Telecommunications infrastructure company Lumen Technologies (NYSE:LUMN) reported Q1 CY2026 results topping the market’s revenue expectations, but sales fell by 8.9% year on year to $2.90 billion. Its non-GAAP loss of $0.47 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Lumen? Find out by accessing our full research report, it’s free.

Lumen (LUMN) Q1 CY2026 Highlights:

- Revenue: $2.90 billion vs analyst estimates of $2.83 billion (8.9% year-on-year decline, 2.3% beat)

- Adjusted EPS: -$0.47 vs analyst estimates of -$0.10 (significant miss)

- Adjusted EBITDA: $1.28 billion vs analyst estimates of $791.3 million (44.1% margin, 61.6% beat)

- EBITDA guidance for the full year is $3.2 billion at the midpoint, in line with analyst expectations

- Operating Margin: 20.8%, up from 3.4% in the same quarter last year

- Free Cash Flow Margin: 13.1%, up from 11.1% in the same quarter last year

- Market Capitalization: $9.61 billion

“Our strategy is working and we continue to progress towards our key financial goals we set out at Investor Day,” said Lumen CEO Kate Johnson.

Company Overview

With approximately 350,000 route miles of fiber optic cable spanning North America and the Asia Pacific, Lumen Technologies (NYSE:LUMN) operates a vast fiber optic network that provides communications, cloud connectivity, security, and IT solutions to businesses and consumers.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $12.12 billion in revenue over the past 12 months, Lumen is larger than most business services companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. For Lumen to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

