Agricultural and farm machinery company AGCO (NYSE:AGCO) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 14.3% year on year to $2.34 billion. The company’s full-year revenue guidance of $10.6 billion at the midpoint came in 0.6% above analysts’ estimates. Its GAAP profit of $0.76 per share was 91.2% above analysts’ consensus estimates.

Is now the time to buy AGCO? Find out by accessing our full research report, it’s free.

AGCO (AGCO) Q1 CY2026 Highlights:

- Revenue: $2.34 billion vs analyst estimates of $2.26 billion (14.3% year-on-year growth, 3.8% beat)

- EPS (GAAP): $0.76 vs analyst estimates of $0.40 (91.2% beat)

- Adjusted Operating Income: $91.1 million vs analyst estimates of $90.12 million (3.9% margin, 1.1% beat)

- The company slightly lifted its revenue guidance for the full year to $10.6 billion at the midpoint from $10.55 billion

- EPS (GAAP) guidance for the full year is $6 at the midpoint, beating analyst estimates by 5.4%

- Operating Margin: 3.4%, up from 2.4% in the same quarter last year

- Free Cash Flow was -$455 million compared to -$260.4 million in the same quarter last year

- Market Capitalization: $8.78 billion

"AGCO delivered healthy first‑quarter sales and margin results, reflecting disciplined execution in a demanding agricultural market and dynamic global environment," said Eric Hansotia, AGCO's Chairman, President and CEO.

Company Overview

With a history that features both organic growth and acquisitions, AGCO (NYSE:AGCO) designs, manufactures, and sells agricultural machinery and related technology.

Revenue Growth

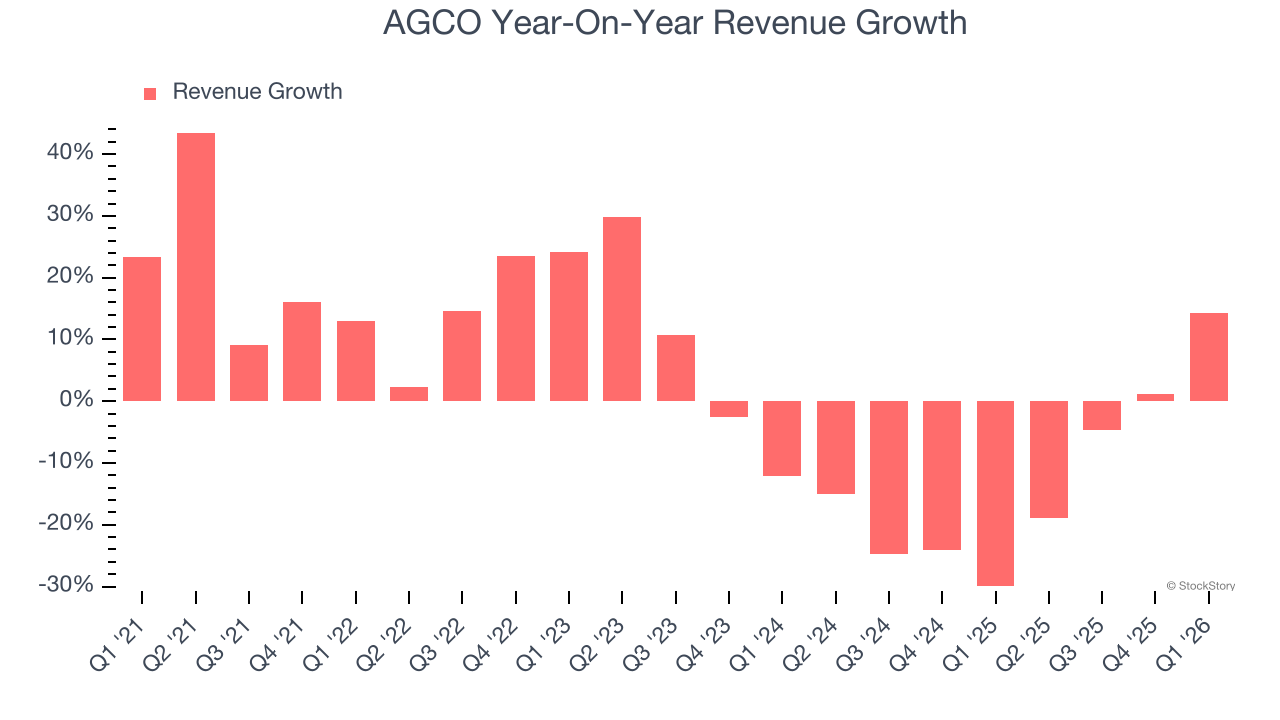

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, AGCO’s 1.6% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. AGCO’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 13.9% annually.

