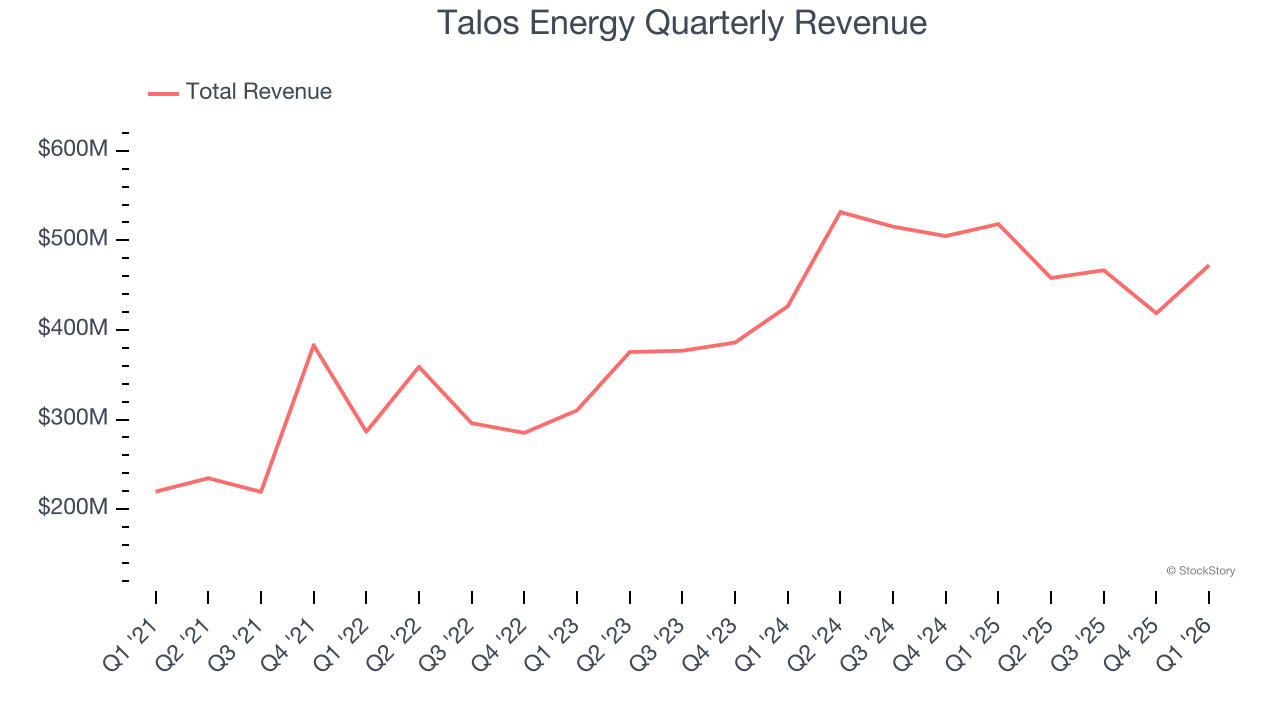

Offshore energy producer Talos Energy (NYSE:TALO) beat Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 8.9% year on year to $472.3 million. Its non-GAAP loss of $0.07 per share was 34.8% above analysts’ consensus estimates.

Is now the time to buy Talos Energy? Find out by accessing our full research report, it’s free.

Talos Energy (TALO) Q1 CY2026 Highlights:

- Revenue: $472.3 million vs analyst estimates of $448.8 million (8.9% year-on-year decline, 5.2% beat)

- Adjusted EPS: -$0.07 vs analyst estimates of -$0.11 (34.8% beat)

