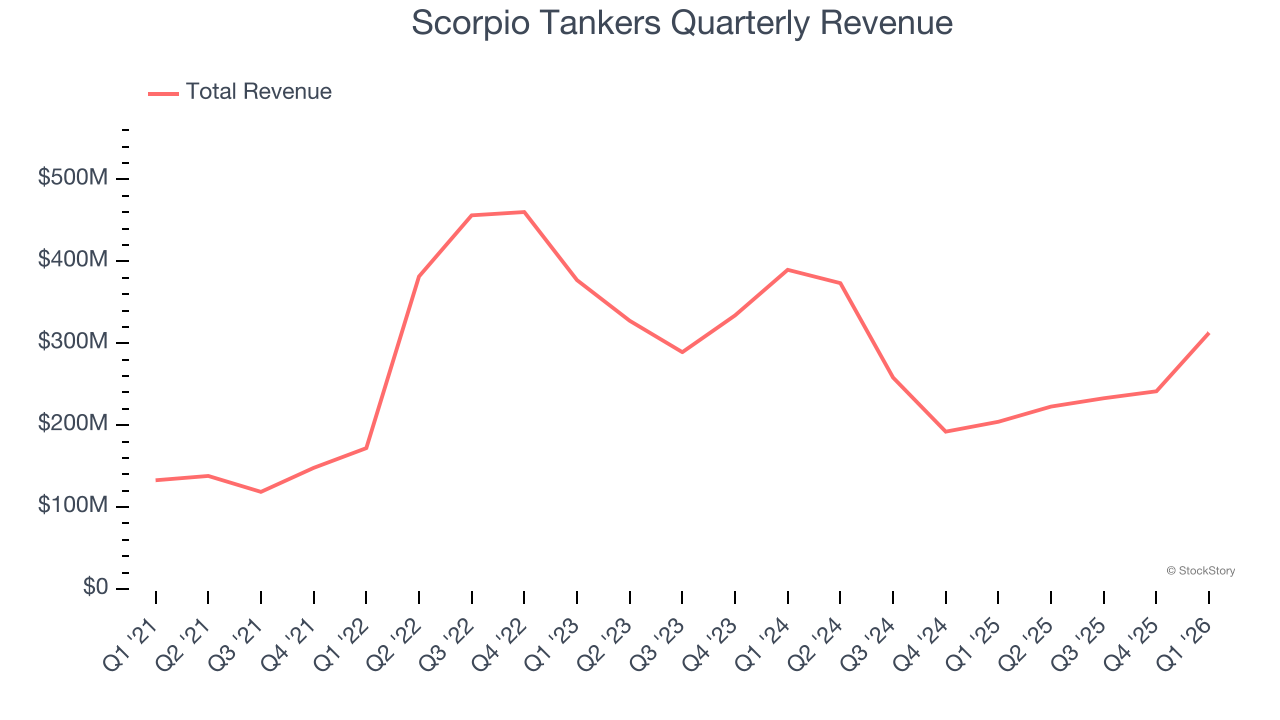

Tanking company Scorpio Tankers (NYSE:STNG) announced better-than-expected revenue in Q1 CY2026, with sales up 53.2% year on year to $312.9 million. Its GAAP profit of $4.32 per share was 58.7% above analysts’ consensus estimates.

Is now the time to buy Scorpio Tankers? Find out by accessing our full research report, it’s free.

Scorpio Tankers (STNG) Q1 CY2026 Highlights:

- Revenue: $312.9 million vs analyst estimates of $285 million (53.2% year-on-year growth, 9.8% beat)

- EPS (GAAP): $4.32 vs analyst estimates of $2.72 (58.7% beat)

- Adjusted EBITDA: $214.1 million vs analyst estimates of $179.1 million (68.4% margin, 19.6% beat)

