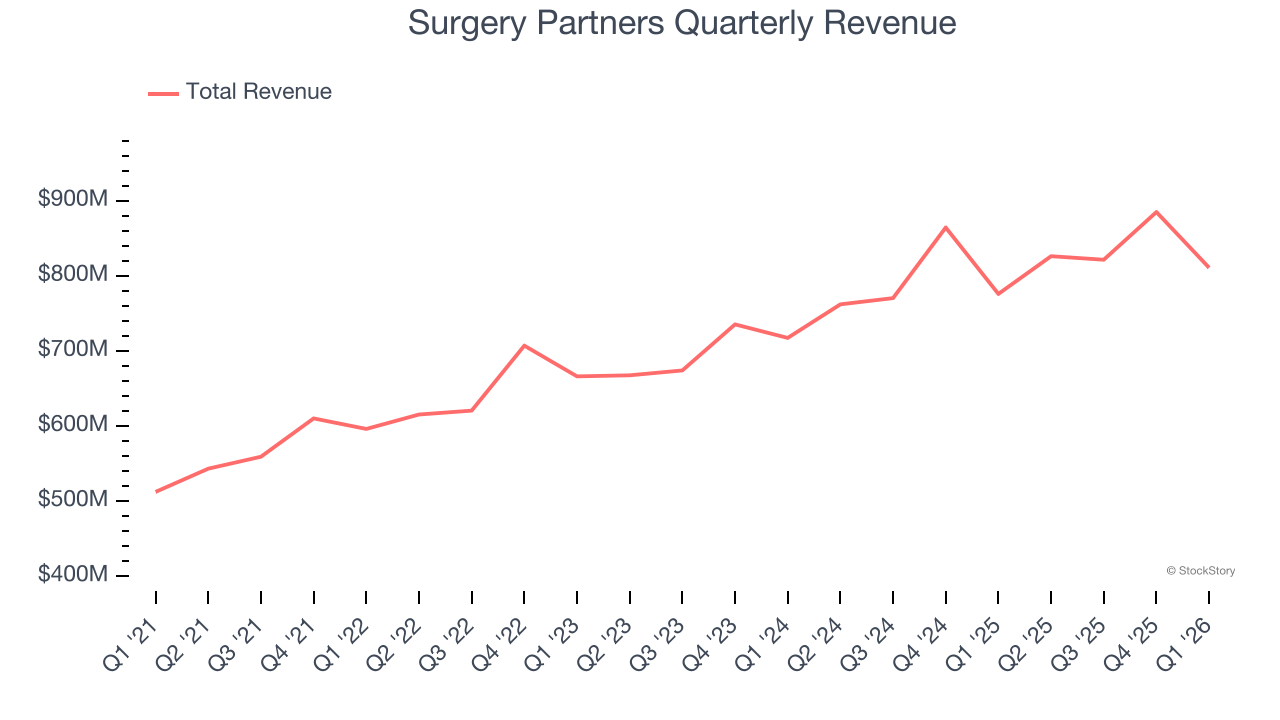

Healthcare company Surgery Partners (NASDAQ:SGRY) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 4.5% year on year to $810.9 million. The company expects the full year’s revenue to be around $3.4 billion, close to analysts’ estimates. Its non-GAAP loss of $0.03 per share was 77.8% above analysts’ consensus estimates.

Is now the time to buy Surgery Partners? Find out by accessing our full research report, it’s free.

Surgery Partners (SGRY) Q1 CY2026 Highlights:

