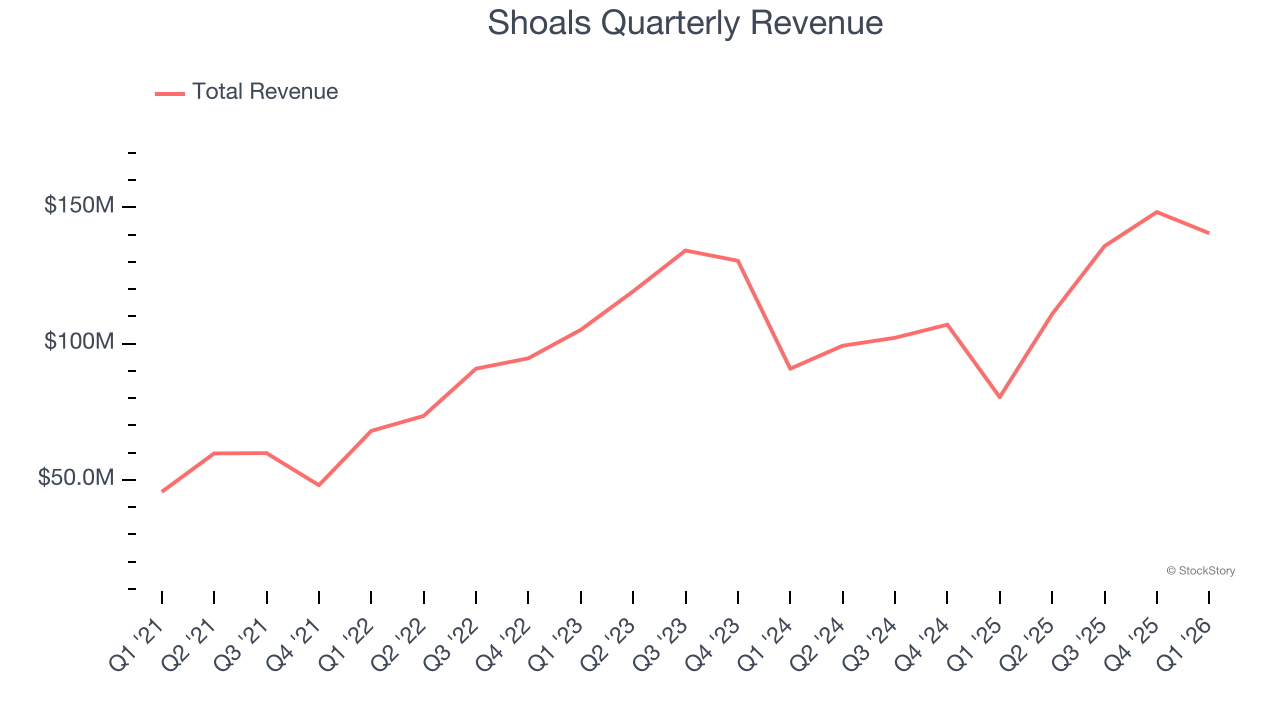

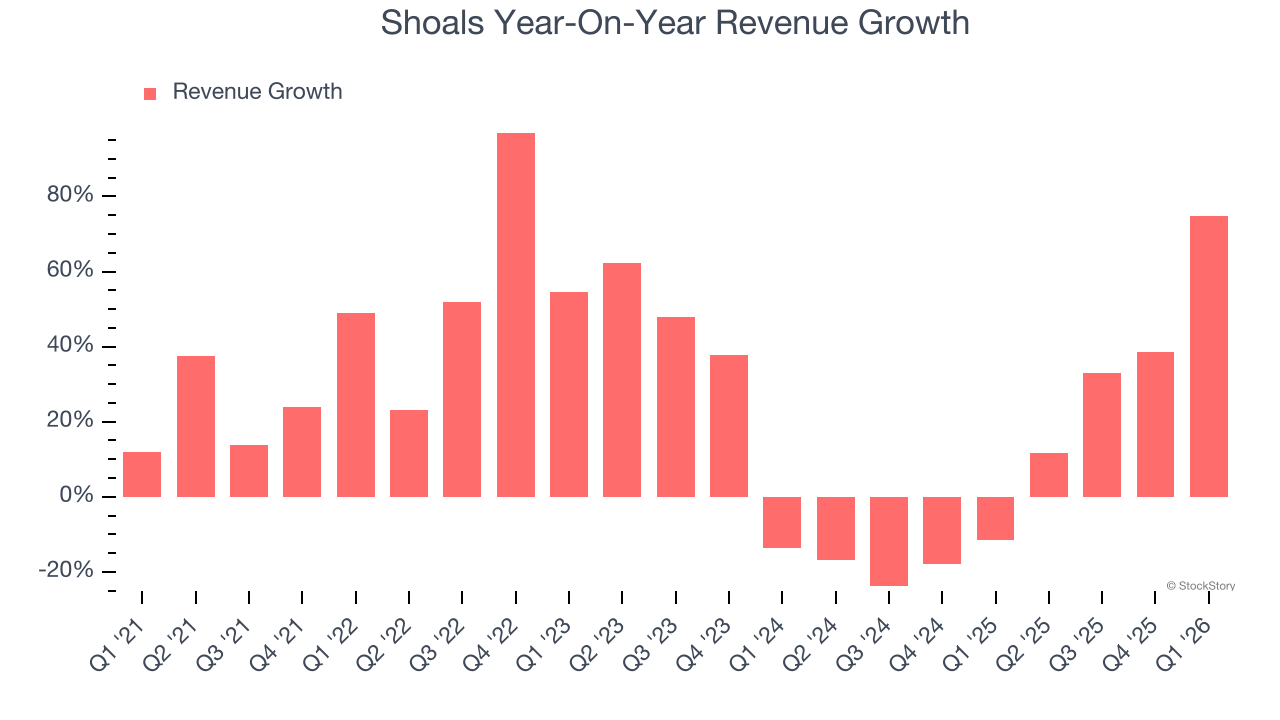

Solar energy systems company Shoals (NASDAQ:SHLS) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 74.9% year on year to $140.6 million. On top of that, next quarter’s revenue guidance ($160 million at the midpoint) was surprisingly good and 15.8% above what analysts were expecting. Its non-GAAP profit of $0.07 per share was in line with analysts’ consensus estimates.

Is now the time to buy Shoals? Find out by accessing our full research report, it’s free.

Shoals (SHLS) Q1 CY2026 Highlights:

- Revenue: $140.6 million vs analyst estimates of $129.4 million (74.9% year-on-year growth, 8.7% beat)

- Adjusted EPS: $0.07 vs analyst estimates of $0.06 (in line)

- Adjusted EBITDA: $21.11 million vs analyst estimates of $19.82 million (15% margin, 6.5% beat)

- The company lifted its revenue guidance for the full year to $620 million at the midpoint from $580 million, a 6.9% increase

- EBITDA guidance for the full year is $125 million at the midpoint, above analyst estimates of $117.2 million