This quarter, AGCO reported year-on-year revenue growth of 14.3%, and its $2.34 billion of revenue exceeded Wall Street’s estimates by 3.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

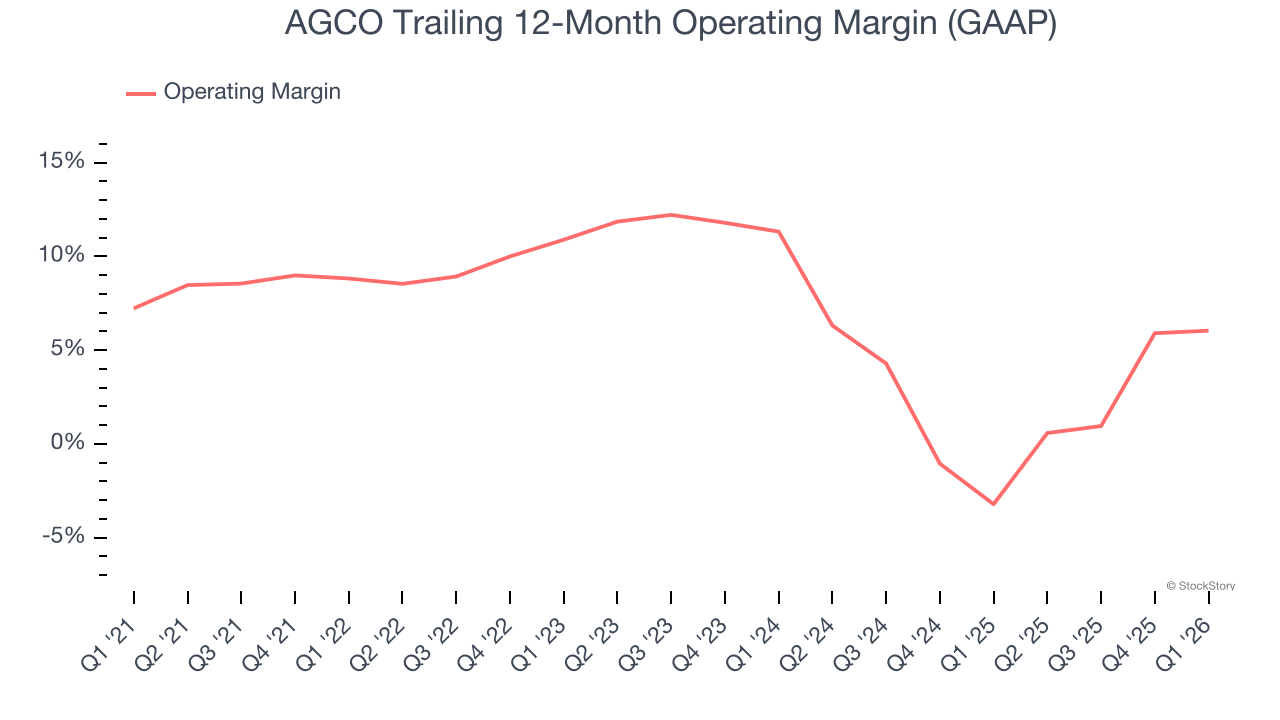

AGCO was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.2% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, AGCO’s operating margin decreased by 2.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. AGCO’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, AGCO generated an operating margin profit margin of 3.4%, up 1 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

