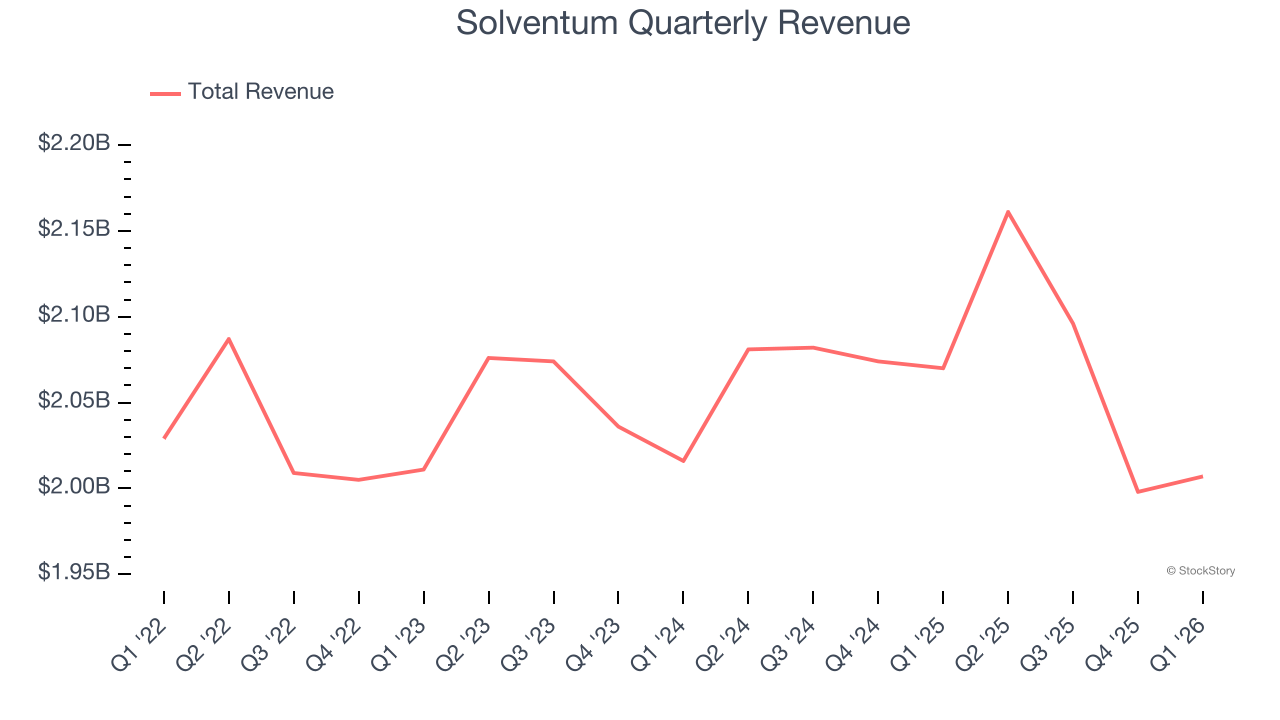

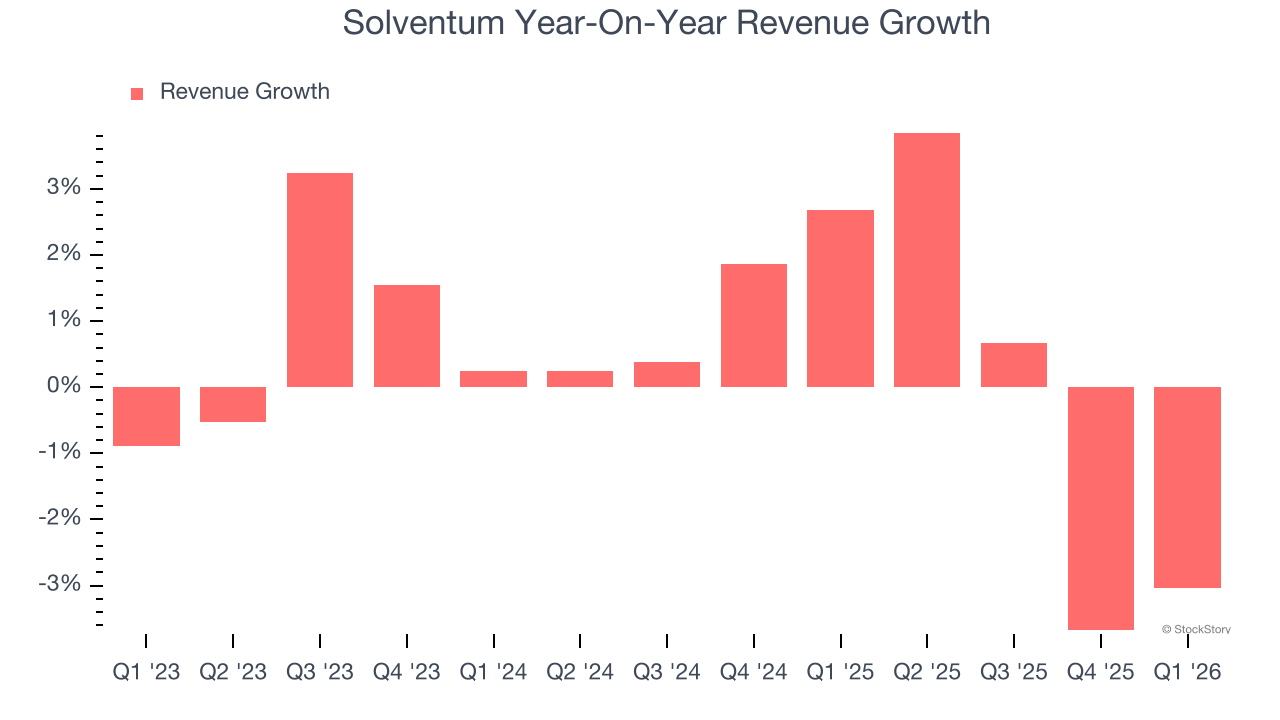

Healthcare solutions provider Solventum (NYSE:SOLV) reported Q1 CY2026 results exceeding the market’s revenue expectations, but sales fell by 3% year on year to $2.01 billion. Its non-GAAP profit of $1.48 per share was 9.3% above analysts’ consensus estimates.

Is now the time to buy Solventum? Find out by accessing our full research report, it’s free.

Solventum (SOLV) Q1 CY2026 Highlights:

- Revenue: $2.01 billion vs analyst estimates of $1.97 billion (3% year-on-year decline, 1.9% beat)

- Adjusted EPS: $1.48 vs analyst estimates of $1.35 (9.3% beat)

- Adjusted EBITDA: $267 million vs analyst estimates of $426.1 million (13.3% margin, 37.3% miss)

- Management reiterated its full-year Adjusted EPS guidance of $6.50 at the midpoint

