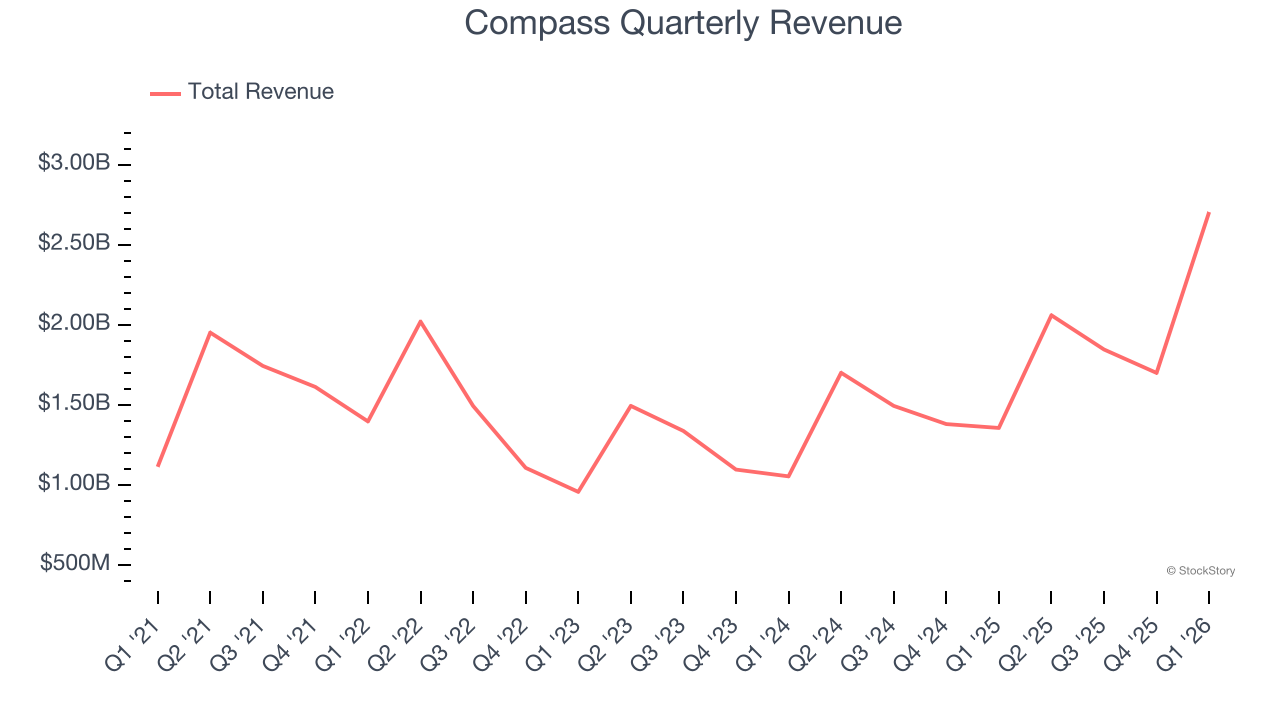

Real estate technology company Compass (NYSE:COMP) announced better-than-expected revenue in Q1 CY2026, with sales up 99.4% year on year to $2.70 billion. On top of that, next quarter’s revenue guidance ($4.1 billion at the midpoint) was surprisingly good and 3.6% above what analysts were expecting. Its GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Compass? Find out by accessing our full research report, it’s free.

Compass (COMP) Q1 CY2026 Highlights:

- Revenue: $2.70 billion vs analyst estimates of $2.67 billion (99.4% year-on-year growth, 1.2% beat)

- EPS (GAAP): $0.03 vs analyst estimates of -$0.16 (significant beat)

- Adjusted EBITDA: $61 million vs analyst estimates of $26.66 million (2.3% margin, significant beat)

- Revenue Guidance for Q2 CY2026 is $4.1 billion at the midpoint, above analyst estimates of $3.96 billion

- EBITDA guidance for Q2 CY2026 is $330 million at the midpoint, above analyst estimates of $306.6 million

