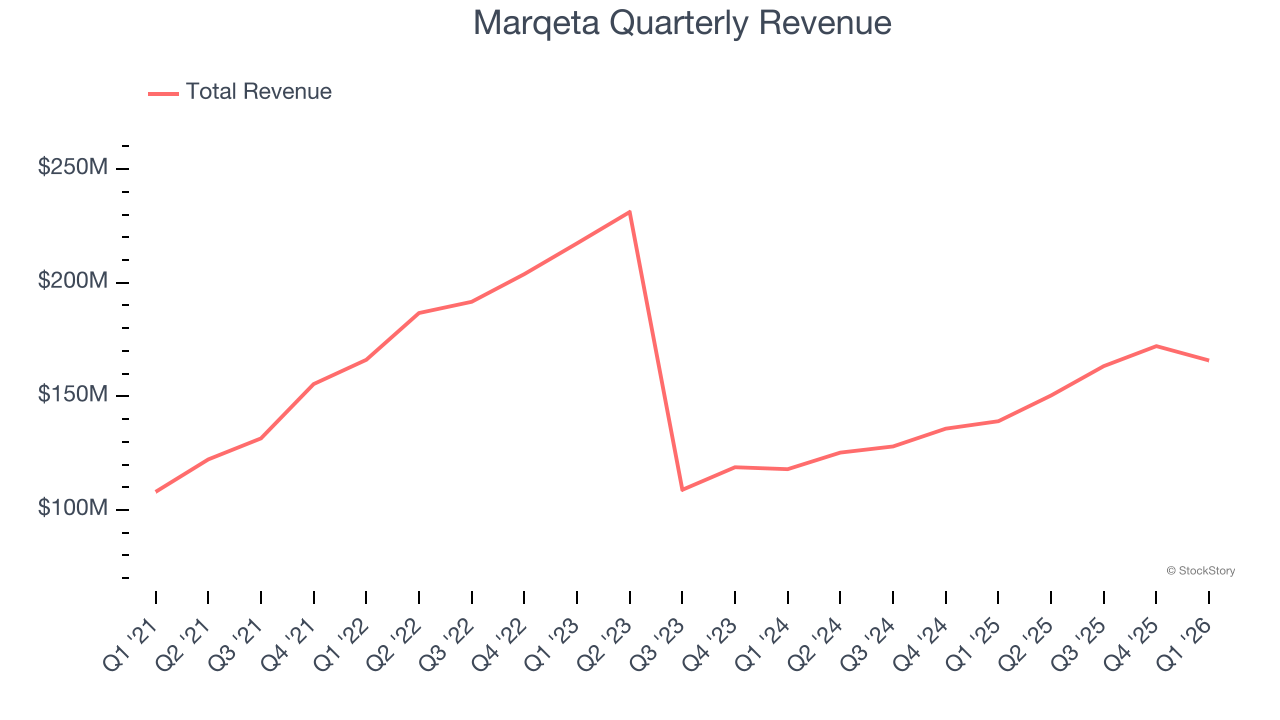

Payment technology company Marqeta (NASDAQ:MQ) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 19.2% year on year to $165.8 million. Its GAAP profit of $0.02 per share was $0.02 above analysts’ consensus estimates.

Is now the time to buy Marqeta? Find out by accessing our full research report, it’s free.

Marqeta (MQ) Q1 CY2026 Highlights:

- Revenue: $165.8 million vs analyst estimates of $164.3 million (19.2% year-on-year growth, 0.9% beat)

- EPS (GAAP): $0.02 vs analyst estimates of $0 ($0.02 beat)

- Adjusted Operating Income: $22.11 million vs analyst estimates of -$11.33 million (13.3% margin, significant beat)

- Operating Margin: 1.3%, up from -13.3% in the same quarter last year

- Free Cash Flow was -$12.44 million, down from $46.52 million in the previous quarter

- Market Capitalization: $1.92 billion

Company Overview

Powering the cards behind innovative fintech services like Block's Cash App, Marqeta (NASDAQ:MQ) provides a cloud-based platform that allows businesses to create customized payment card programs and process card transactions.