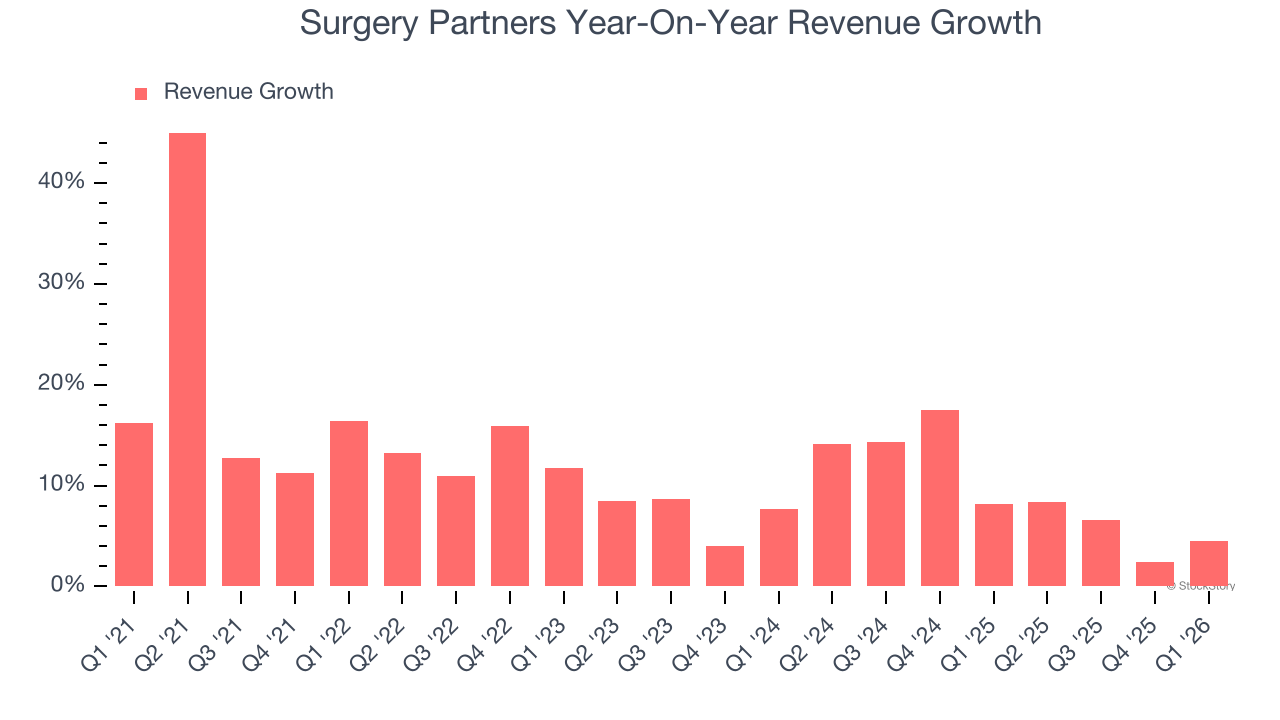

- Revenue: $810.9 million vs analyst estimates of $798.3 million (4.5% year-on-year growth, 1.6% beat)

- Adjusted EPS: -$0.03 vs analyst estimates of -$0.14 (77.8% beat)

- Adjusted EBITDA: $102.3 million vs analyst estimates of $99.76 million (12.6% margin, 2.5% beat)

- The company reconfirmed its revenue guidance for the full year of $3.4 billion at the midpoint

- EBITDA guidance for the full year is $530 million at the midpoint, in line with analyst expectations