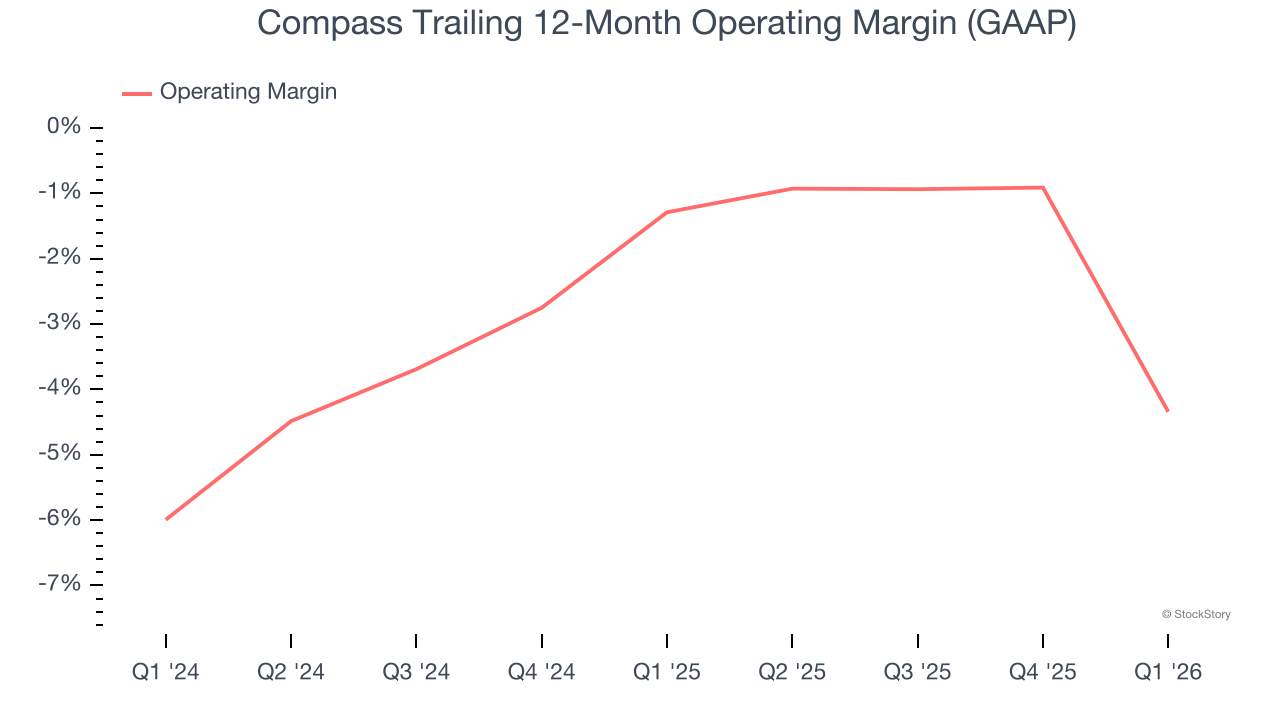

- Operating Margin: -13%, down from -4% in the same quarter last year

- Free Cash Flow was -$168 million, down from $19.5 million in the same quarter last year