Revenue Growth

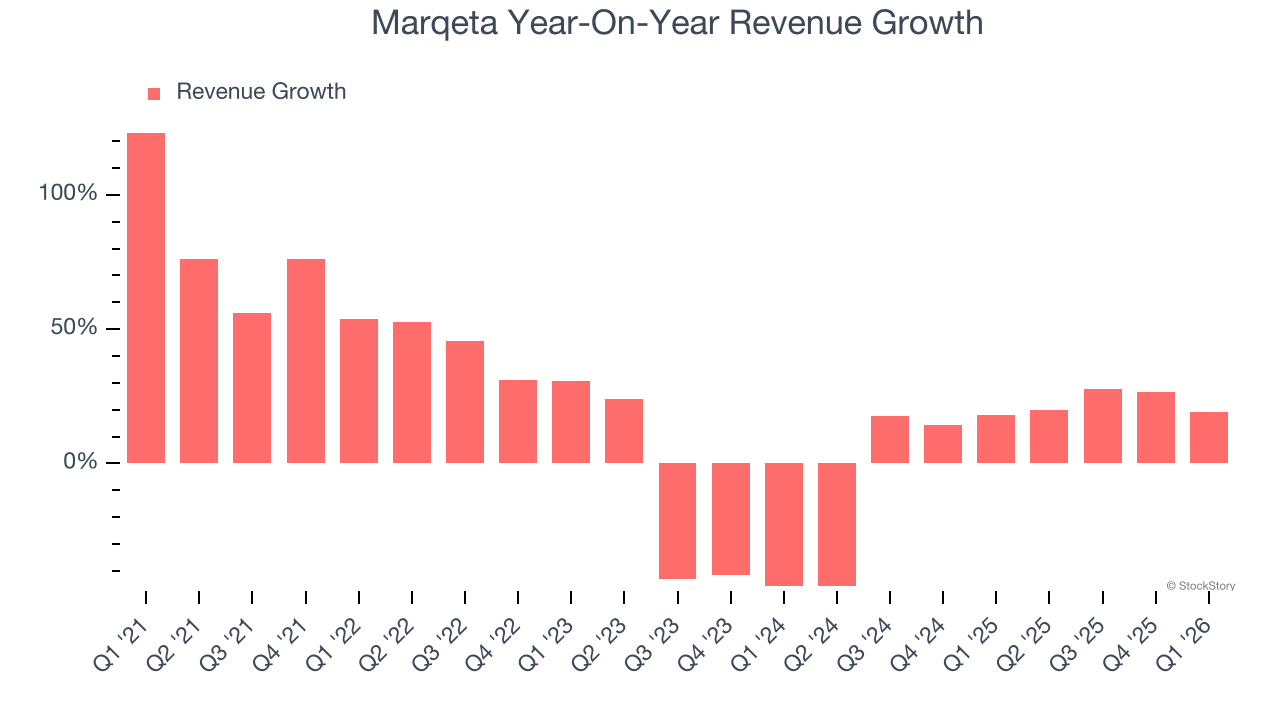

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Marqeta grew its sales at a 13.2% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Marqeta’s recent performance shows its demand has slowed as its annualized revenue growth of 6.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Marqeta reported year-on-year revenue growth of 19.2%, and its $165.8 million of revenue exceeded Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to grow 12.5% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

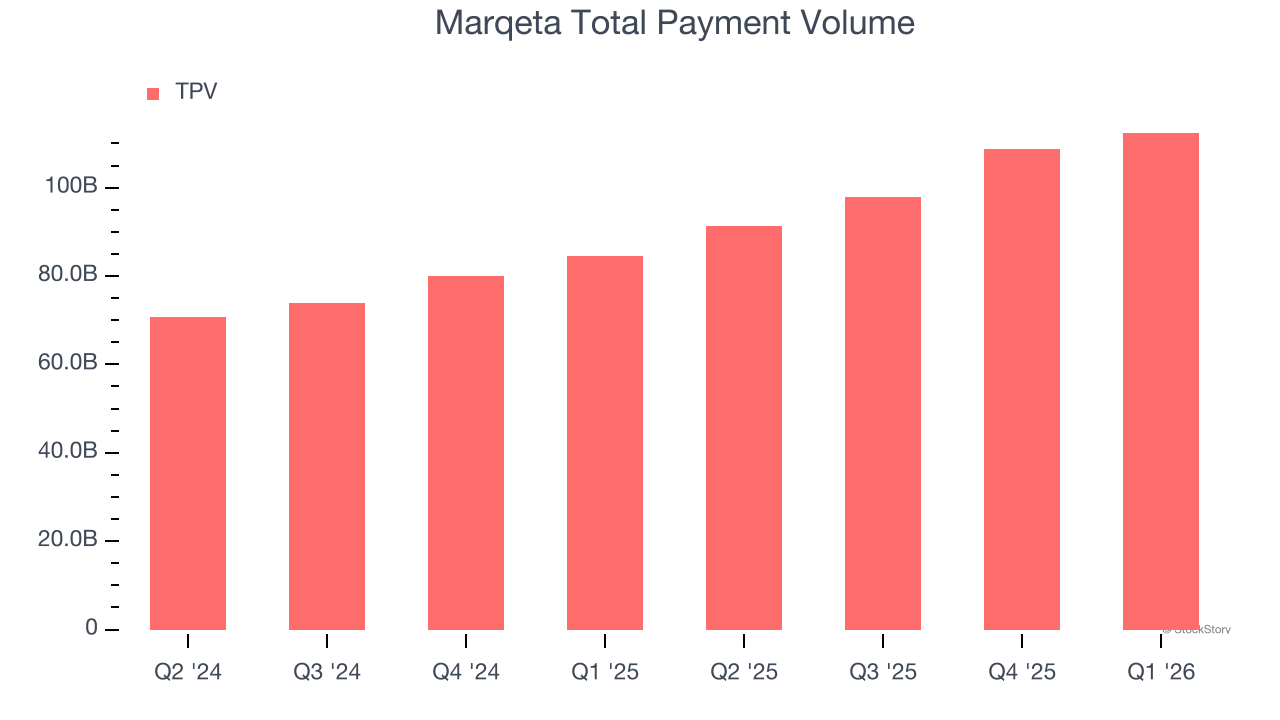

Total Payment Volume

TPV, or total processing volume, is the aggregate dollar value of transactions flowing through Marqeta’s platform. This is the number from which the company will ultimately collect fees, and the higher it is, the more chances Marqeta has to upsell additional services (like banking).

Marqeta’s TPV punched in at $112.4 billion in Q1, and over the last four quarters, its growth was fantastic as it averaged 32.7% year-on-year increases. This alternate topline metric grew faster than total sales, which could mean that take rates have declined. However, we can’t automatically assume the company is reducing its fees because take rates can also vary depending on the type of products sold on its platform.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Marqeta’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Marqeta’s Q1 Results

We were impressed by how significantly Marqeta blew past analysts’ EBITDA expectations this quarter. Zooming out, we think this quarter featured some important positives. Investors were likely hoping for more, and shares traded down 2.1% to $4.38 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).