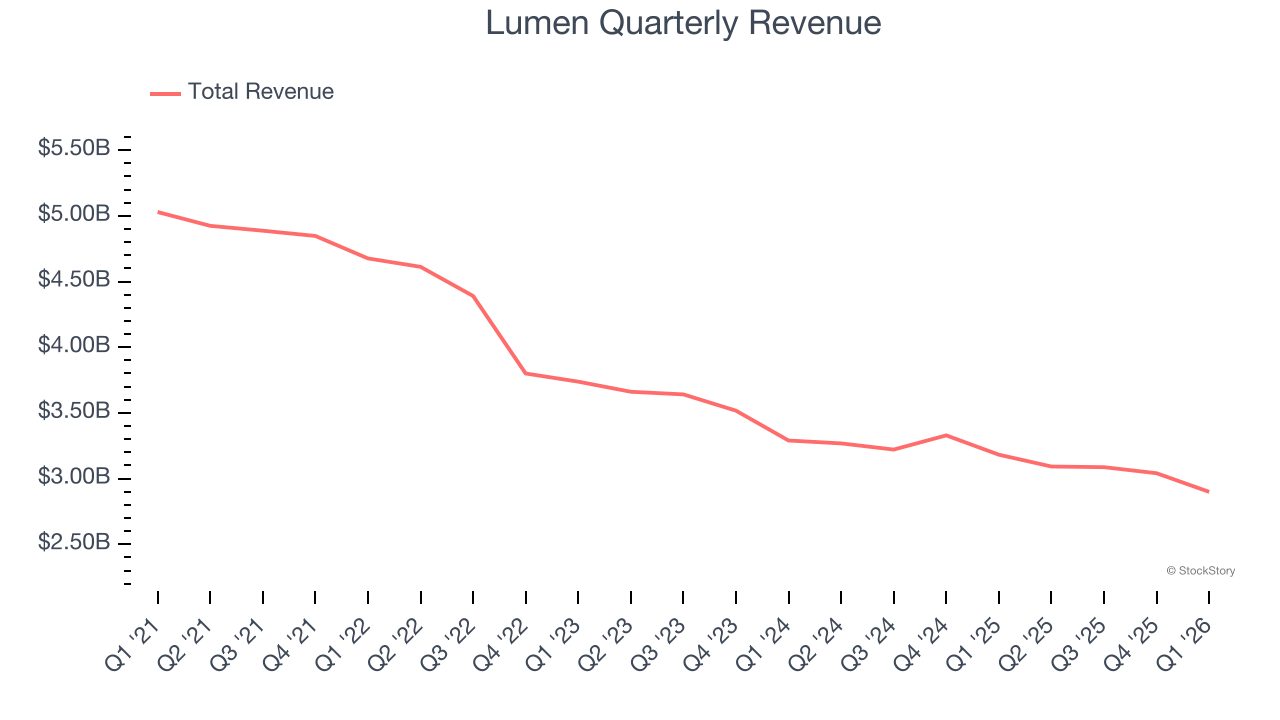

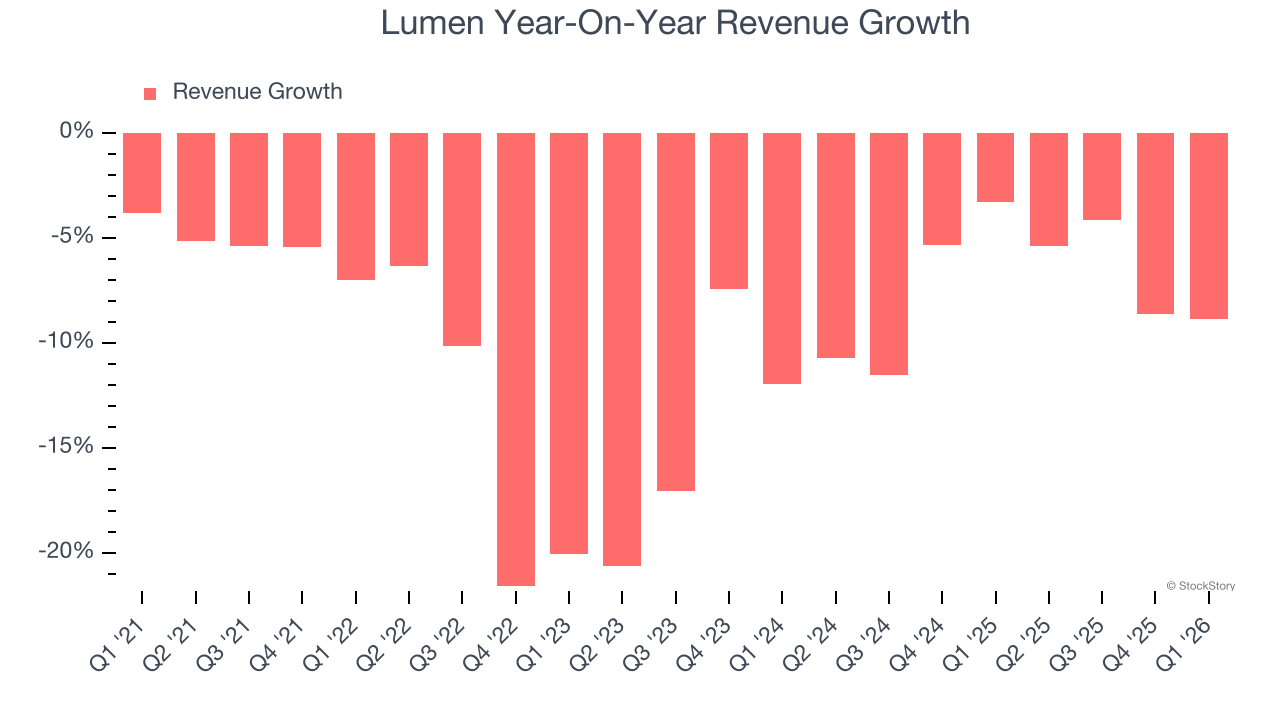

As you can see below, Lumen struggled to generate demand over the last five years. Its sales dropped by 10% annually, a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Lumen’s annualized revenue declines of 7.3% over the last two years suggest its demand continued shrinking.