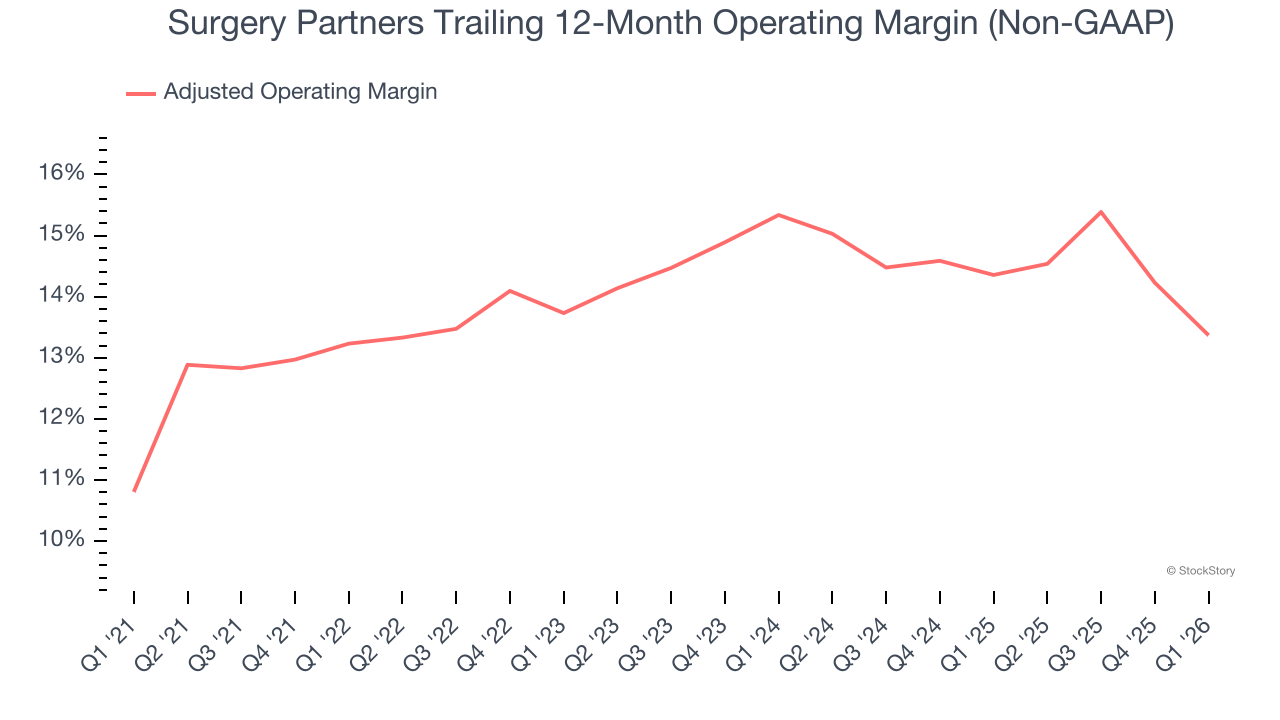

- Operating Margin: 8.1%, in line with the same quarter last year

- Free Cash Flow was -$4.3 million compared to -$16.7 million in the same quarter last year

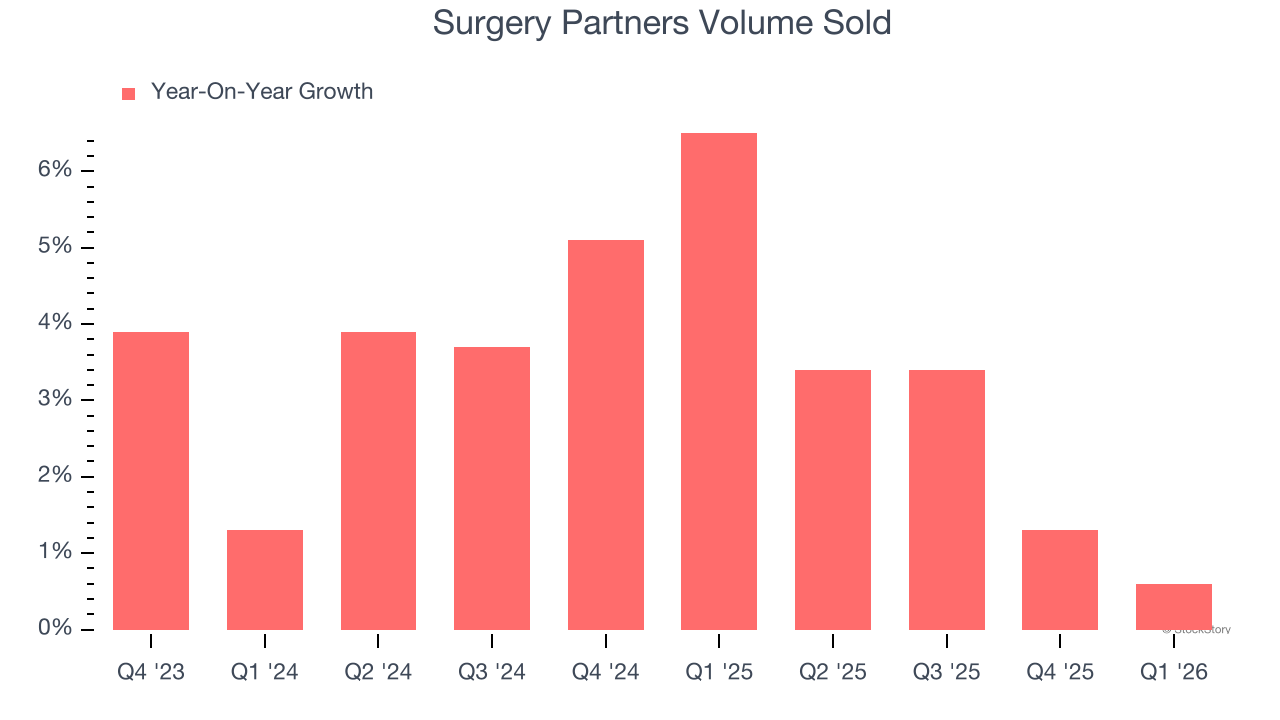

- Sales Volumes were flat year on year (6.5% in the same quarter last year)

- Market Capitalization: $1.84 billion

Eric Evans, Chief Executive Officer, stated, “We are encouraged by our solid start to 2026, with same store revenue growth of 4.4% in line with our Q1 and long-term growth expectations. As we continue to navigate near-term market dynamics, our cost management discipline and continued execution on physician recruitment position us well to meet or exceed our 2026 plan. Our portfolio optimization efforts also remain critical to our long-term strategy as we take steps to better align with our core short-stay surgical operating model. Looking ahead, we are confident in our ability to return to our growth algorithm through capitalizing on market opportunities, driving operational excellence, and thoughtful capital deployment.”

