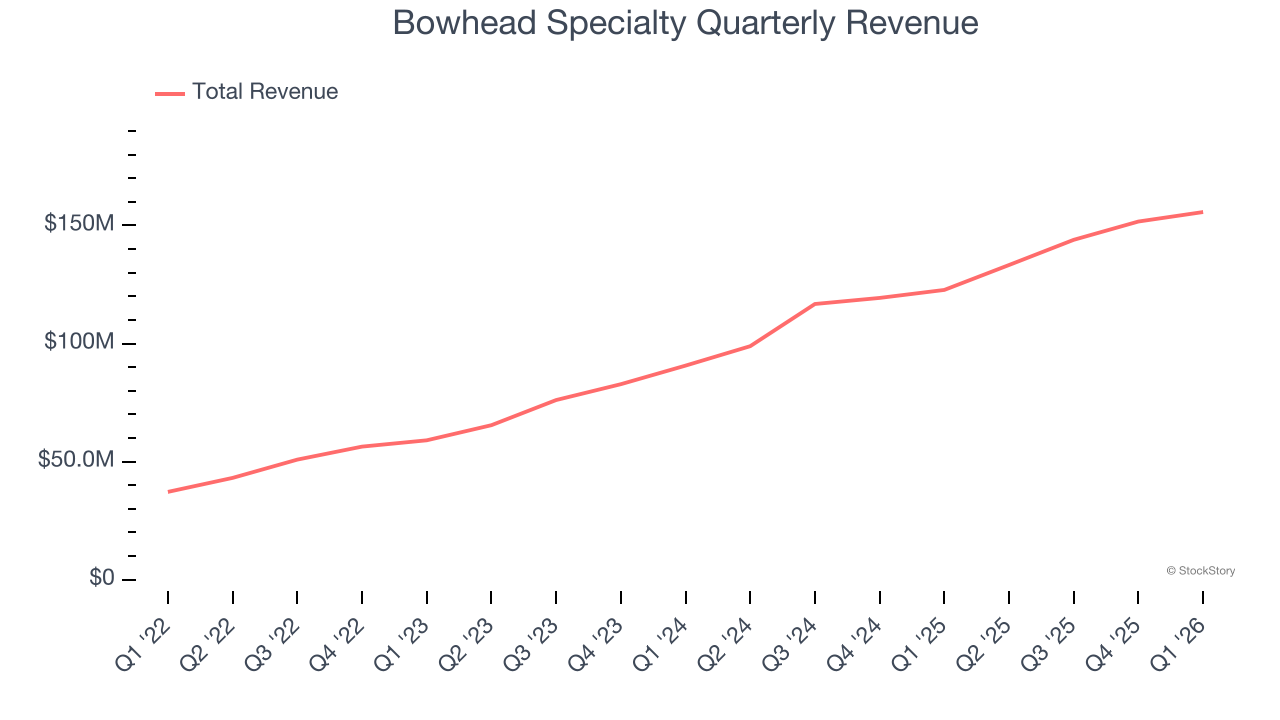

Specialty insurance company Bowhead Specialty Holdings (NYSE:BOW) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 26.9% year on year to $155.7 million. Its GAAP profit of $0.48 per share was 18.5% above analysts’ consensus estimates.

Is now the time to buy Bowhead Specialty? Find out by accessing our full research report, it’s free.

Bowhead Specialty (BOW) Q1 CY2026 Highlights:

