Steve Eisman is a businessman and investor who shorted collateralized debt obligations (CDOs) during the Great Recession and profited significantly from it. He has remained active in the stock market and manages a portfolio, which is now shorting a specific software stock.

His short position is not in Palantir (PLTR) or Microsoft (MSFT), but a more specialized software firm called Fair Isaac Corp. (FICO). You're likely aware of "FICO scores," and this comes from Fair Isaac's credit scoring.

You may wonder why Eisman is betting against such a well-established and well-embedded company. And for that, we do have to look a bit deeper.

FICO Isn't Your Run-of-the-Mill Software Company

FICO scores are used in 90% of U.S. consumer lending decisions, and each time lenders pull those scores, the company earns a fee. Thus, it has enormous pricing power. Lenders can't really switch credit rating scores without sacrificing coverage and reliability, and paying Fair Isaac is a much better deal than having non-performing loans.

But competition might catch up soon, and that's why many investors are reevaluating Fair Isaac's pricing power. In April 2026, FHFA said Fannie Mae (FNMA) and Freddie Mac (FMCC) were updating their selling guides to move forward with VantageScore 4.0 and FICO Score 10T and would immediately accept VantageScore loans from approved lenders, while FHA said it would also permit VantageScore 4.0 and FICO 10T for FHA-insured mortgage underwriting.

The incumbent system is still here, though it will likely lose its edge if more lenders start opening up to alternatives.

Why Eisman is Bearish

He is not broadly bearish on the market and probably not even on software. However, he is going after FICO because the company "very arrogantly" raised prices by about 500% over many years and “ticked off literally everybody in the lending world.”