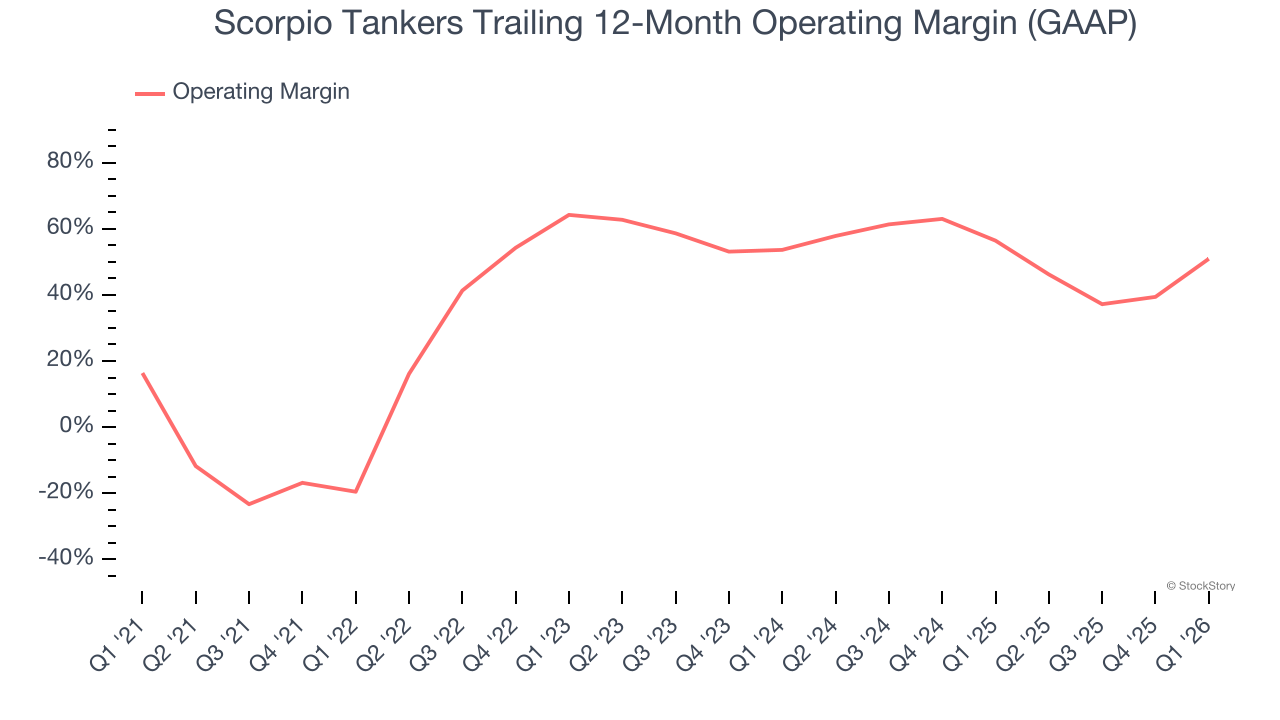

- Operating Margin: 70.2%, up from 29.6% in the same quarter last year

- Free Cash Flow Margin: 49.6%, up from 19.2% in the same quarter last year

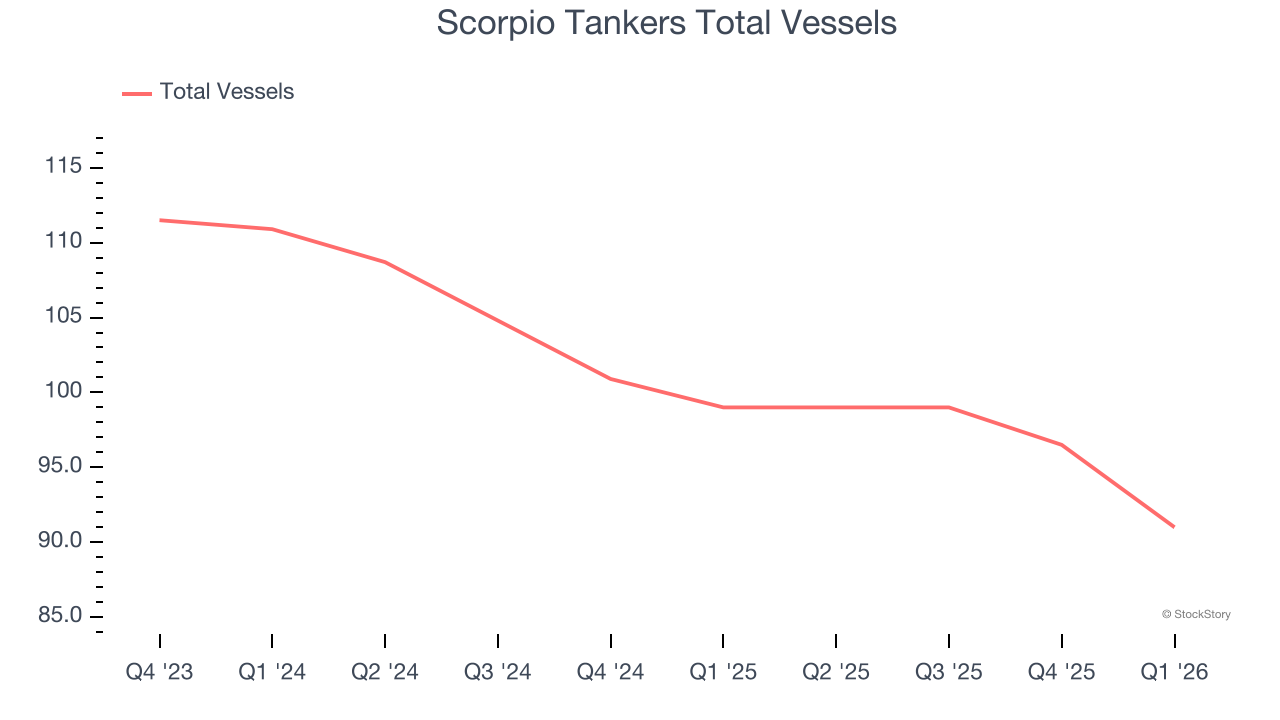

- total vessels: down 8 year on year

- Market Capitalization: $3.93 billion

Company Overview

Operating one of the youngest fleets in the industry, Scorpio Tankers (NYSE: STNG) is an international provider of marine transportation services, specializing in the shipment of refined petroleum.

Revenue Growth

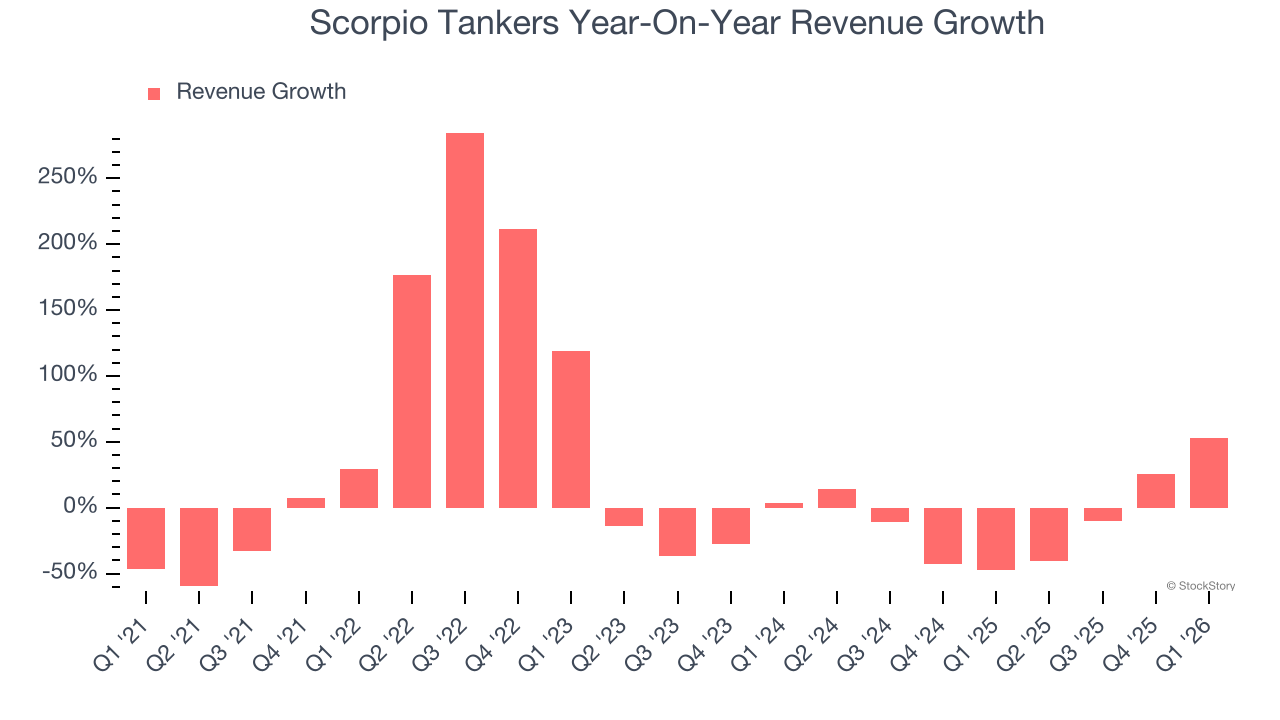

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Scorpio Tankers’s 5% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Scorpio Tankers’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 13.2% annually.