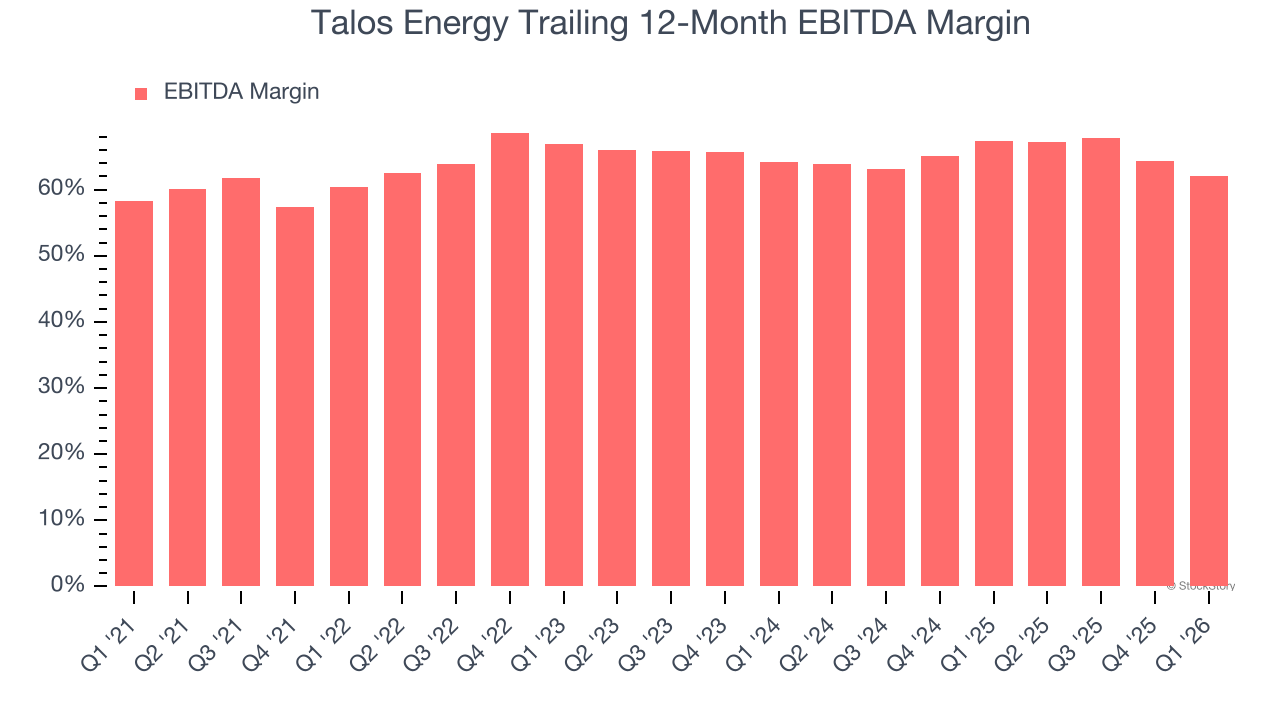

- Adjusted EBITDA: $293.4 million vs analyst estimates of $274.1 million (62.1% margin, 7% beat)