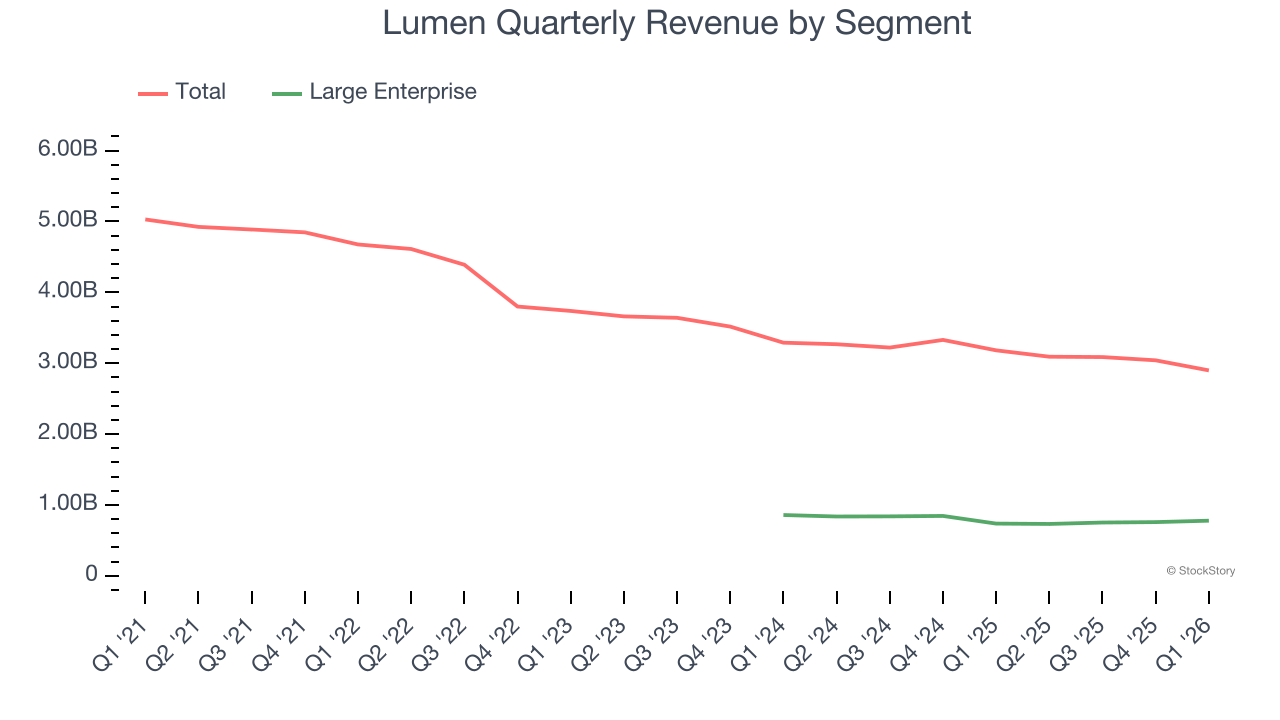

We can better understand the company’s revenue dynamics by analyzing its most important segment, Large Enterprise. Over the last two years, Lumen’s Large Enterprise revenue (services provided to businesses) averaged 8.3% year-on-year declines. This segment has lagged the company’s overall sales.

This quarter, Lumen’s revenue fell by 8.9% year on year to $2.90 billion but beat Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to decline by 11.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