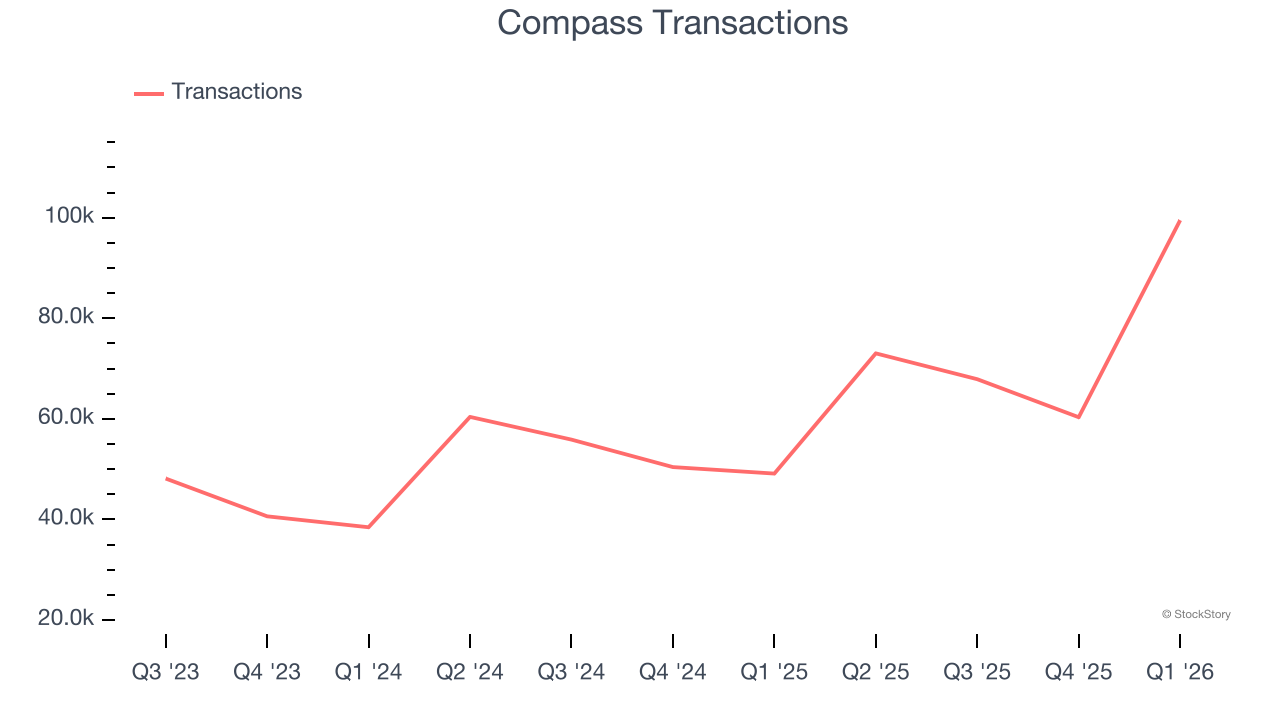

- Transactions: up 50,383 year on year

- Market Capitalization: $5.27 billion

Company Overview

Fueled by its mission to replace the "paper-driven, antiquated workflow" of buying a house, Compass (NYSE:COMP) is a digital-first company operating a residential real estate brokerage in the United States.

Revenue Growth

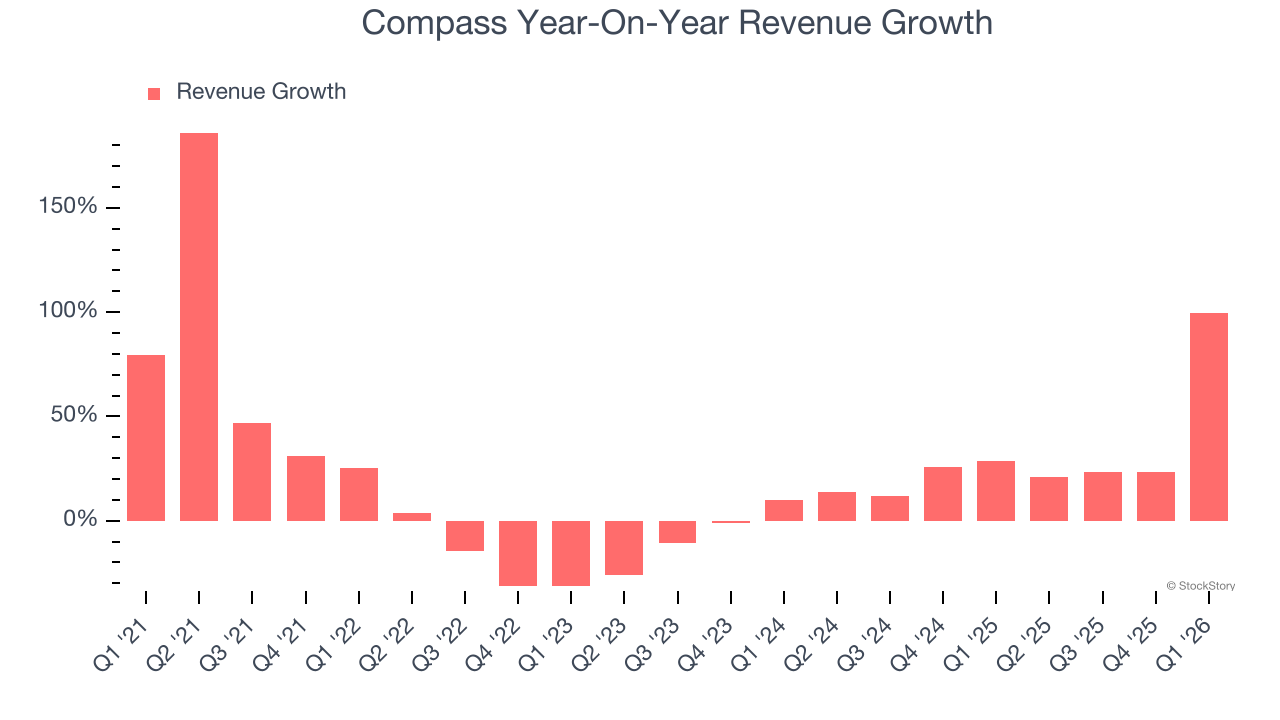

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Compass grew its sales at a 14.5% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Compass’s annualized revenue growth of 29.1% over the last two years is above its five-year trend, which is encouraging.