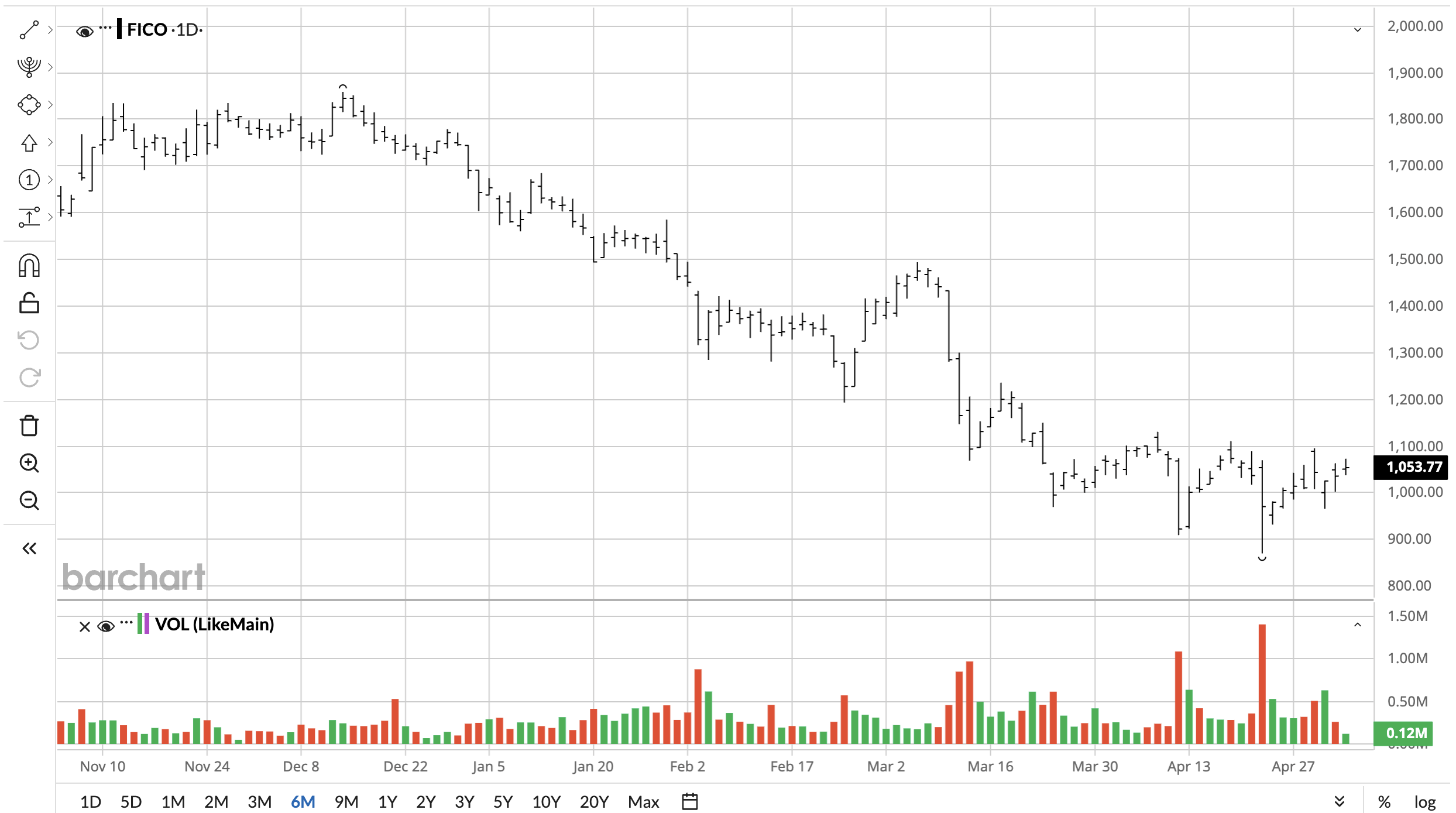

Fair Isaac's management used the pricing power they had a little too much. This did have a good impact on the business, with the stock climbing over 500% from December 2021 to its peak in November 2024. FICO stock has fallen by over 55% since then due to fears that customers were eventually going to come up with a solution to this.

Eisman pointed out that lenders need to pay about $2,000 to FICO for every 100 mortgage applications, while VantageScore would cost $99.

Eisman Is Going Against the Grain

FICO stock has fallen massively, but this is mostly due to fear and overvaluation. Continuing to short this stock right now means you are putting yourself in the line of fire if this business keeps doing well. Fair Isaac reported a strong fiscal Q2 2026, with revenue of $692 million, up 39% year-over-year (YoY), and it raised full-year guidance. EPS came in at $12.50 and beat expectations of $11.03. Any other business with these metrics would've kept on climbing higher, but the sheer amount of fear surrounding Fair Isaac has instead caused it to continue sliding.

Eisman is calling time on one of the fattest pricing franchises in lending, and he's arguing that FICO spent years squeezing customers. Washington’s long-delayed move to allow real competition in mortgage credit scores may finally give those customers a way to hit back.

What You Can Do With FICO Stock

Eisman has been in the lending world for decades, and he's right that Fair Isaac has indeed "ticked off" people in lending. That said, what he's arguing is not as simple. But again, he's short, and people will say what they need to to make their positions pay off.

For example, his $2,000 vs. $99 figure is technically true and substantively beside the point. The actual cost driver in mortgage origination is the tri-merge credit report bundle, which the Community Home Lenders of America recently pegged at around $540 per file, up sharply from a few years ago.

The score itself is maybe four percent of that stack. So when Eisman waves around the 95% savings, he's talking about the smallest line item in the file. A lender switching from FICO to VantageScore on every application saves roughly $19 per loan on a closing cost number that runs into the tens of thousands. That is real money on a million-loan book and exactly zero motivation for any single loan officer to rip out their underwriting system.

I'd argue that lenders are not ticked off enough yet, and the stock has already taken the beating it deserves. In fact, it is near the lowest analyst price target.

I wouldn't short such a beaten-down stock. You should avoid shorting a highly profitable and fast-growing company unless you absolutely know what you are doing, so I'd either go long on FICO or not touch it at all.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Shopify's Strong Q1 FCF Growth Sparks Unusual Buying of SHOP Calls

- Ignore the Amazon Trucking Noise and Buy UPS Stock for Its High Yield Near 7%

- The Amazon Most Investors Knew No Longer Exists

- Universal Logistics Stock Plunged on Amazon’s Trucking News. Its 3.4% Dividend Could Make the Dip Worth Buying.