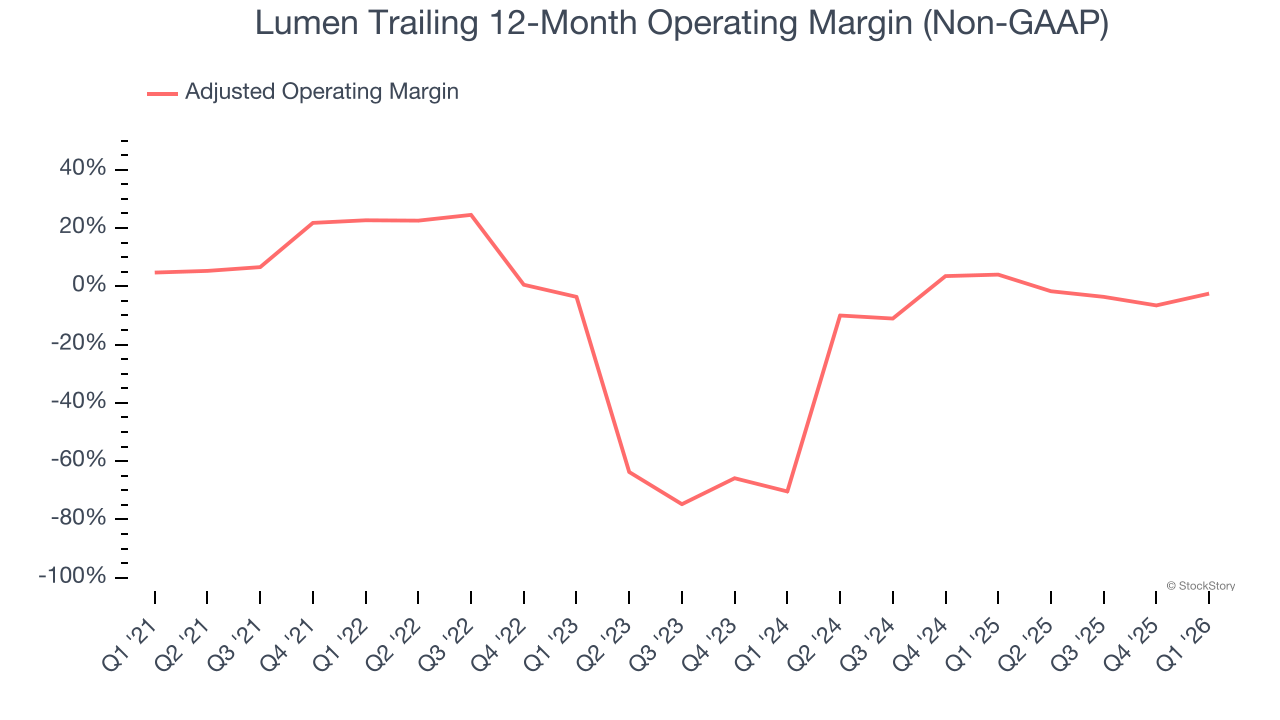

Although Lumen was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average adjusted operating margin of negative 7.9% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Lumen’s adjusted operating margin decreased by 25.2 percentage points over the last five years. Lumen’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Lumen generated an adjusted operating margin profit margin of 21.2%, up 17.9 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

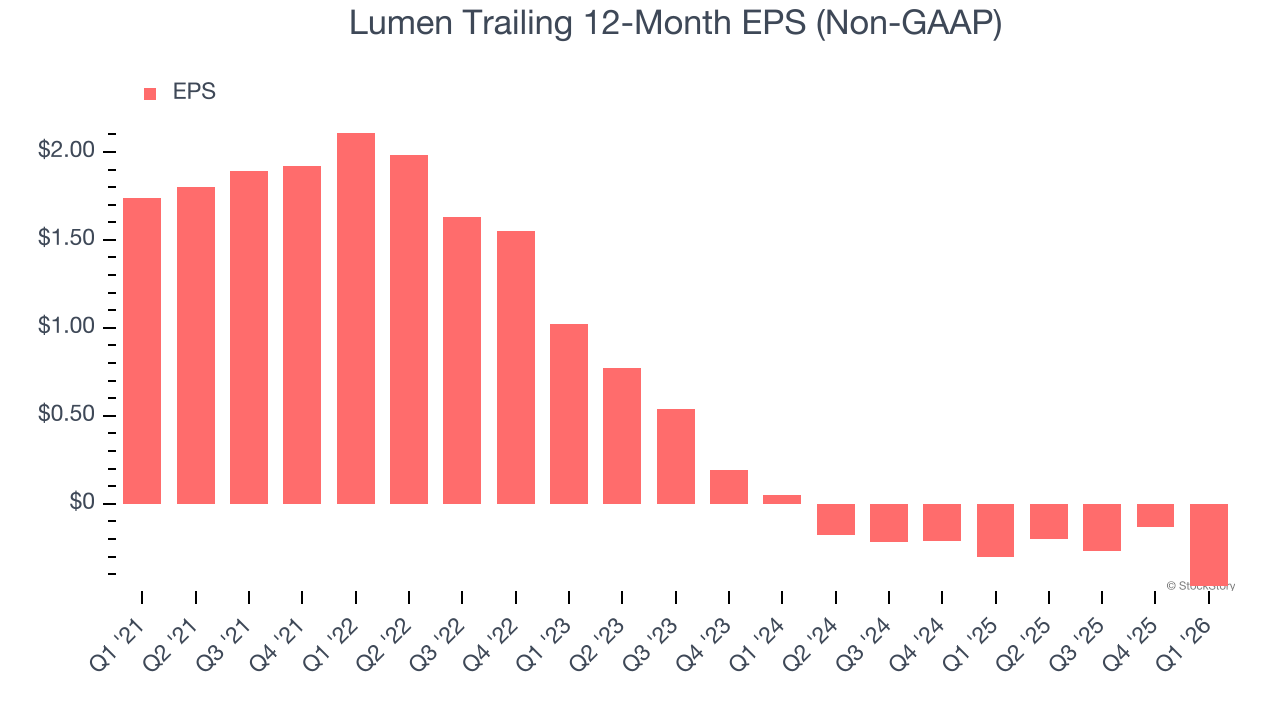

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Lumen, its EPS declined by 17.8% annually over the last five years, more than its revenue. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its adjusted operating margin and repurchased its shares during this time.

Diving into the nuances of Lumen’s earnings can give us a better understanding of its performance. As we mentioned earlier, Lumen’s adjusted operating margin expanded this quarter but declined by 25.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Lumen’s two-year annual EPS declines of 238% were bad and lower than its two-year revenue losses.

In Q1, Lumen reported adjusted EPS of negative $0.47, down from negative $0.13 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Lumen’s Q1 Results

It was encouraging to see Lumen beat analysts’ revenue and EBITDA expectations this quarter. Looking ahead, EBITDA guidance was in line. Overall, this was a decent quarter. The stock traded up 2.1% to $9.41 immediately following the results.

So do we think Lumen is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).