Wrapping up Q4 earnings, we look at the numbers and key takeaways for the waste management stocks, including Montrose (NYSE:MEG) and its peers.

Waste management companies can possess licenses permitting them to handle hazardous materials. Furthermore, many services are performed through contracts and statutorily mandated, non-discretionary, or recurring, leading to more predictable revenue streams. However, regulation can be a headwind, rendering existing services obsolete or forcing companies to invest precious capital to comply with new, more environmentally-friendly rules. Lastly, waste management companies are at the whim of economic cycles. Interest rates, for example, can greatly impact industrial production or commercial projects that create waste and byproducts.

The 8 waste management stocks we track reported a mixed Q4. As a group, revenues were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 7.6% since the latest earnings results.

Montrose (NYSE:MEG)

Founded to protect a tree-lined two-lane road, Montrose (NYSE:MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

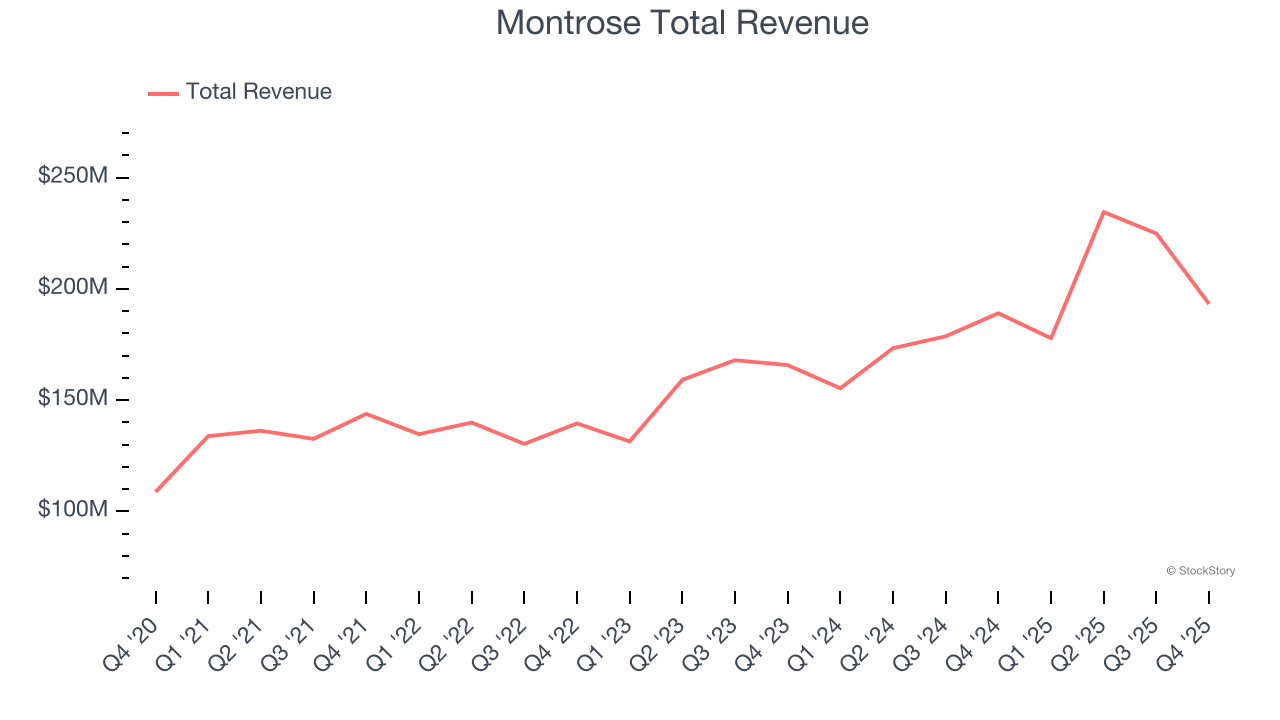

Montrose reported revenues of $193.3 million, up 2.2% year on year. This print exceeded analysts’ expectations by 2.5%. Overall, it was an exceptional quarter for the company with a beat of analysts’ EPS and adjusted operating income estimates.

Montrose Chief Executive Officer and Director, Vijay Manthripragada, commented, “Over a year ago, we announced a pause in acquisitions to highlight the quality and durability of our business. We also shared our expectation that US regulatory volatility would create more tailwinds than headwinds given our unique business model and global client focus. As we reflect on our focused execution in 2025, our business outperformed and exceeded every major objective. We delivered 13% organic revenue growth, expanded EBITDA margins, and generated record cash flow with 75% Free cash flow1 conversion. Our cash flow generation outperformance resulted in 2025 year-end leverage approximately 0.5x lower than our forecast at the start of 2025. We also accelerated cross-selling across our platform, expanded our IP portfolio, and attracted incredible talent, all of which position us very well for 2026 and beyond."

Unsurprisingly, the stock is down 4.1% since reporting and currently trades at $22.42.

We think Montrose is a good business, but is it a buy today? Read our full report here, it’s free.