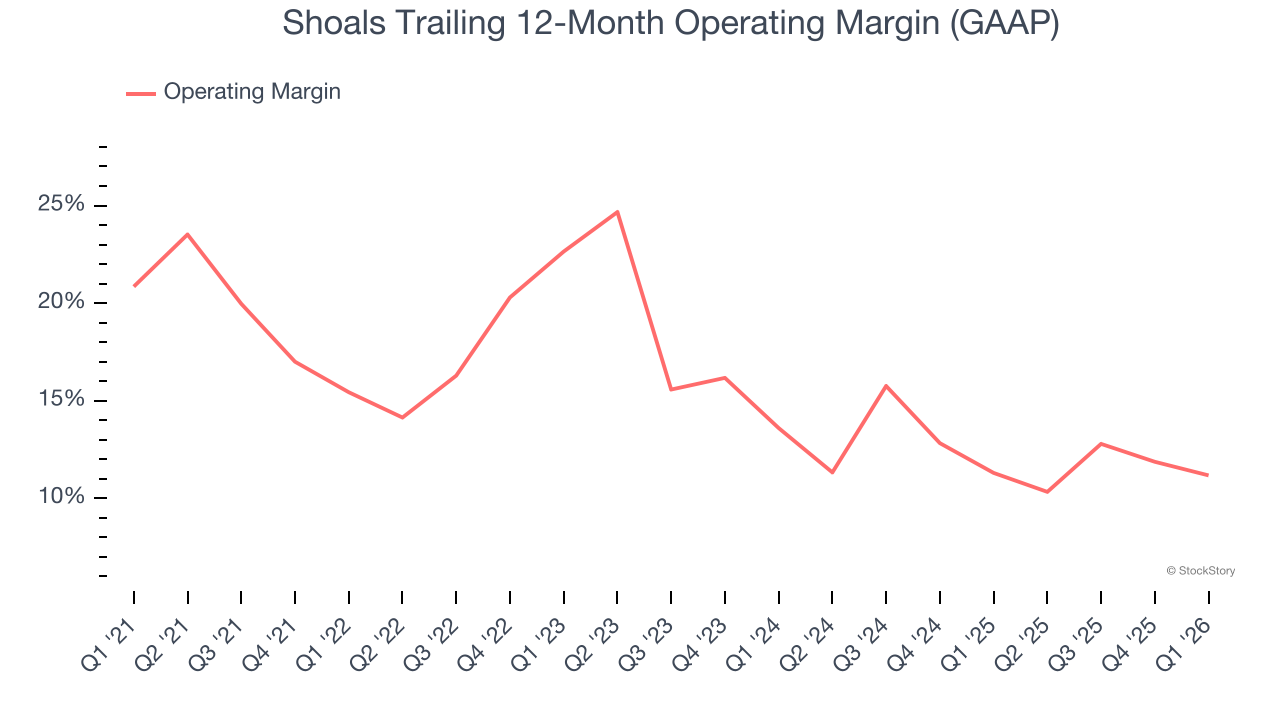

- Operating Margin: 5.5%, in line with the same quarter last year

- Free Cash Flow was -$49.1 million, down from $12.35 million in the same quarter last year

