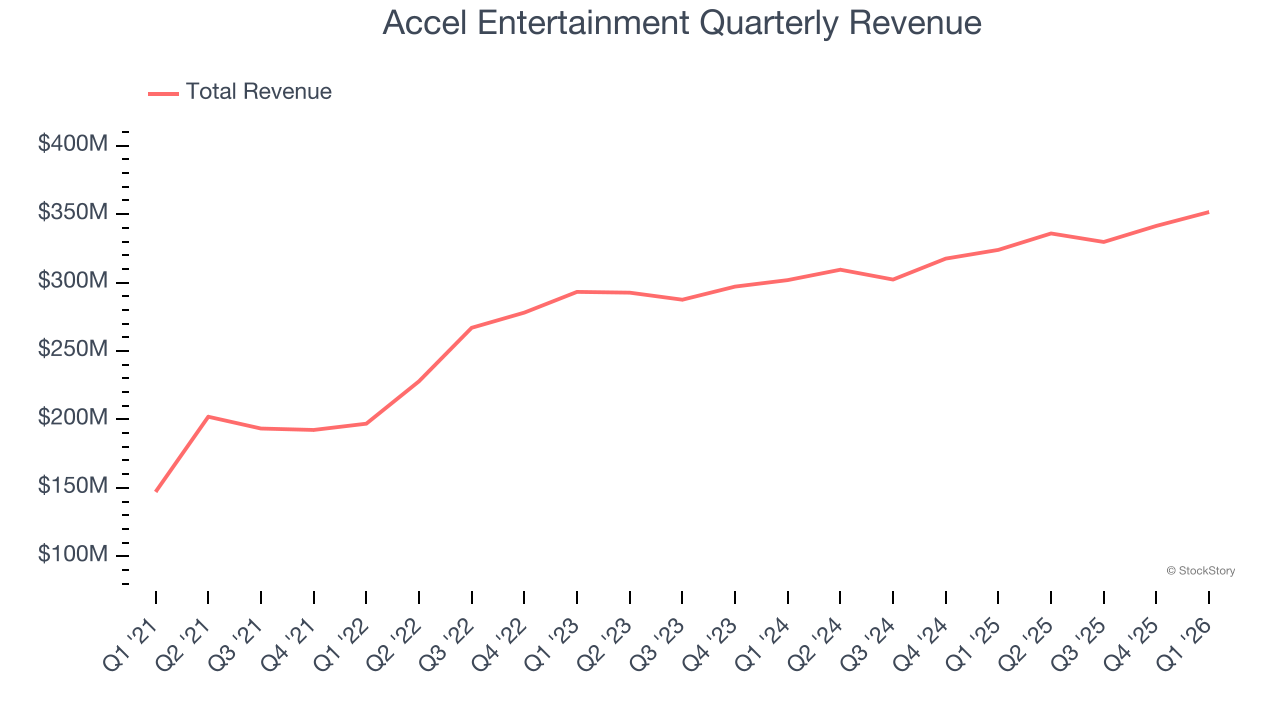

Slot machine and terminal operator Accel Entertainment (NYSE:ACEL) announced better-than-expected revenue in Q1 CY2026, with sales up 8.5% year on year to $351.6 million. Its GAAP profit of $0.17 per share was 6.6% below analysts’ consensus estimates.

Is now the time to buy Accel Entertainment? Find out by accessing our full research report, it’s free.

Accel Entertainment (ACEL) Q1 CY2026 Highlights:

- Revenue: $351.6 million vs analyst estimates of $343.7 million (8.5% year-on-year growth, 2.3% beat)

- EPS (GAAP): $0.17 vs analyst expectations of $0.18 (6.6% miss)

- Adjusted EBITDA: $53.76 million vs analyst estimates of $53.62 million (15.3% margin, in line)