We can better understand the company’s revenue dynamics by analyzing its number of transactions, which reached 99,504 in the latest quarter. Over the last two years, Compass’s transactions averaged 33.2% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Compass reported magnificent year-on-year revenue growth of 99.4%, and its $2.70 billion of revenue beat Wall Street’s estimates by 1.2%. Company management is currently guiding for a 99.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 67.6% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will spur better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Compass’s operating margin has shrunk over the last 12 months and averaged negative 3.1% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

In Q1, Compass generated a negative 13% operating margin. The company's consistent lack of profits raise a flag.

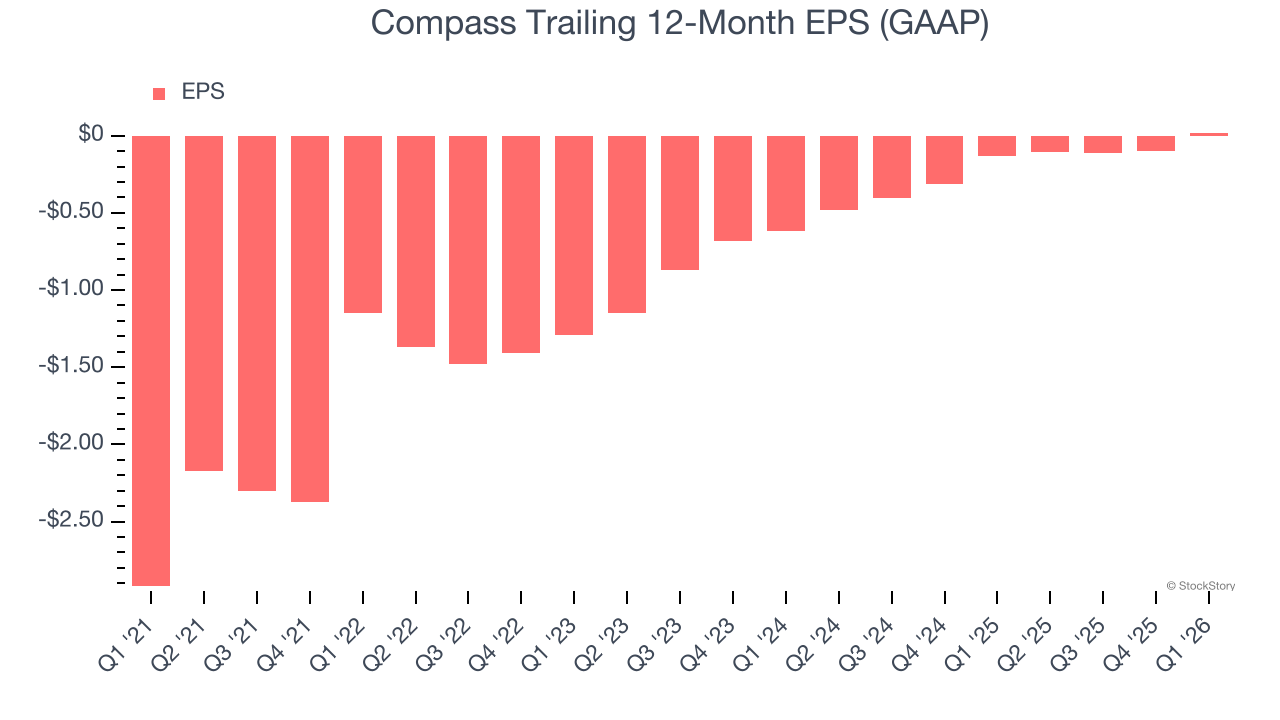

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Compass’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Compass reported EPS of $0.03, up from negative $0.09 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Compass’s full-year EPS of $0.02 to grow 2,014%.

Key Takeaways from Compass’s Q1 Results

We were impressed by Compass’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 17.6% to $8.54 immediately following the results.

Compass put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).