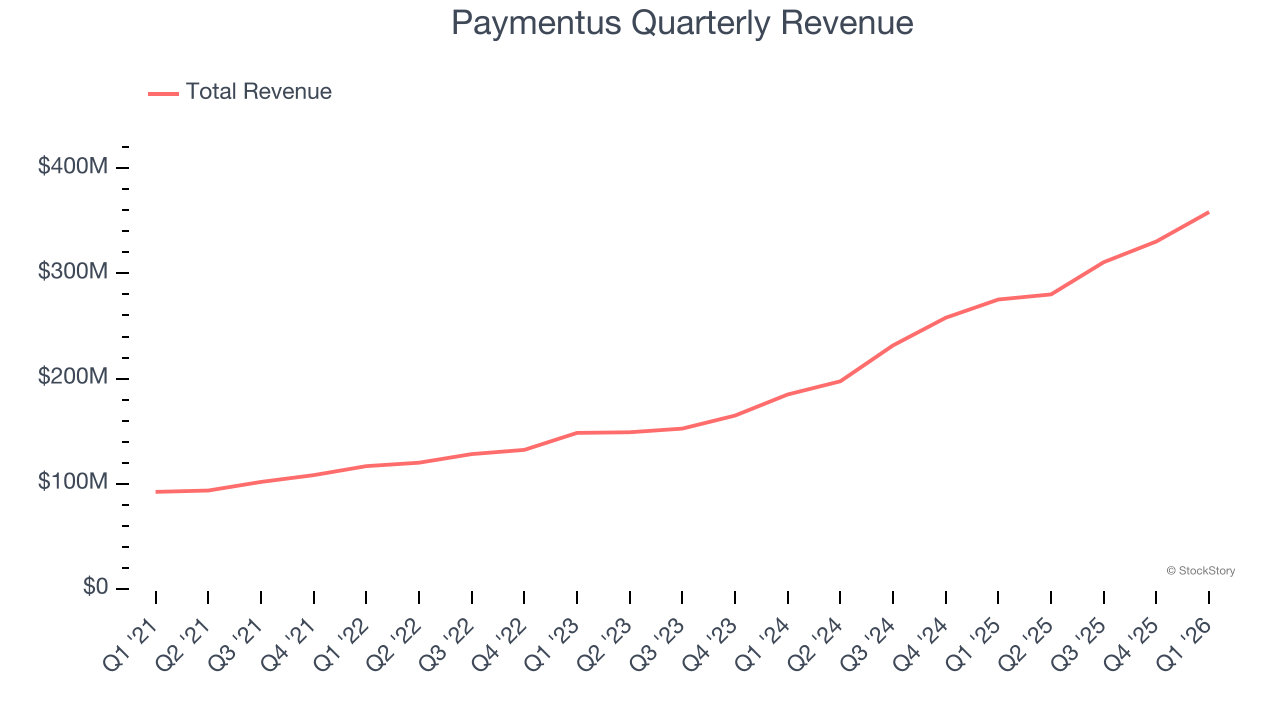

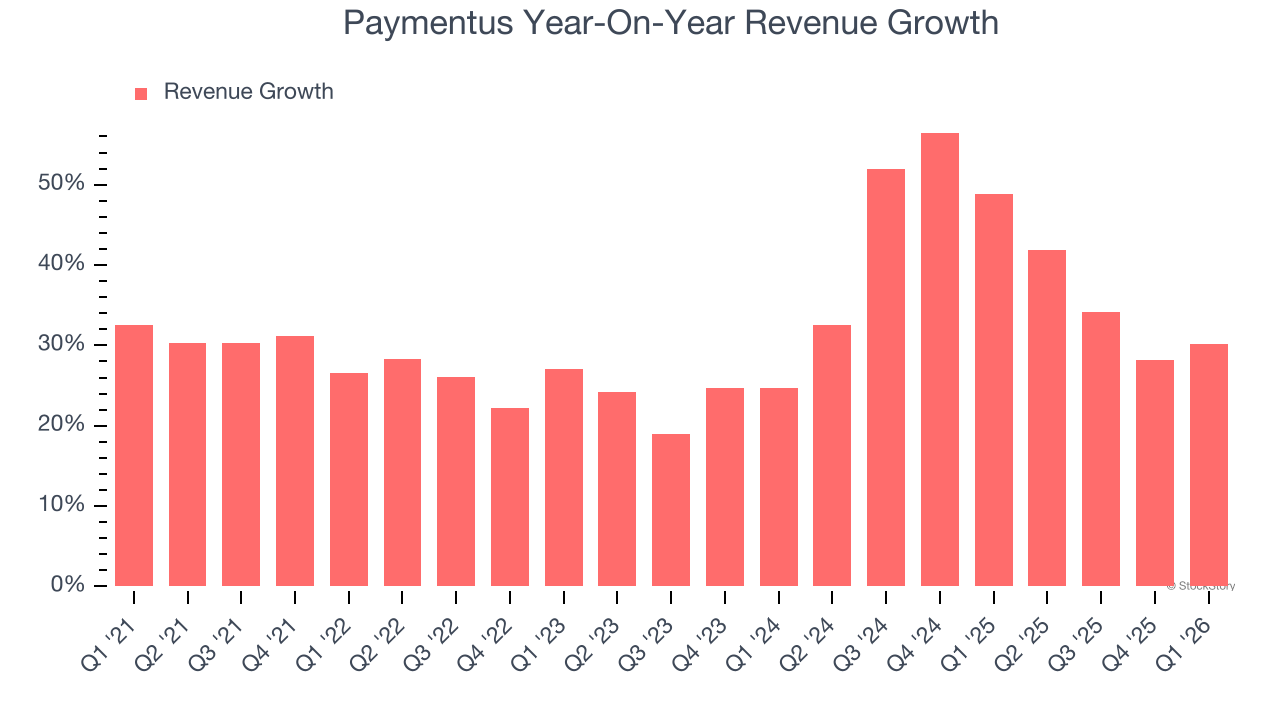

Digital payment platform Paymentus (NYSE:PAY) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 30.2% year on year to $358.4 million. On top of that, next quarter’s revenue guidance ($345 million at the midpoint) was surprisingly good and 3.3% above what analysts were expecting. Its non-GAAP profit of $0.21 per share was 19.8% above analysts’ consensus estimates.

Is now the time to buy Paymentus? Find out by accessing our full research report, it’s free.

Paymentus (PAY) Q1 CY2026 Highlights:

- Revenue: $358.4 million vs analyst estimates of $336.9 million (30.2% year-on-year growth, 6.4% beat)

- Pre-tax Profit: $29.09 million (8.1% margin)

- Adjusted EPS: $0.21 vs analyst estimates of $0.18 (19.8% beat)

- The company lifted its revenue guidance for the full year to $1.43 billion at the midpoint from $1.4 billion, a 2.3% increase

- Market Capitalization: $3.49 billion

“Paymentus had a very strong start to 2026 with record revenue in the first quarter up 30.2% year-over-year, reflecting increased billers and transactions. This helped drive contribution profit growth and adjusted EBITDA growth of 25.2% and 41.5% year-over-year, respectively. These results, combined with our strong bookings and backlog at quarter-end, support our positive outlook for 2026 and beyond,” said Dushyant Sharma, Founder and CEO.

Company Overview

Founded in 2004 to simplify the complex world of bill payments, Paymentus (NYSE:PAY) provides a cloud-based platform that helps utilities, municipalities, and service providers automate billing and payment processes.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Paymentus’s 31.6% annualized revenue growth over the last five years was incredible. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Paymentus’s annualized revenue growth of 40.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Paymentus reported wonderful year-on-year revenue growth of 30.2%, and its $358.4 million of revenue exceeded Wall Street’s estimates by 6.4%. Company management is currently guiding for a 23.2% year-on-year increase in sales next quarter.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Key Takeaways from Paymentus’s Q1 Results

We were impressed by how significantly Paymentus blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 5.6% to $30.25 immediately after reporting.

Paymentus put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).