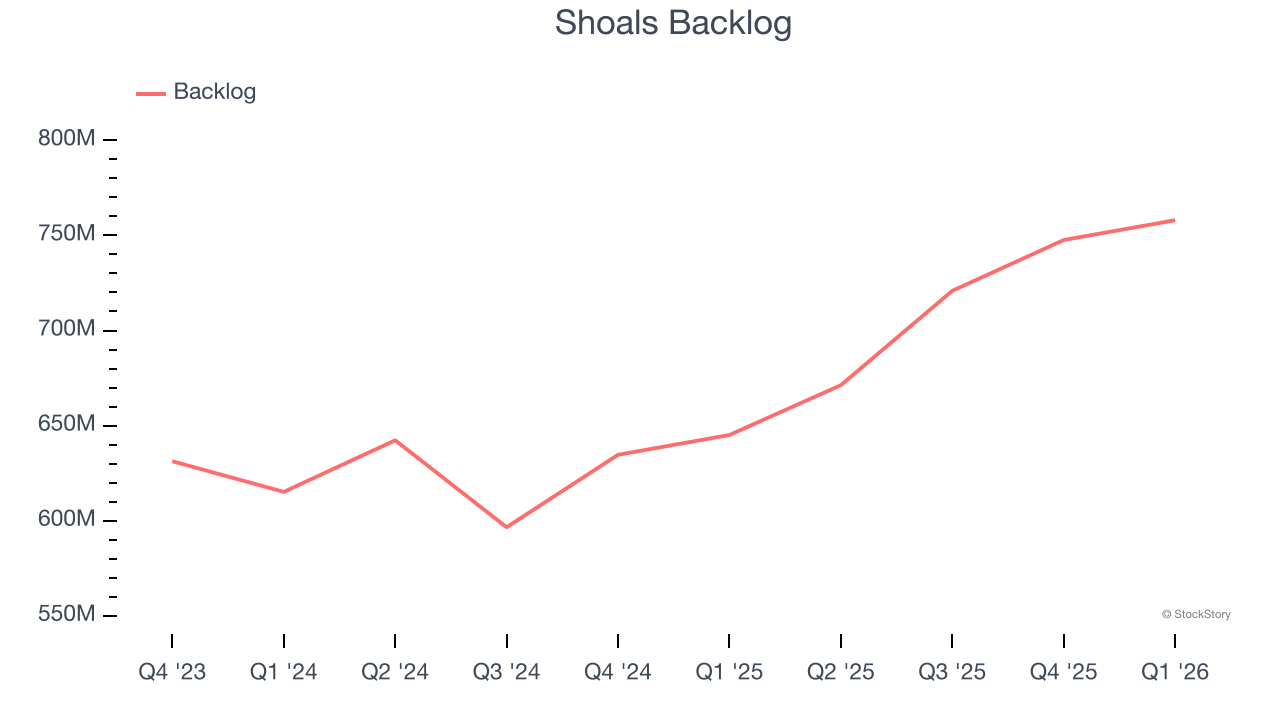

- Backlog: $758 million at quarter end, up 17.5% year on year

- Market Capitalization: $1.39 billion

“We began the year on very solid footing, with revenue above our expected range and growing at approximately 75% from the prior-year period. The underlying demand environment remains extremely strong as evidenced by our record backlog and awarded orders of $758 million. We are executing our strategic plan of accelerating growth within our core domestic utility scale solar market and expanding our offering into attractive high growth markets,” said Brandon Moss, CEO of Shoals.

Company Overview

Started in Huntsville, Alabama, Shoals (NASDAQ:SHLS) designs and manufactures products that make solar energy systems work more efficiently.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Shoals’s sales grew at an incredible 24.3% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Shoals’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 6.2% over the last two years was well below its five-year trend.

