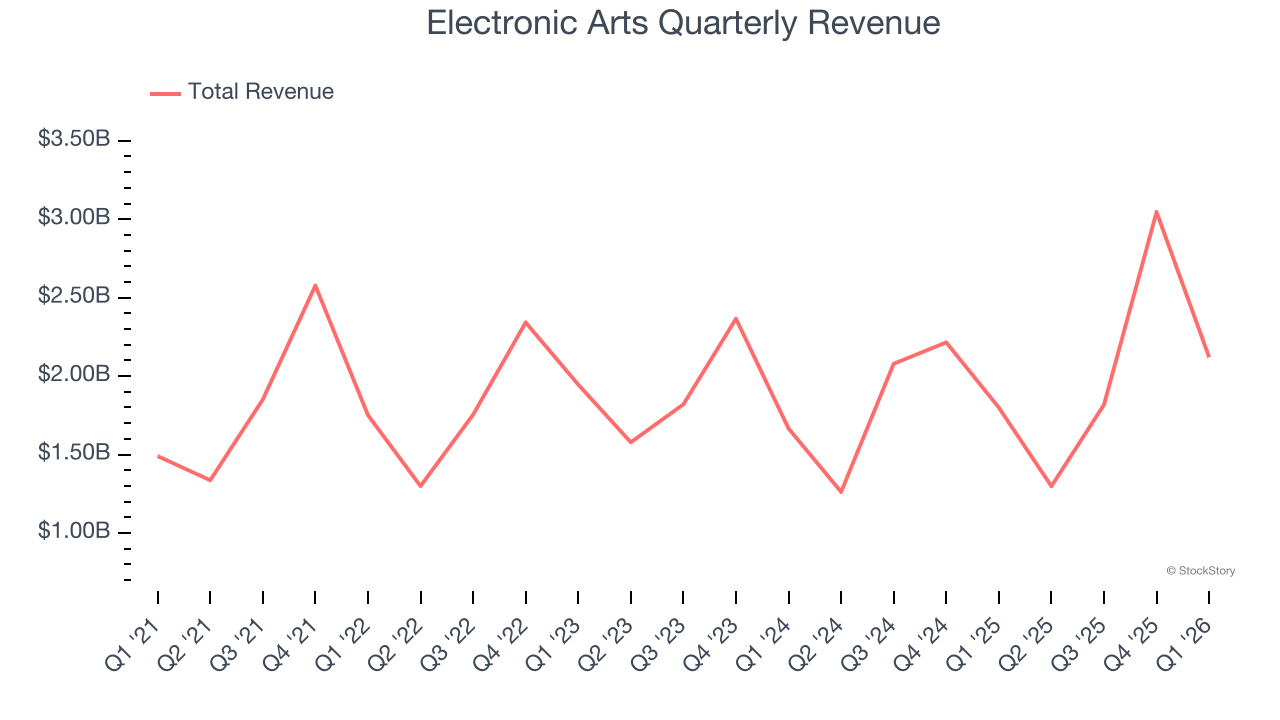

Video game publisher Electronic Arts (NASDAQ:EA) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 17.8% year on year to $2.12 billion. Its GAAP profit of $1.81 per share was 39.6% above analysts’ consensus estimates.

Is now the time to buy Electronic Arts? Find out by accessing our full research report, it’s free.

Electronic Arts (EA) Q1 CY2026 Highlights:

- Revenue: $2.12 billion vs analyst estimates of $2.02 billion (17.8% year-on-year growth, 5.2% beat)

- EPS (GAAP): $1.81 vs analyst estimates of $1.30 (39.6% beat)

- Adjusted EBITDA: $799 million vs analyst estimates of $804.9 million (37.7% margin, 0.7% miss)