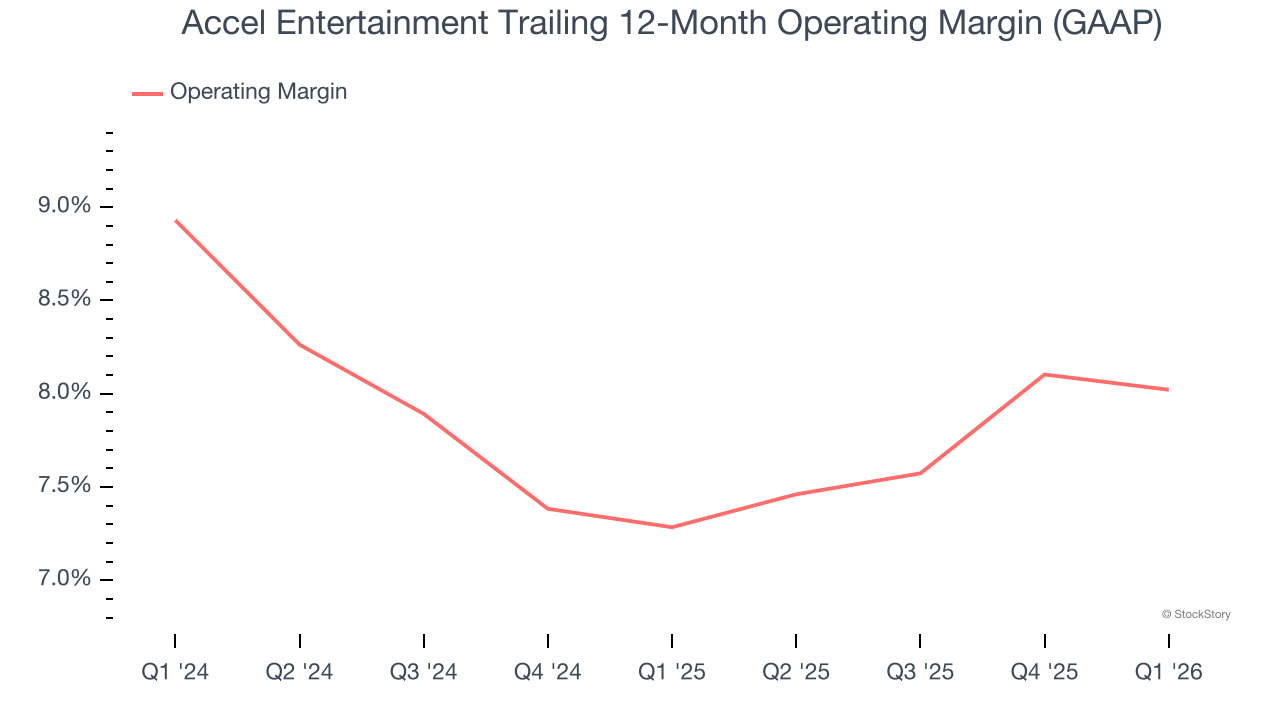

- Operating Margin: 7.7%, in line with the same quarter last year

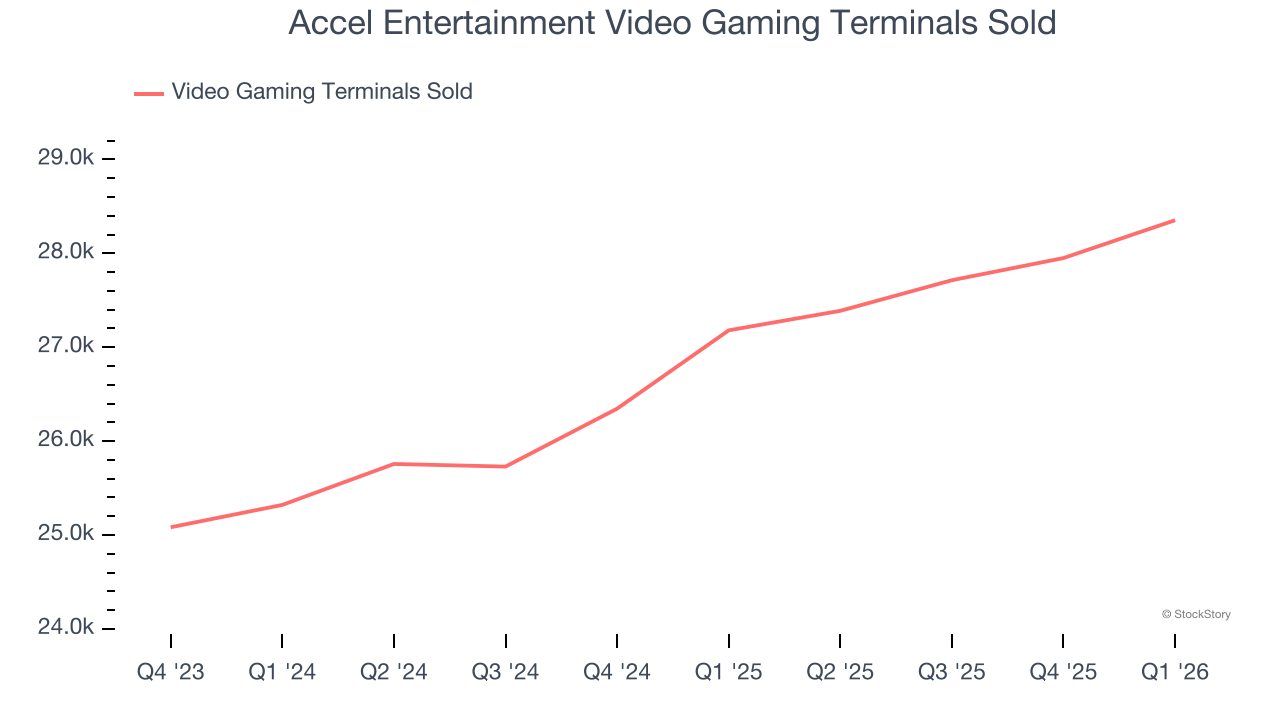

- Video Gaming Terminals Sold: up 1,173 year on year

- Market Capitalization: $996 million

Company Overview

Established in Illinois, Accel Entertainment (NYSE:ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