Shoals also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Shoals’s backlog reached $758 million in the latest quarter and averaged 11% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Shoals’s products and services but raises concerns about capacity constraints.

This quarter, Shoals reported magnificent year-on-year revenue growth of 74.9%, and its $140.6 million of revenue beat Wall Street’s estimates by 8.7%. Company management is currently guiding for a 44.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.2% over the next 12 months, an improvement versus the last two years. This projection is admirable and indicates its newer products and services will catalyze better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Shoals has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.4%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Shoals’s operating margin decreased by 4.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Shoals generated an operating margin profit margin of 5.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

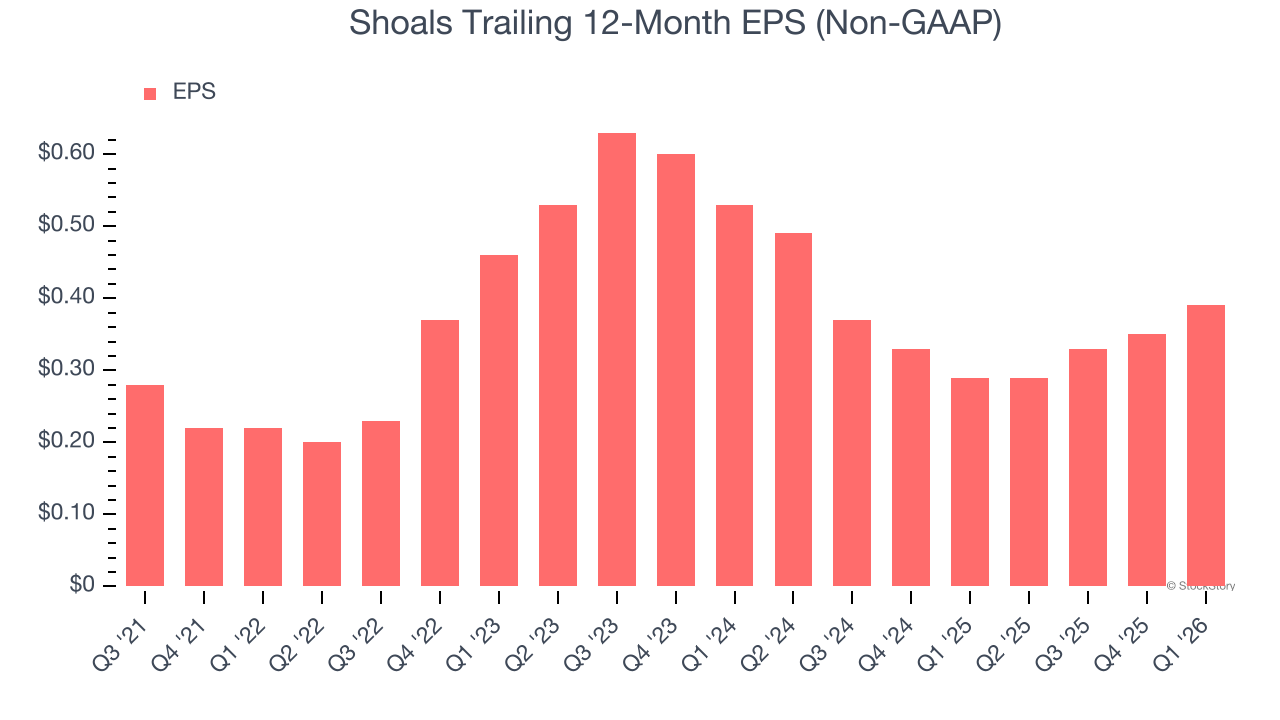

Shoals’s EPS grew at an unimpressive 7.3% compounded annual growth rate over the last five years, lower than its 24.3% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