- Operating Margin: 26.6%, up from 22% in the same quarter last year

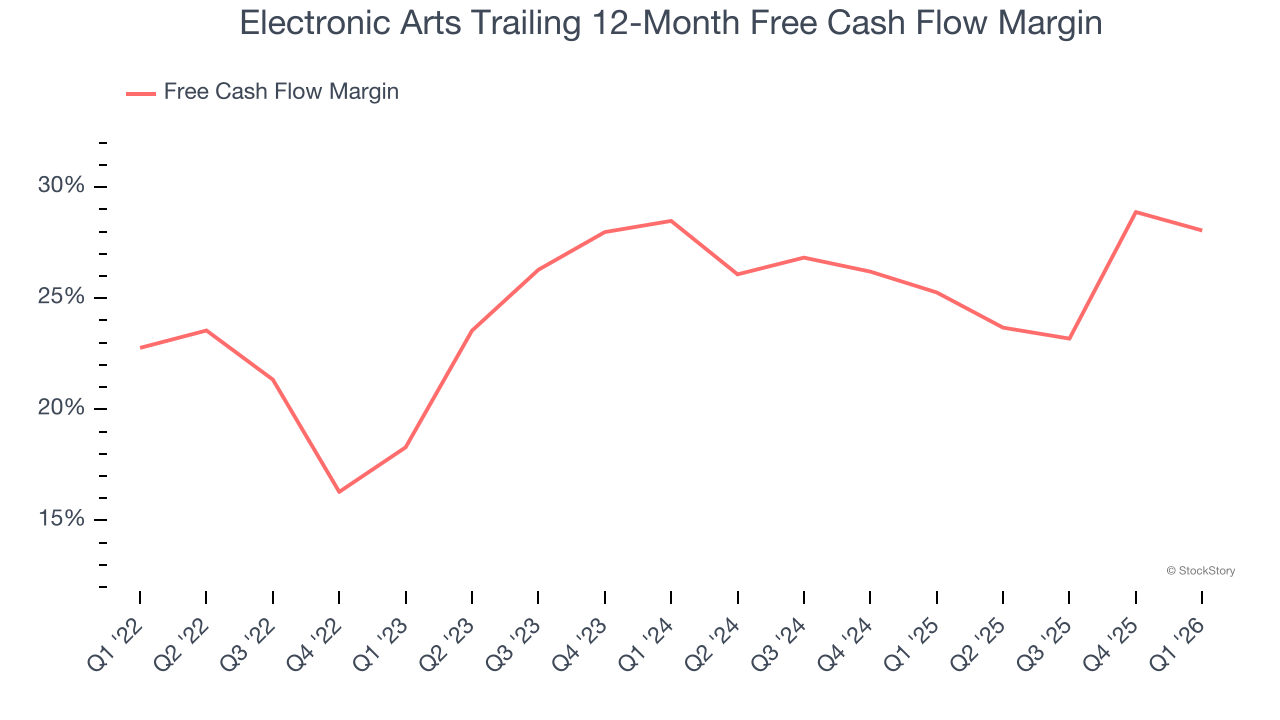

- Free Cash Flow Margin: 24.5%, down from 58.2% in the previous quarter

- Market Capitalization: $50.51 billion

Company Overview

Best known for its Madden NFL and FIFA sports franchises, Electronic Arts (NASDAQ:EA) is one of the world’s largest video game publishers.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Electronic Arts grew its sales at a sluggish 4.1% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Electronic Arts.

This quarter, Electronic Arts reported year-on-year revenue growth of 17.8%, and its $2.12 billion of revenue exceeded Wall Street’s estimates by 5.2%.

Looking ahead, sell-side analysts expect revenue to grow 2.9% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Electronic Arts has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 26.7% over the last two years.

Taking a step back, we can see that Electronic Arts’s margin expanded by 9.8 percentage points over the last few years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Electronic Arts’s free cash flow clocked in at $519 million in Q1, equivalent to a 24.5% margin. The company’s cash profitability regressed as it was 3 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Electronic Arts’s Q1 Results

We enjoyed seeing Electronic Arts beat analysts’ revenue expectations this quarter. On the other hand, its EBITDA slightly missed. Overall, this print had some key positives. The stock remained flat at $201.10 immediately after reporting.

So do we think Electronic Arts is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).