We can dig further into the company’s revenue dynamics by analyzing its number of total vessels, which reached 91 in the latest quarter. Over the last two years, Scorpio Tankers’s total vessels averaged 7.9% year-on-year declines. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Scorpio Tankers reported magnificent year-on-year revenue growth of 53.2%, and its $312.9 million of revenue beat Wall Street’s estimates by 9.8%.

Looking ahead, sell-side analysts expect revenue to decline by 1.2% over the next 12 months. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Scorpio Tankers has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 49.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Scorpio Tankers’s operating margin rose by 70.5 percentage points over the last five years, as its sales growth gave it operating leverage. Its expansion was impressive, especially when considering most Marine Transportation peers saw their margins plummet.

In Q1, Scorpio Tankers generated an operating margin profit margin of 70.2%, up 40.6 percentage points year on year. The increase was solid and shows its expenses recently grew slower than its revenue, leading to higher efficiency.

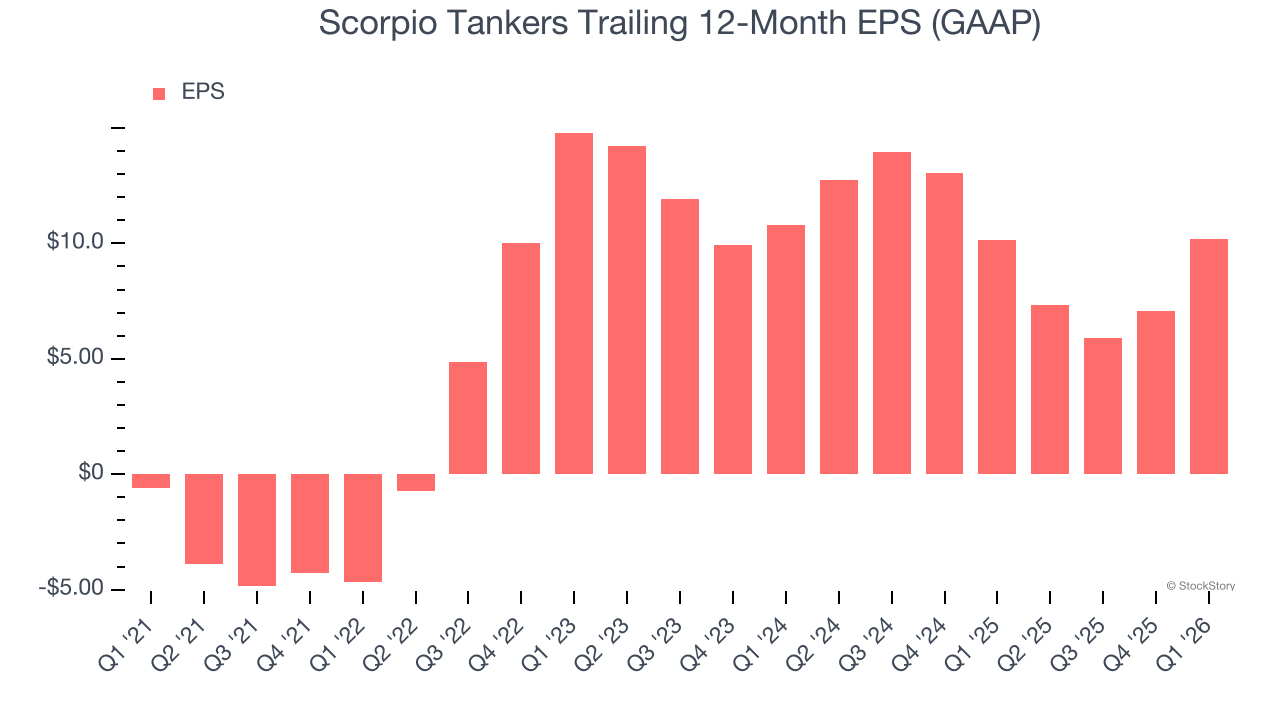

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Scorpio Tankers’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Scorpio Tankers, its EPS and revenue declined by 2.9% and 13.2% annually over the last two years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Scorpio Tankers’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, Scorpio Tankers reported EPS of $4.32, up from $1.22 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Scorpio Tankers’s full-year EPS of $10.17 to shrink by 24%.

Key Takeaways from Scorpio Tankers’s Q1 Results

It was good to see Scorpio Tankers beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 2.7% to $85.50 immediately following the results.

Scorpio Tankers may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).