Company Overview

With more than 180 locations across 33 states serving as alternatives to traditional hospital settings, Surgery Partners (NASDAQ:SGRY) operates a national network of outpatient surgical facilities including ambulatory surgery centers and short-stay surgical hospitals.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Surgery Partners grew its sales at a decent 11.6% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Surgery Partners’s annualized revenue growth of 9.4% over the last two years is below its five-year trend, but we still think the results were respectable.

We can better understand the company’s revenue dynamics by analyzing its number of units sold. Over the last two years, Surgery Partners’s units sold averaged 3.5% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Surgery Partners reported modest year-on-year revenue growth of 4.5% but beat Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

Surgery Partners’s adjusted operating margin has generally stayed the same over the last 12 months, averaging 14% over the last five years. This profitability was higher than the broader healthcare sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, Surgery Partners’s adjusted operating margin of 13.4% for the trailing 12 months may be around the same as five years ago, but it has decreased by 2 percentage points over the last two years.

This quarter, Surgery Partners generated an adjusted operating margin profit margin of 8.1%, down 3.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

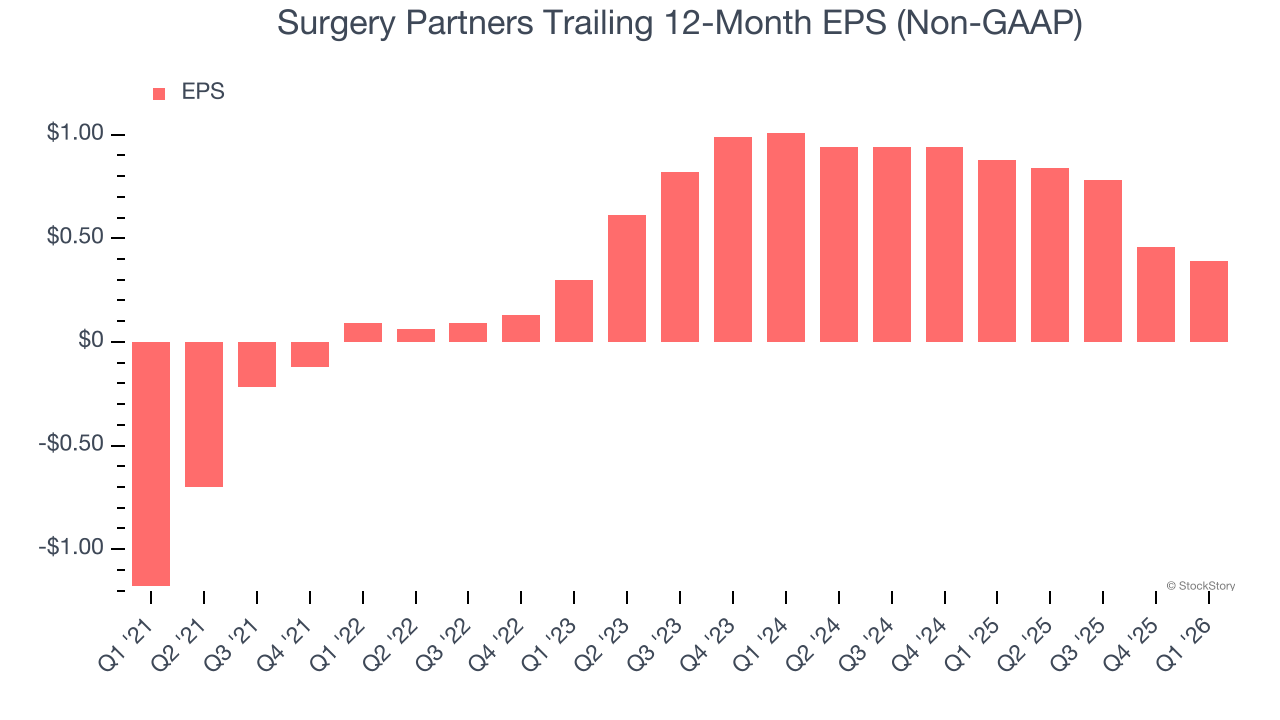

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Surgery Partners’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Surgery Partners reported adjusted EPS of negative $0.03, down from $0.04 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Surgery Partners’s full-year EPS of $0.39 to shrink by 39%.

Key Takeaways from Surgery Partners’s Q1 Results

It was good to see Surgery Partners beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance was in line. Overall, this print had some key positives. The stock traded up 1.9% to $14.47 immediately after reporting.

Surgery Partners had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).