Wrapping up Q4 earnings, we look at the numbers and key takeaways for the e-commerce software stocks, including Commerce (NASDAQ:CMRC) and its peers.

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

The 4 e-commerce software stocks we track reported a mixed Q4. As a group, revenues along with next quarter’s revenue guidance were in line with analysts’ consensus estimates.

In light of this news, share prices of the companies have held steady as they are up 1.6% on average since the latest earnings results.

Weakest Q4: Commerce (NASDAQ:CMRC)

As a founding member of the MACH Alliance advocating for modern tech standards, Commerce (NASDAQ:CMRC) provides a SaaS platform that enables businesses to build and manage online stores, connect with marketplaces, and integrate with point-of-sale systems.

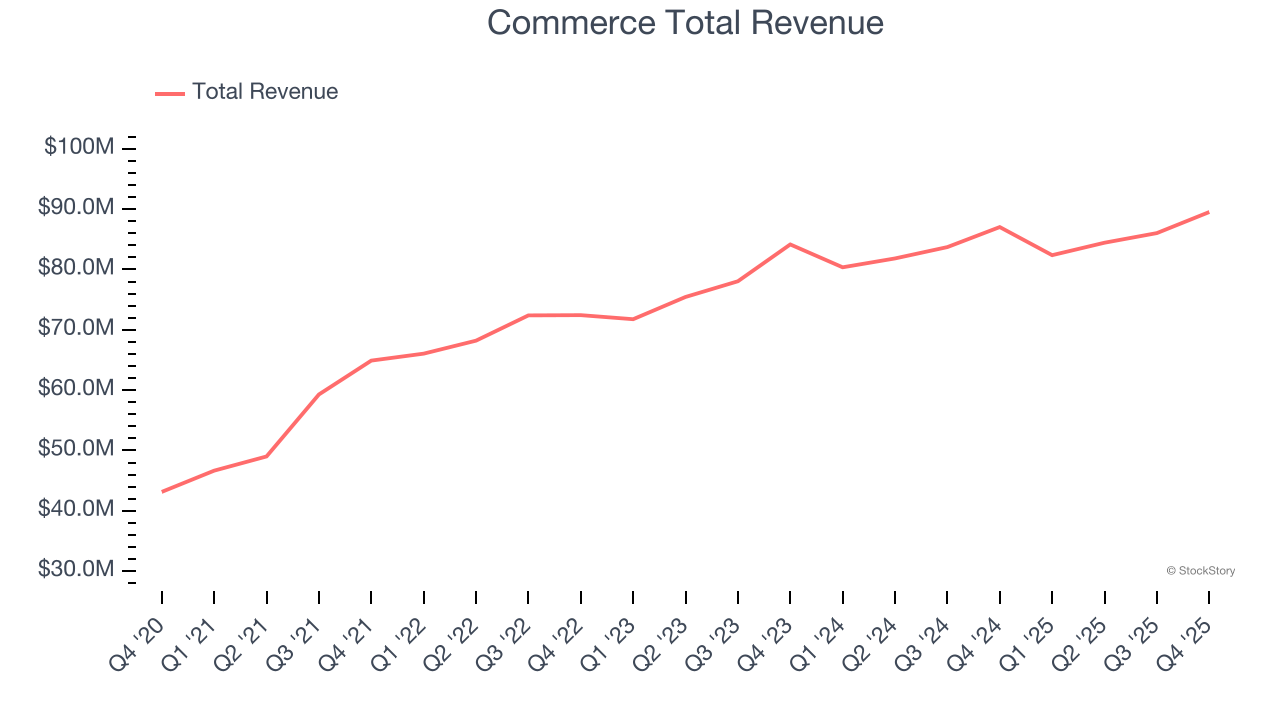

Commerce reported revenues of $89.52 million, up 2.9% year on year. This print fell short of analysts’ expectations by 0.8%. Overall, it was a slower quarter for the company with revenue guidance for next quarter missing analysts’ expectations significantly and a slight miss of analysts’ revenue estimates.

“2025 was a year of material business transformation. We improved efficiency, expanded margins, and realigned investment to our highest-impact growth areas, culminating in our rebrand as Commerce and a clear position in AI-powered agentic commerce,” said Travis Hess, CEO of Commerce.

Commerce pulled off the highest full-year guidance raise but had the weakest performance against analyst estimates and weakest performance against analyst estimates of the whole group. Still, the market seems discontent with the results. The stock is down 3.7% since reporting and currently trades at $2.71.

Read our full report on Commerce here, it’s free.

Best Q4: Shopify (NASDAQ:SHOP)

Starting with just three people selling snowboards online in 2004, Shopify (NYSE:SHOP) provides a comprehensive platform that enables merchants of all sizes to create, manage and grow their businesses across multiple sales channels.