Revenue Growth

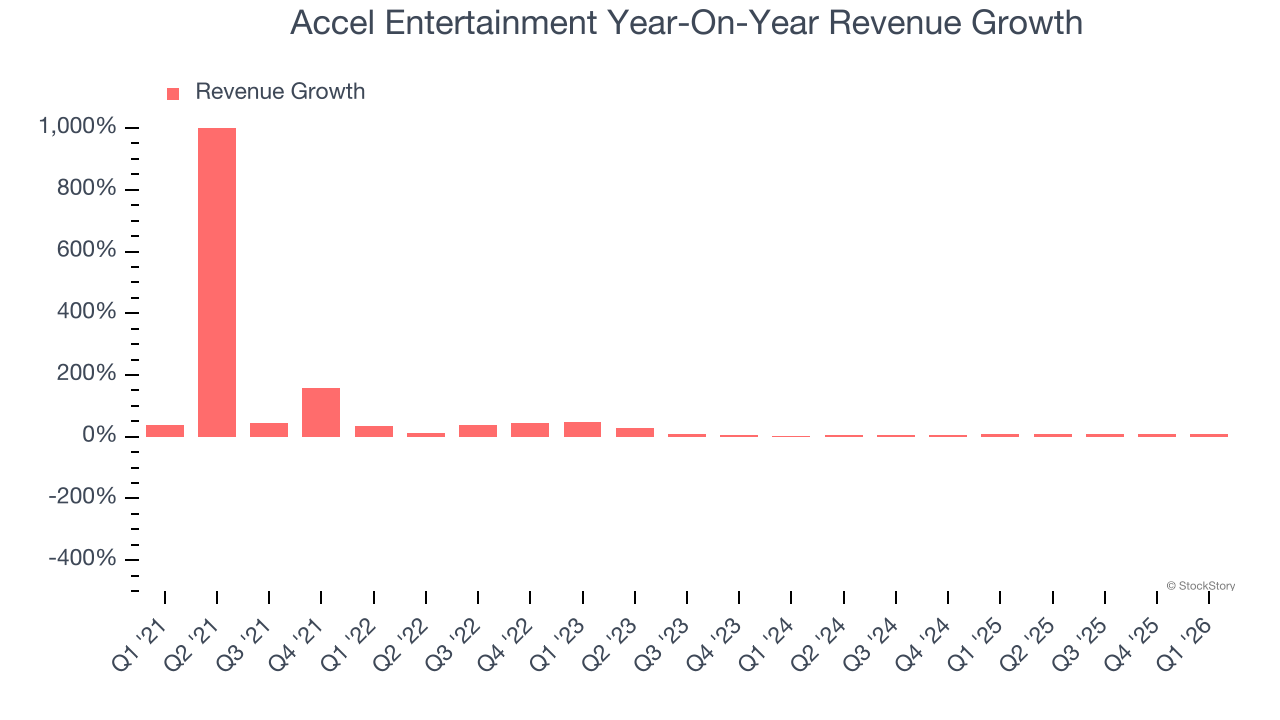

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Accel Entertainment grew its sales at a 30.6% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Accel Entertainment’s recent performance shows its demand has slowed as its annualized revenue growth of 7.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Accel Entertainment also discloses its number of video gaming terminals sold, which reached 28,353 in the latest quarter. Over the last two years, Accel Entertainment’s video gaming terminals sold averaged 6.1% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Accel Entertainment reported year-on-year revenue growth of 8.5%, and its $351.6 million of revenue exceeded Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Accel Entertainment’s operating margin has more or less stayed the same over the last 12 months , and we generally like to see margin increases due to economies of scale and cost efficiency over time.