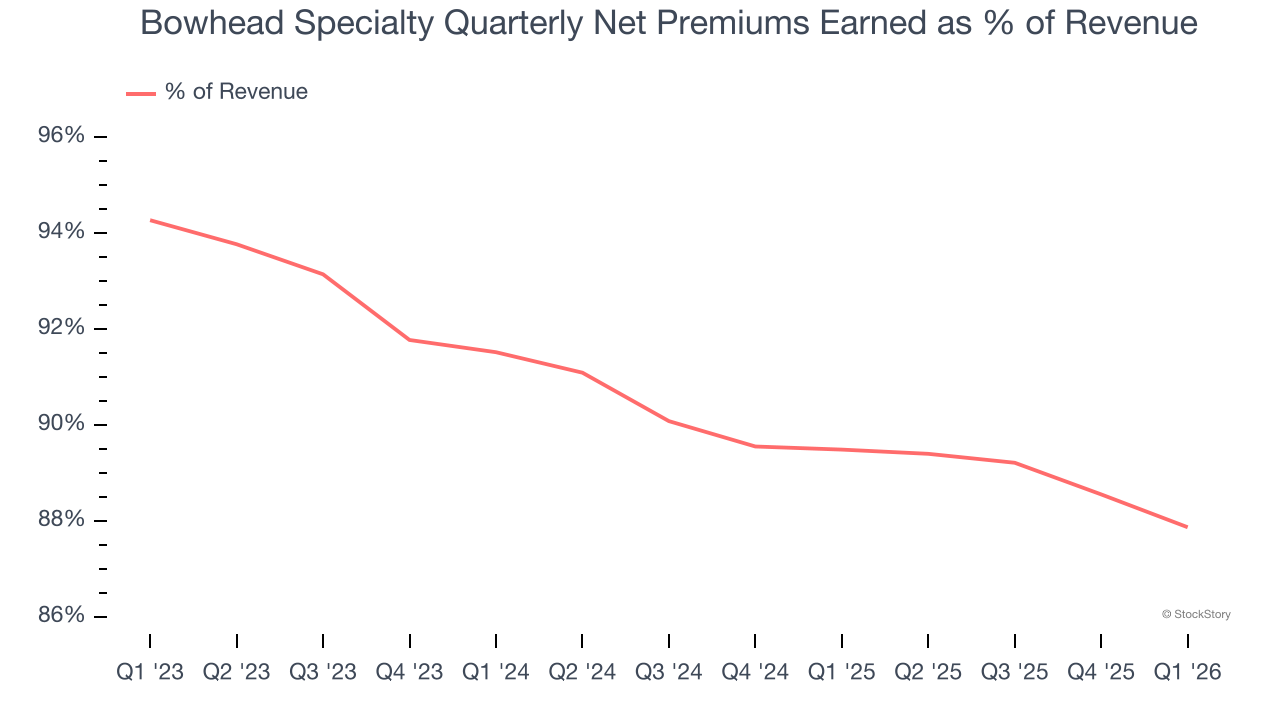

- Net Premiums Earned: $136.8 million vs analyst estimates of $133.3 million (24.6% year-on-year growth, 2.7% beat)

- Revenue: $155.7 million vs analyst estimates of $147.6 million (26.9% year-on-year growth, 5.5% beat)

- Combined Ratio: 95.3% vs analyst estimates of 97.7% (236.7 basis point beat)

- EPS (GAAP): $0.48 vs analyst estimates of $0.41 (18.5% beat)

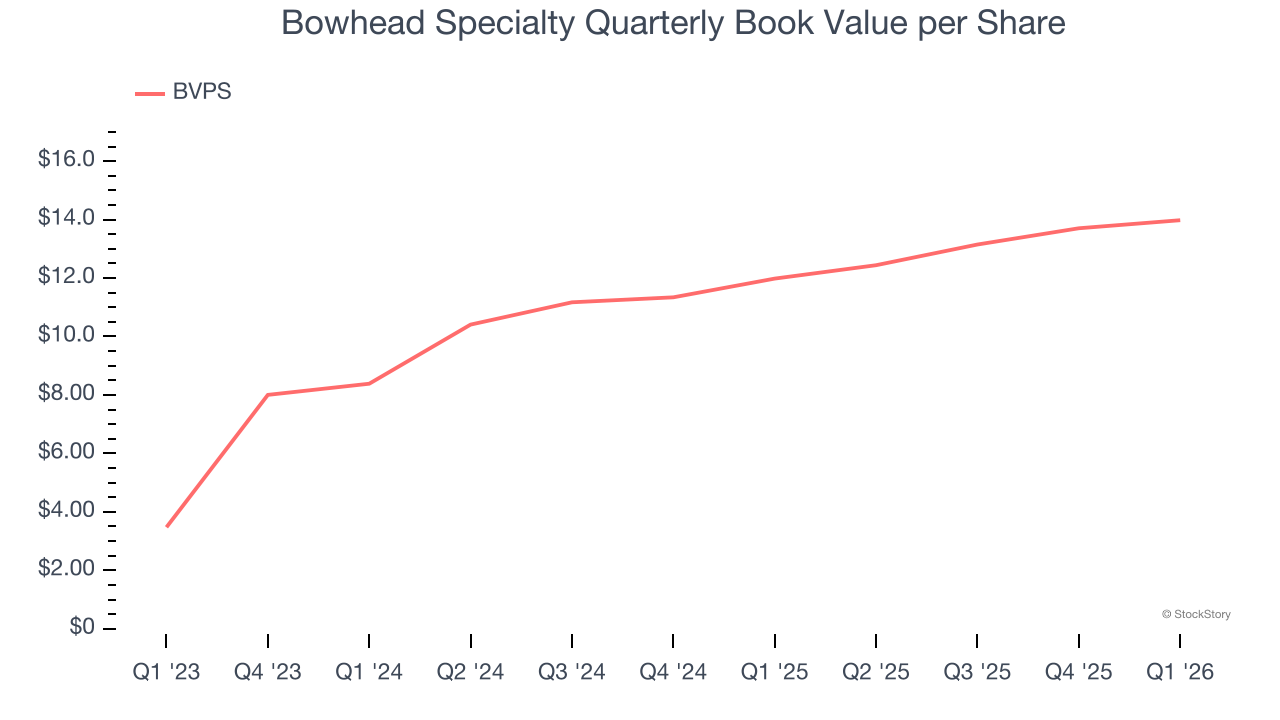

- Book Value per Share: $13.98 (16.7% year-on-year growth)