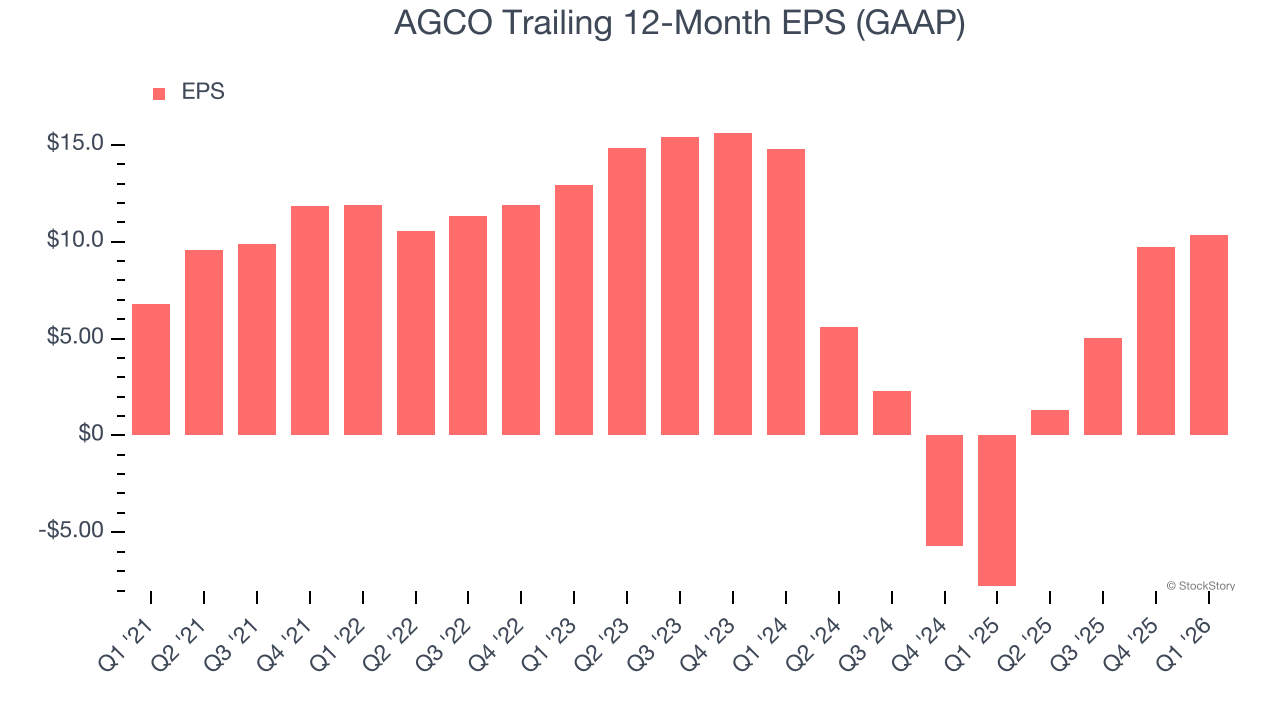

AGCO’s EPS grew at 8.8% compounded annual growth rate over the last five years, higher than its 1.6% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

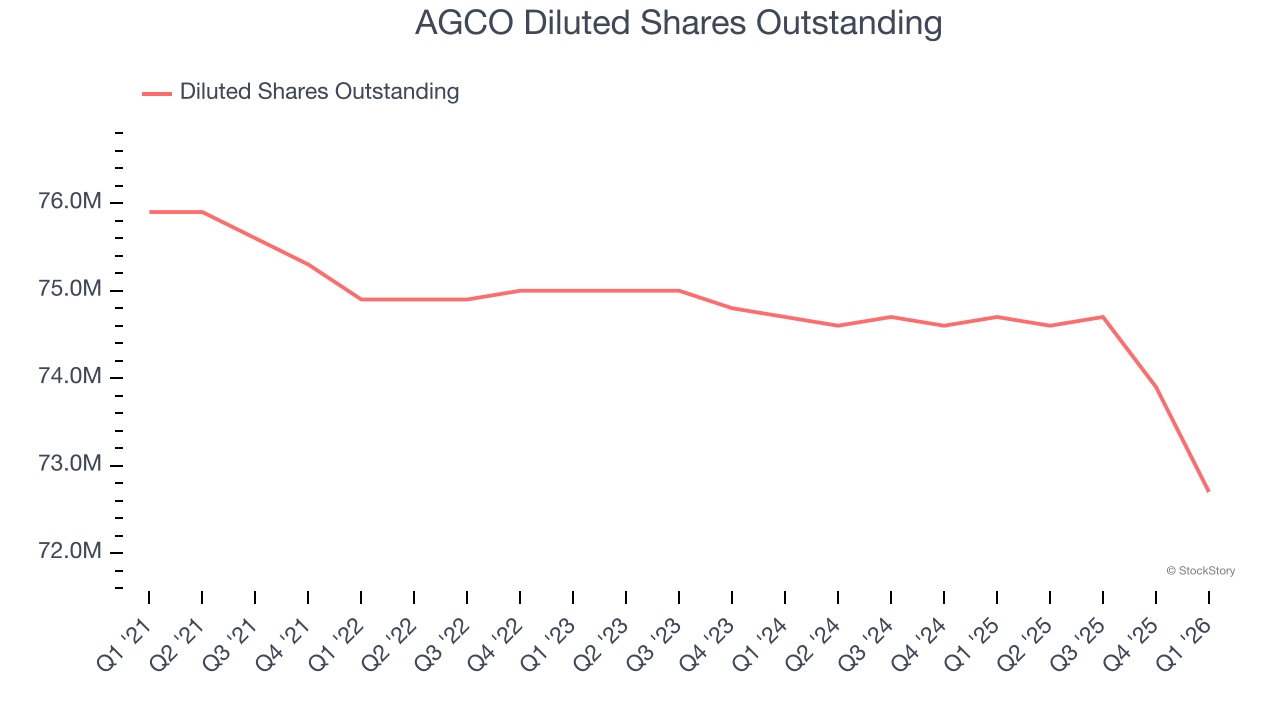

Diving into the nuances of AGCO’s earnings can give us a better understanding of its performance. A five-year view shows that AGCO has repurchased its stock, shrinking its share count by 4.2%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For AGCO, its two-year annual EPS declines of 16.3% mark a reversal from its five-year trend. We hope AGCO can return to earnings growth in the future.

In Q1, AGCO reported EPS of $0.76, up from $0.14 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects AGCO’s full-year EPS of $10.36 to shrink by 39.3%.

Key Takeaways from AGCO’s Q1 Results

It was good to see AGCO beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 2% to $123.75 immediately after reporting.

Indeed, AGCO had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).