This quarter, Accel Entertainment generated an operating margin profit margin of 7.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

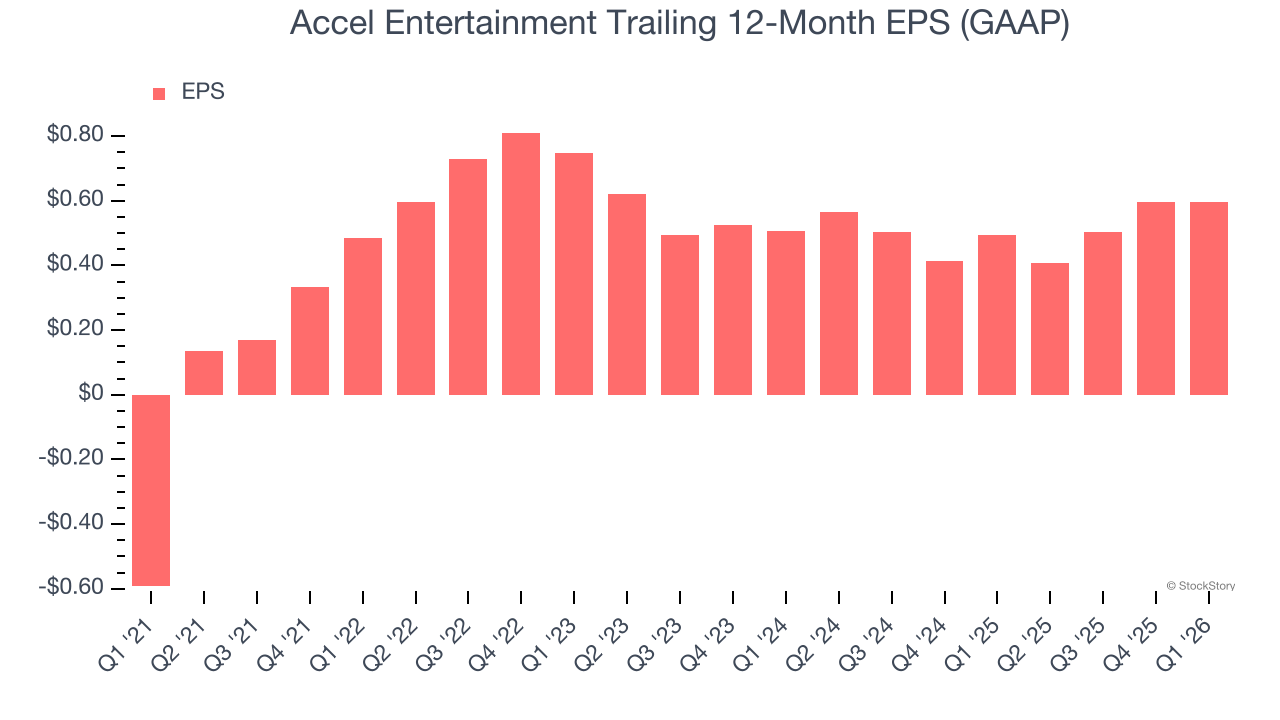

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Accel Entertainment’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Accel Entertainment reported EPS of $0.17, in line with the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Accel Entertainment’s full-year EPS of $0.60 to grow 26.2%.

Key Takeaways from Accel Entertainment’s Q1 Results

It was encouraging to see Accel Entertainment beat analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its adjusted operating income fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.4% to $12.29 immediately after reporting.

Accel Entertainment’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).