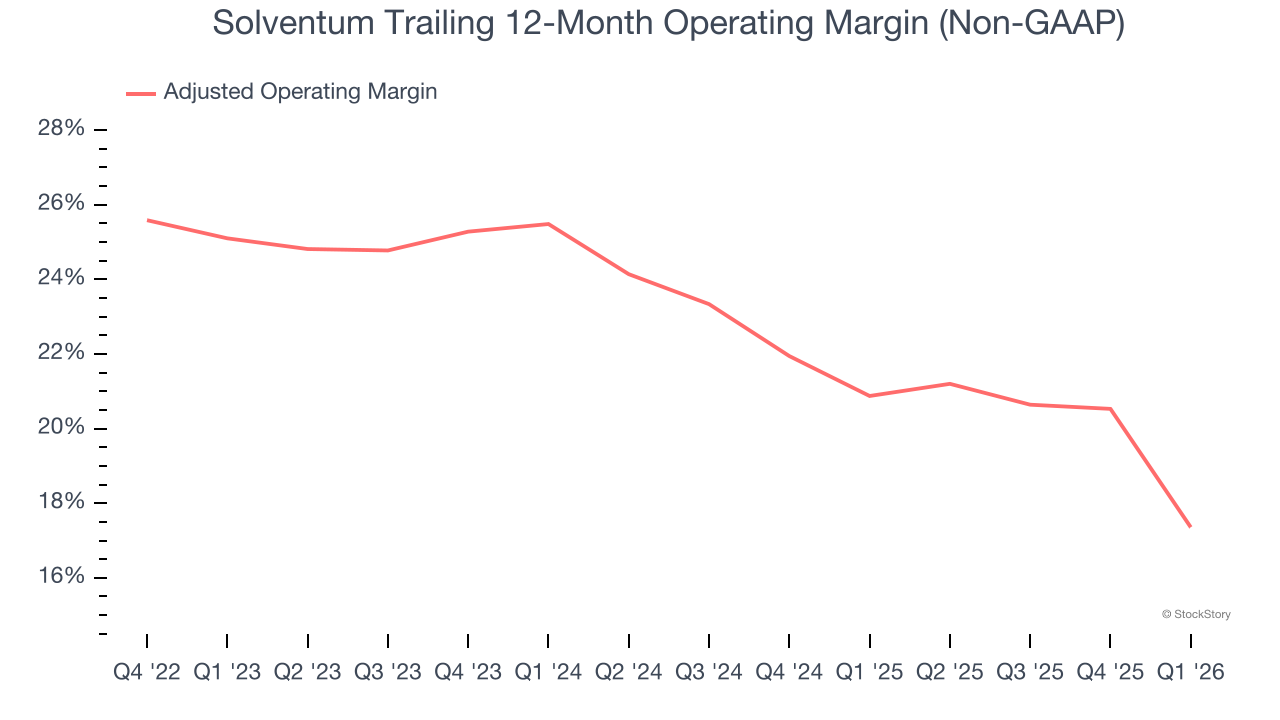

- Operating Margin: 4%, down from 7.3% in the same quarter last year

- Free Cash Flow was -$273 million compared to -$80 million in the same quarter last year

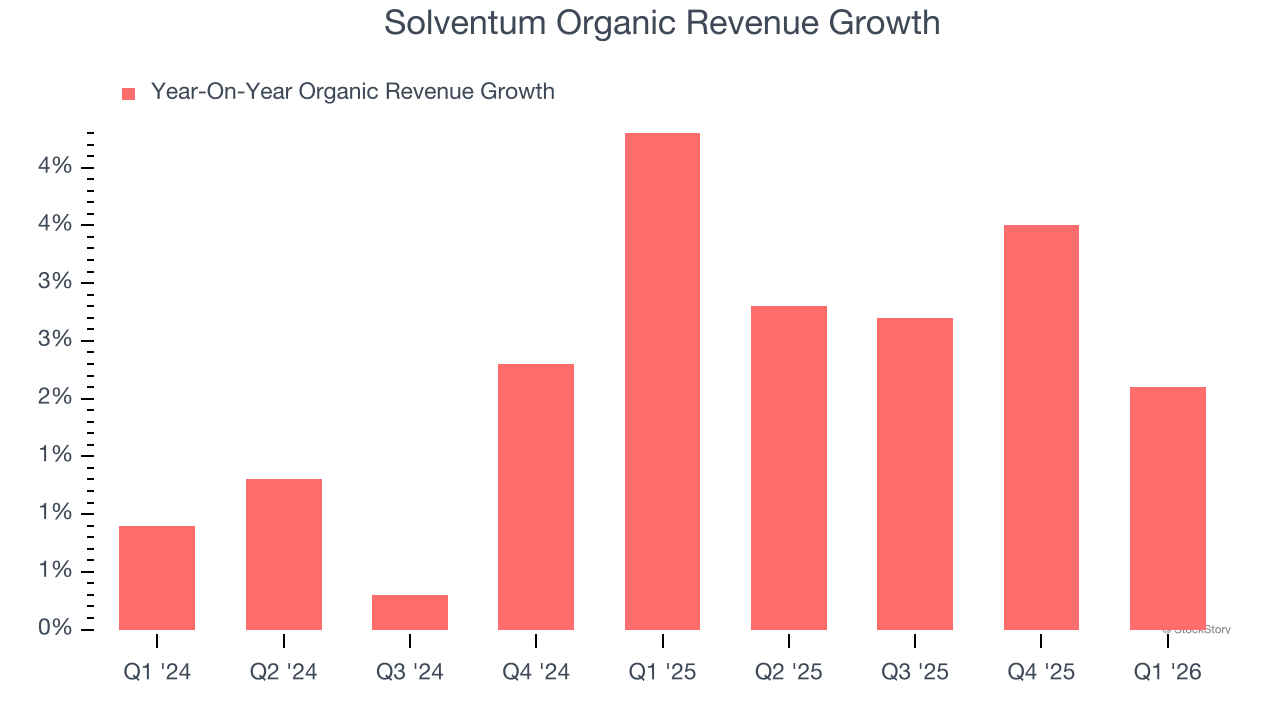

- Organic Revenue rose 2.1% year on year (miss)

- Market Capitalization: $11.69 billion

"Solventum delivered first quarter results ahead of expectations, reflecting strong execution and underlying commercial momentum," said Bryan Hanson, chief executive officer of Solventum.