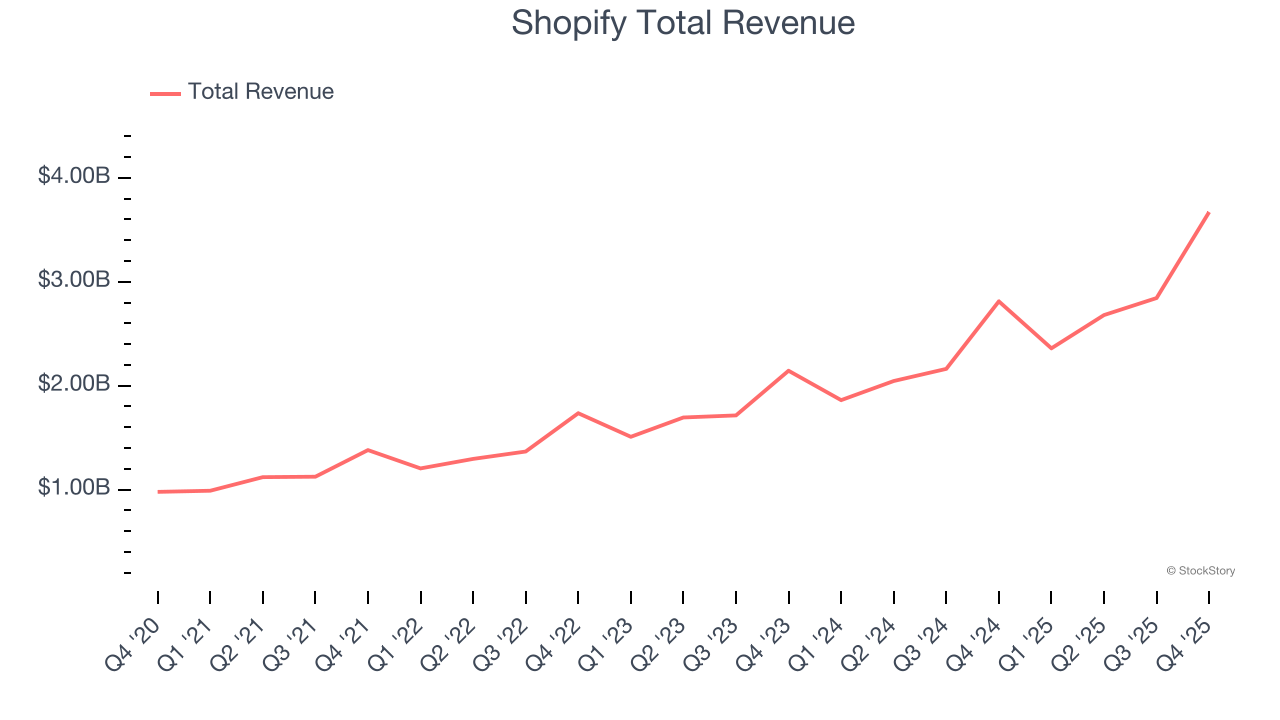

Shopify reported revenues of $3.67 billion, up 30.6% year on year, outperforming analysts’ expectations by 2%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ gross merchandise volume estimates.

Shopify achieved the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 3.7% since reporting. It currently trades at $122.57.

Is now the time to buy Shopify? Access our full analysis of the earnings results here, it’s free.

GoDaddy (NYSE:GDDY)

Known for its memorable Super Bowl commercials that put it on the map, GoDaddy (NYSE:GDDY) is a domain registrar and web services provider that helps entrepreneurs establish an online presence through domain registration, website building, hosting, and e-commerce tools.

GoDaddy reported revenues of $1.27 billion, up 6.8% year on year, in line with analysts’ expectations. It was a slower quarter as it posted revenue guidance for next quarter slightly missing analysts’ expectations and full-year revenue guidance slightly missing analysts’ expectations.

GoDaddy delivered the weakest full-year guidance update in the group. The company added 9,000 customers to reach a total of 20.42 million. As expected, the stock is down 9.3% since the results and currently trades at $83.76.

Read our full analysis of GoDaddy’s results here.

Wix (NASDAQ:WIX)

Powering over 263 million registered users worldwide with its AI-driven tools, Wix (NASDAQ:WIX) provides a cloud-based platform that helps individuals and businesses create and manage professional websites without requiring coding skills.

Wix reported revenues of $524.3 million, up 13.9% year on year. This print was in line with analysts’ expectations. Aside from that, it was a mixed quarter as it also recorded a solid beat of analysts’ EBITDA estimates but revenue in line with analysts’ estimates.

The stock is up 20.6% since reporting and currently trades at $89.69.

Read our full, actionable report on Wix here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.