SunOpta has had an impressive run over the past six months as its shares have beaten the S&P 500 by 20.2%. The stock now trades at $6.49, marking a 24.3% gain. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy SunOpta, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think SunOpta Will Underperform?

We’re glad investors have benefited from the price increase, but we don't have much confidence in SunOpta. Here are three reasons you should be careful with STKL and a stock we'd rather own.

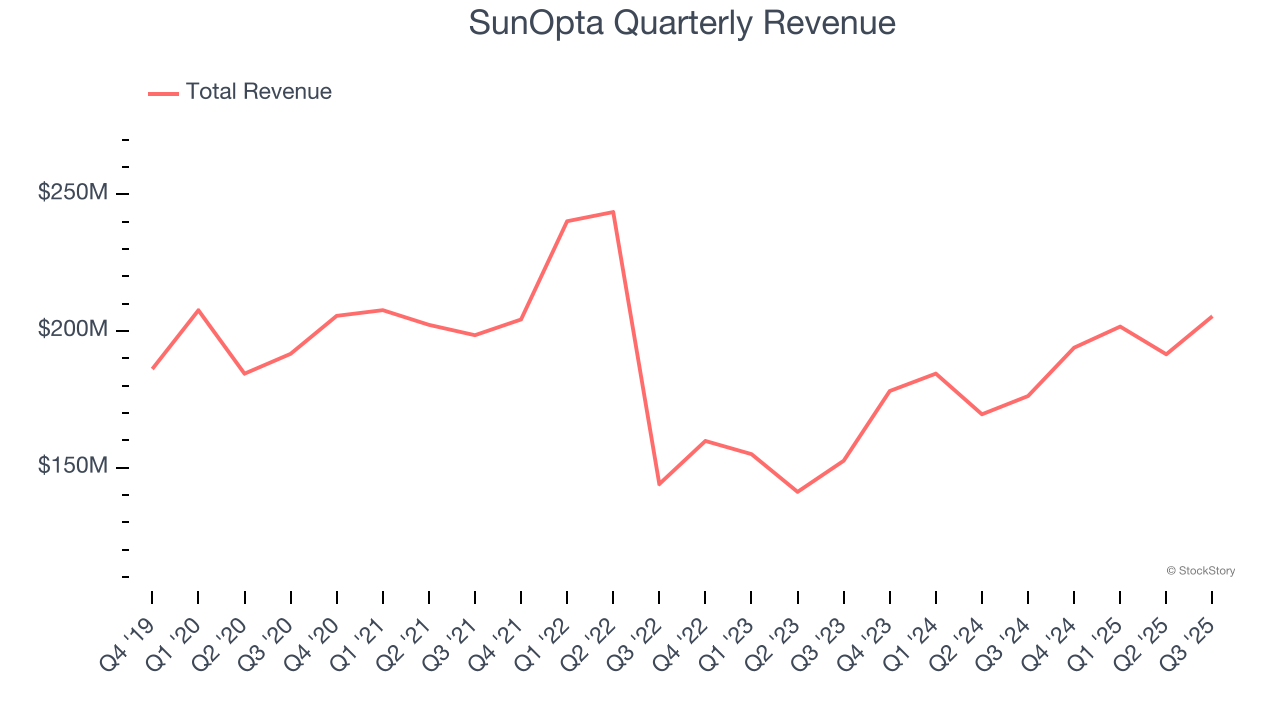

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, SunOpta’s demand was weak and its revenue declined by 1.6% per year. This wasn’t a great result and is a sign of poor business quality.

2. Fewer Distribution Channels Limit its Ceiling

With $792.4 million in revenue over the past 12 months, SunOpta is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

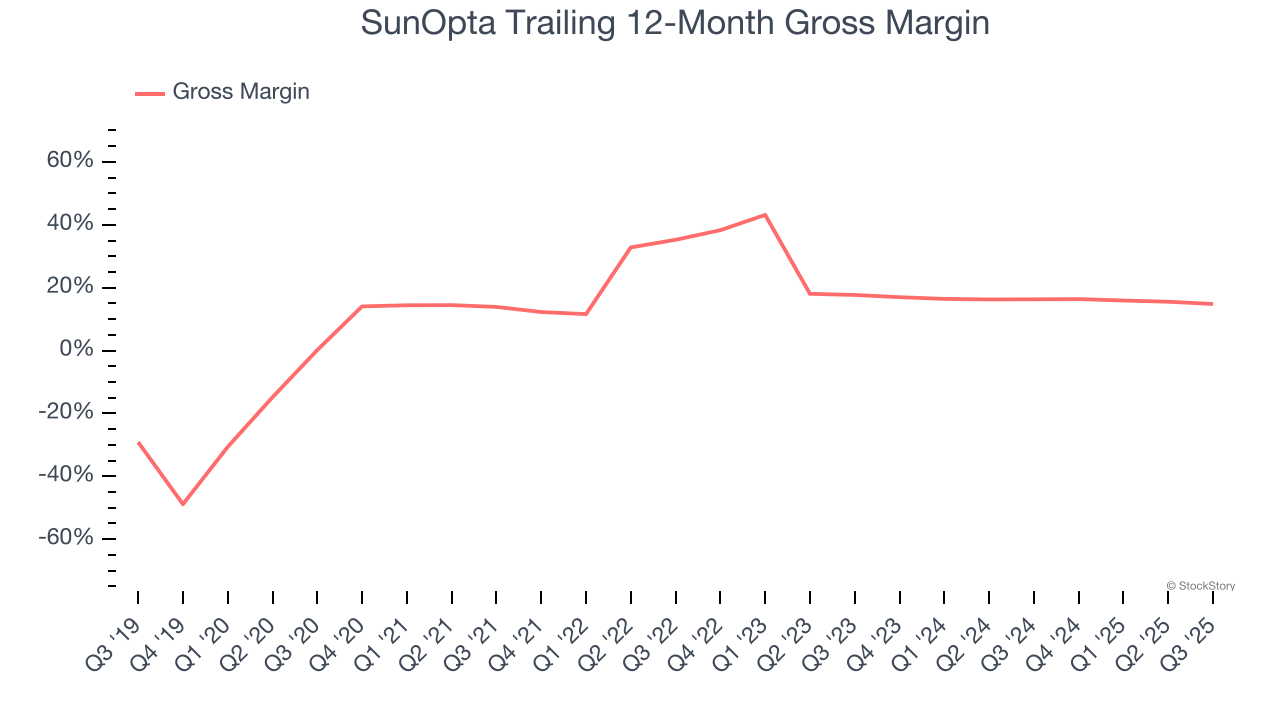

3. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

SunOpta has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 15.5% gross margin over the last two years. Said differently, for every $100 in revenue, a chunky $84.48 went towards paying for raw materials, production of goods, transportation, and distribution.

Final Judgment

SunOpta doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 36.5× forward P/E (or $6.49 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of SunOpta

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.