Company Overview

Founded in 1985, Solventum (NYSE:SOLV) develops, manufactures, and commercializes a portfolio of healthcare products and services addressing critical customer and therapeutic patient needs.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Solventum’s sales grew at a tepid 1.3% compounded annual growth rate over the last three years. This was below our standards and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. Solventum’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

Solventum also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Solventum’s organic revenue averaged 2.4% year-on-year growth. Because this number is better than its two-year revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

This quarter, Solventum’s revenue fell by 3% year on year to $2.01 billion but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Solventum has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 22.4%.

Analyzing the trend in its profitability, Solventum’s adjusted operating margin decreased by 7.7 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 8.1 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Solventum generated an adjusted operating margin profit margin of 6.6%, down 13.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

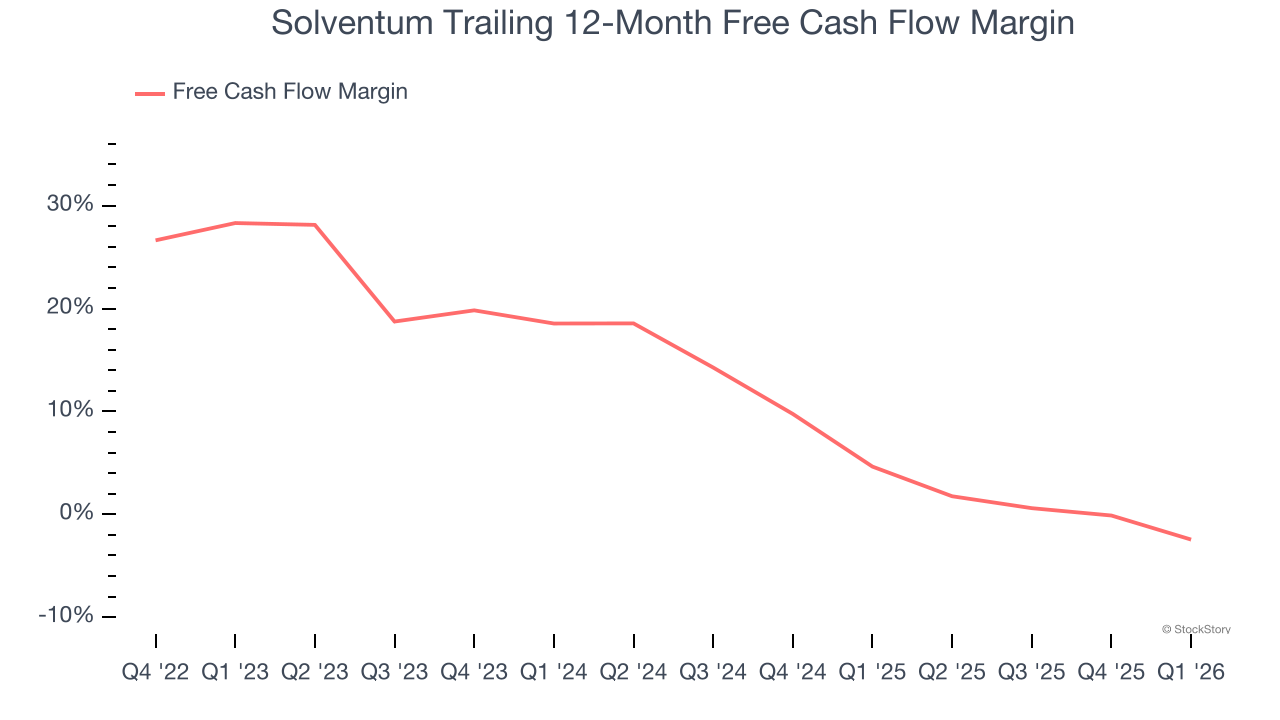

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Solventum has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 12.4% over the last five years, better than the broader healthcare sector.

Taking a step back, we can see that Solventum’s margin dropped by 30.8 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Solventum burned through $273 million of cash in Q1, equivalent to a negative 13.6% margin. The company’s cash burn increased from $80 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

Key Takeaways from Solventum’s Q1 Results

It was encouraging to see Solventum beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $69.50 immediately following the results.

Solventum had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).