Best Q4: Enviri (NYSE:NVRI)

Cooling America’s first indoor ice rink in the 19th century, Enviri (NYSE:NVRI) offers steel and waste handling services.

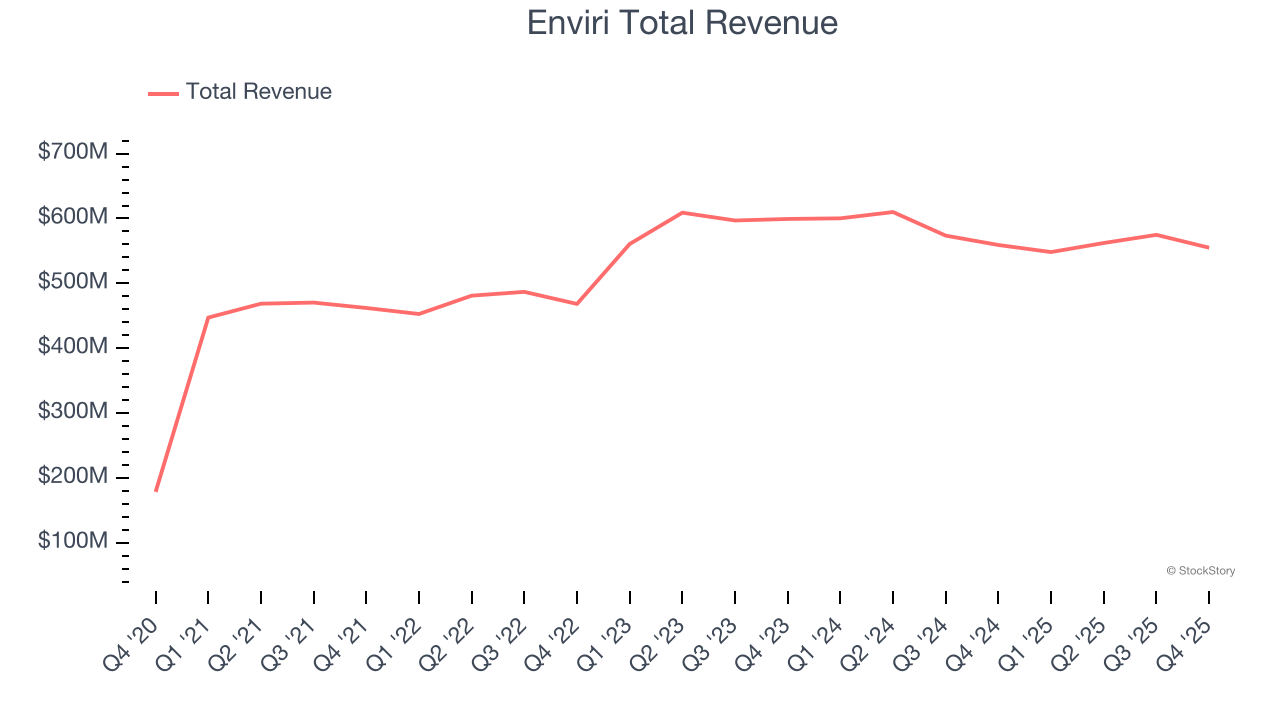

Enviri reported revenues of $555 million, flat year on year, outperforming analysts’ expectations by 0.7%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.6% since reporting. It currently trades at $18.24.

Is now the time to buy Enviri? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Quest Resource (NASDAQ:QRHC)

Recycling corporate waste to help companies be more sustainable, Quest Resource (NASDAQ:QRHC) is a provider of waste and recycling services.

Quest Resource reported revenues of $58.91 million, down 15.8% year on year, falling short of analysts’ expectations by 3.8%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Quest Resource delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 41.2% since the results and currently trades at $0.85.

Read our full analysis of Quest Resource’s results here.

Casella Waste Systems (NASDAQ:CWST)

Starting with the founder picking up garbage with a pickup truck he purchased using savings from high school, Casella (NASDAQ:CWST) offers waste management services for businesses, residents, and the government.

Casella Waste Systems reported revenues of $469.1 million, up 9.7% year on year. This number was in line with analysts’ expectations. Aside from that, it was a slower quarter as it recorded a significant miss of analysts’ adjusted operating income estimates and a miss of analysts’ EBITDA estimates.

Casella Waste Systems scored the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is down 16.8% since reporting and currently trades at $84.22.

Read our full, actionable report on Casella Waste Systems here, it’s free.

Waste Management (NYSE:WM)

Headquartered in Houston, Waste Management (NYSE:WM) is a provider of comprehensive waste management services in North America.

Waste Management reported revenues of $6.31 billion, up 7.1% year on year. This result lagged analysts' expectations by 1.3%. It was a slower quarter as it also logged a slight miss of analysts’ revenue and adjusted operating income estimates.

Waste Management delivered the highest full-year guidance raise among its peers. The stock is up 1.2% since reporting and currently trades at $234.37.

Read our full, actionable report on Waste Management here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.