- Market Capitalization: $764.5 million

Bowhead Chief Executive Officer, Stephen Sills, commented, “We are very pleased with our strong start to 2026, delivering a 24% growth in gross written premiums in the first quarter. This performance was driven by the disciplined premium growth achieved in our Casualty portfolio and the strong execution in Baleen within our digital underwriting platform. As we look ahead, we remain focused on our strategy of building a balanced portfolio of craft and digital solutions to deliver sustainable and profitable growth across market cycles. Brandon Mezick, our Head of Digital, will join today’s earnings call to share how our digital underwriting platform supports this strategy and strengthens our competitive position.”

Company Overview

Named after the Arctic bowhead whale known for navigating challenging waters, Bowhead Specialty Holdings (NYSE:BOW) is a specialty insurance company that provides customized coverage for complex and high-risk commercial sectors.

Revenue Growth

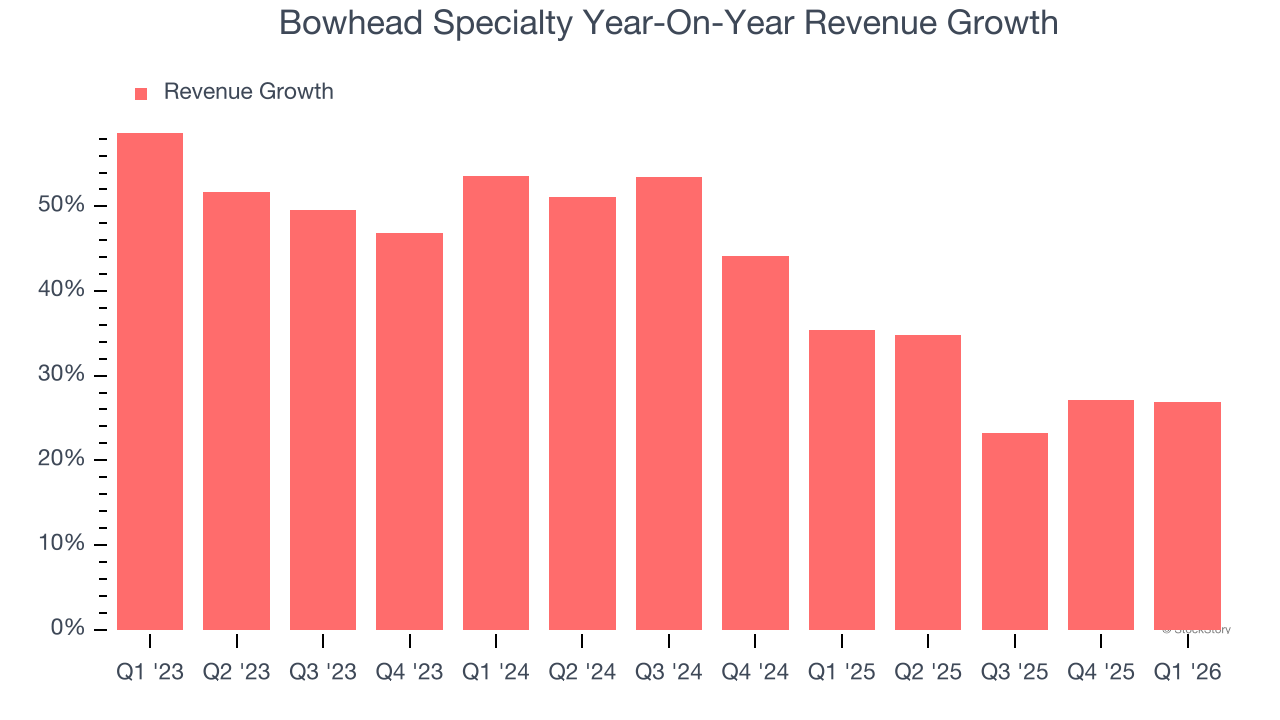

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services. Thankfully, Bowhead Specialty’s 43.4% annualized revenue growth over the last three years was incredible. Its growth surpassed the average insurance company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. Bowhead Specialty’s annualized revenue growth of 36.2% over the last two years is below its three-year trend, but we still think the results suggest healthy demand.

This quarter, Bowhead Specialty reported robust year-on-year revenue growth of 26.9%, and its $155.7 million of revenue topped Wall Street estimates by 5.5%.

Net premiums earned made up 90.2% of the company’s total revenue during the last four years, meaning Bowhead Specialty lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

Fortunately for investors, Bowhead Specialty’s BVPS grew at an incredible 29.1% annual clip over the last two years.

Key Takeaways from Bowhead Specialty’s Q1 Results

We were impressed by how significantly Bowhead Specialty blew past analysts’ net premiums earned expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 6% to $24.68 immediately after reporting.

Sure, Bowhead Specialty had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).