- Operating Margin: -25.3%, down from 8.4% in the same quarter last year

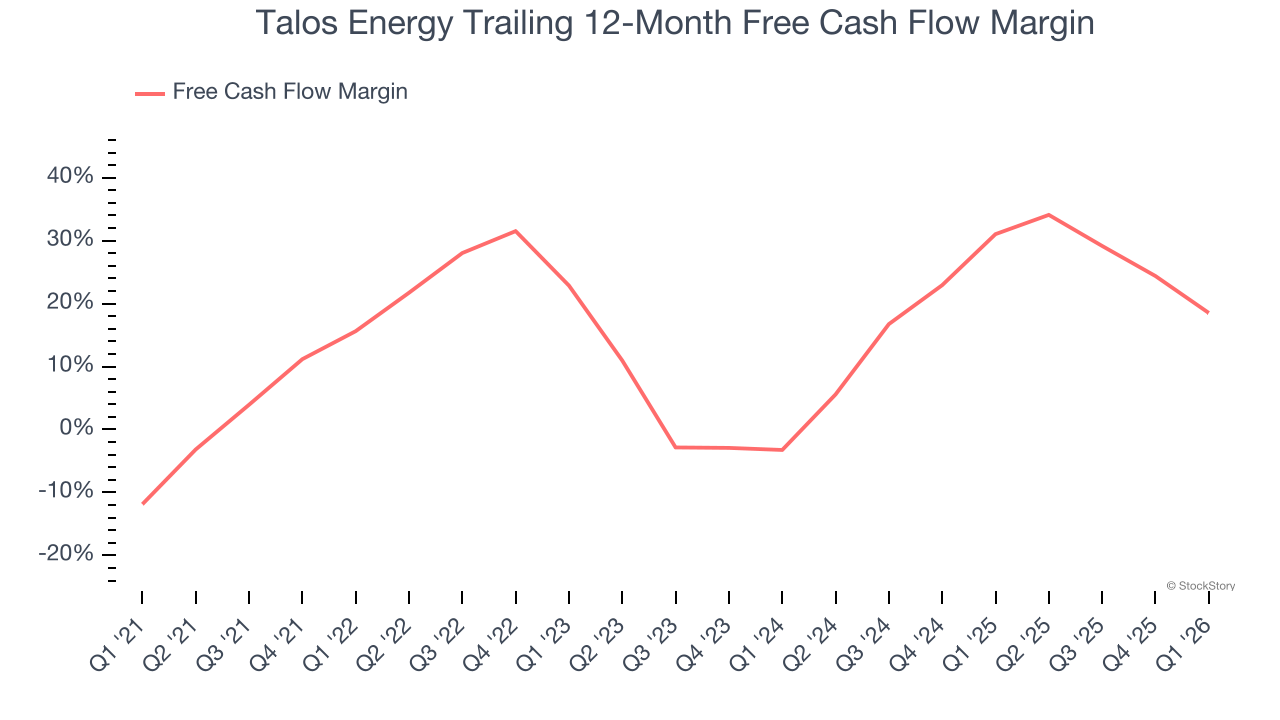

- Free Cash Flow Margin: 4.6%, down from 26.9% in the same quarter last year

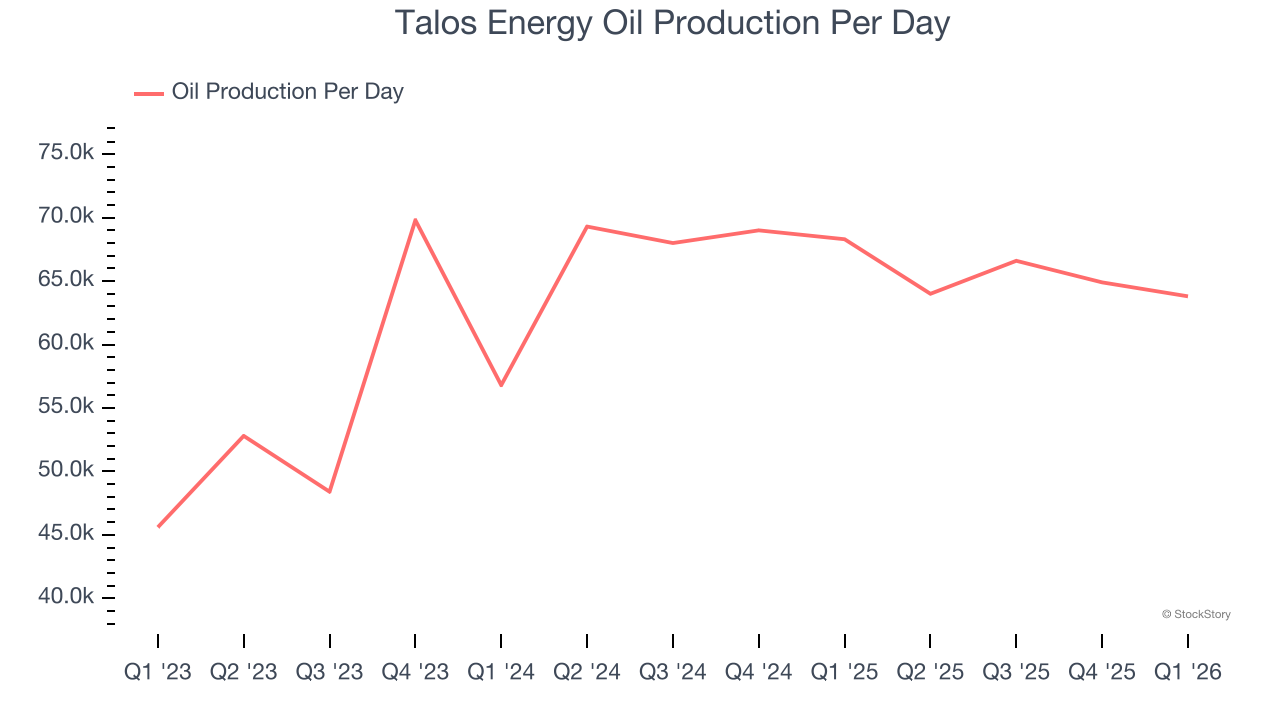

- Oil production per day: down -6.6% year on year

- Market Capitalization: $2.68 billion

"Amid significant macro volatility, Talos remains firmly focused on executing the 2026 plan that we outlined earlier this year, anchored by our disciplined capital allocation framework," said Paul Goodfellow, President and Chief Executive Officer of Talos.

Company Overview

Operating its own deepwater production facilities with names like Tarantula, Pompano, and Brutus, Talos Energy (NYSE:TALO) explores for and produces oil and natural gas from offshore wells in the Gulf of Mexico and offshore Mexico.

Revenue Growth

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Luckily, Talos Energy’s sales grew at an excellent 20.3% compounded annual growth rate over the last five years. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers, a great starting point for our analysis.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Talos Energy’s annualized revenue growth of 17.1% over the last eight years is below its five-year trend, but we still think the results suggest decent demand.

While looking at revenue is important, it can also introduce noise around commodity prices and M&A. Analyzing production, on the other hand, highlights what is happening inside the asset base and whether the economic footprint of a company is expanding. Over the last two years, Talos Energy’s oil production per day averaged 8.6% year-on-year growth while its natural gas production per day averaged 39.3% year-on-year growth.

This quarter, Talos Energy’s revenue fell by 8.9% year on year to $472.3 million but beat Wall Street’s estimates by 5.2%. This quarter, Talos Energy’s Oil production per day fell by 6.6% year on year.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted EBITDA Margin

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Talos Energy has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 64.4%.

Analyzing the trend in its profitability, Talos Energy’s EBITDA margin rose by 1.8 percentage points over the last year, as its sales growth gave it operating leverage.

In Q1, Talos Energy generated an EBITDA margin profit margin of 62.1%, down 7.9 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA beat Wall Street’s estimates by 7%.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Talos Energy has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 17.8% over the last five years.

While the level of free cash flow margins is important, their consistency matters just as much.

Talos Energy’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 7.8 (lower is better), indicating reasonable insulation from commodity swings.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Talos Energy? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Talos Energy’s free cash flow clocked in at $21.58 million in Q1, equivalent to a 4.6% margin. The company’s cash profitability regressed as it was 22.3 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Talos Energy’s Q1 Results

It was good to see Talos Energy beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 1.9% to $15.62 immediately after reporting.

So should you invest in Talos Energy right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).