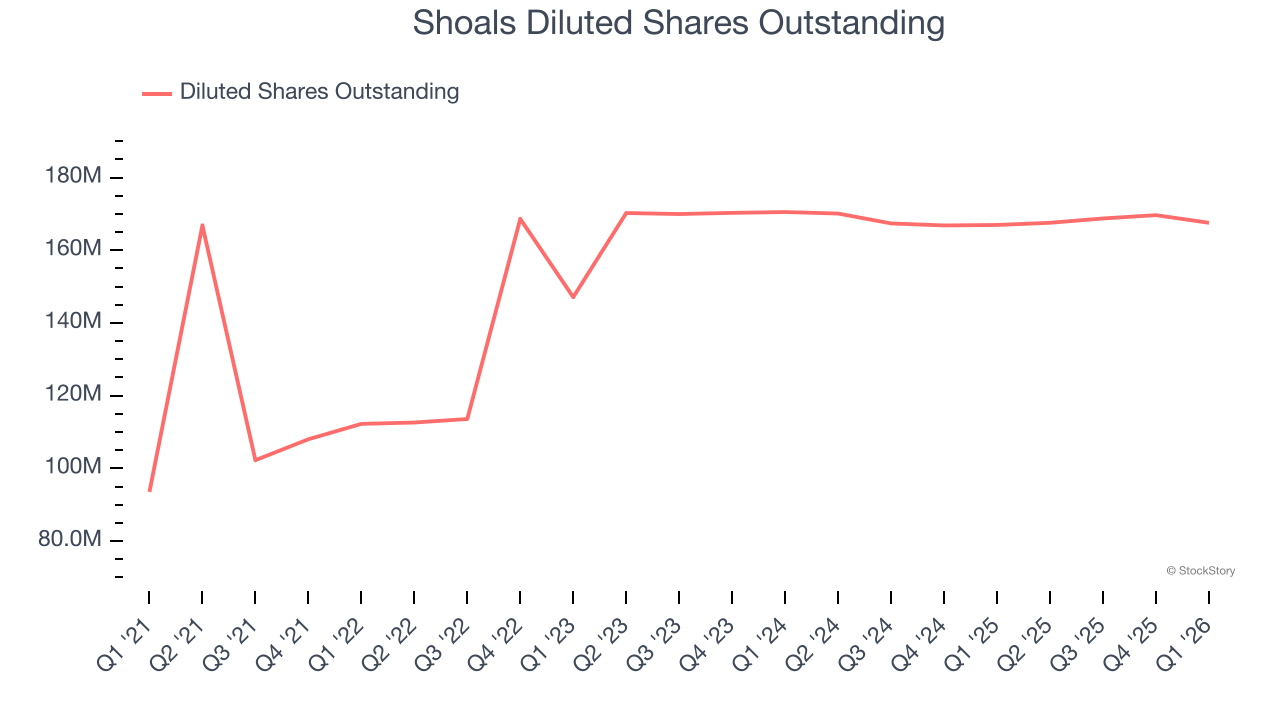

Diving into the nuances of Shoals’s earnings can give us a better understanding of its performance. As we mentioned earlier, Shoals’s operating margin was flat this quarter but declined by 4.3 percentage points over the last five years. Its share count also grew by 79.1%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Shoals, its two-year annual EPS declines of 14.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, Shoals reported adjusted EPS of $0.07, up from $0.03 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Shoals’s full-year EPS of $0.39 to grow 15.4%.

Key Takeaways from Shoals’s Q1 Results

We were impressed by Shoals’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its adjusted operating income missed. Zooming out, we think this quarter featured some important positives. The stock traded up 16.1% to $9.61 immediately after reporting.

Shoals had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).