Cost-cutting and restructuring moves are nothing new on Wall Street. When companies face slowing growth or shifting consumer trends, trimming the workforce and tightening operations often become key levers to protect margins and reignite profitability. Investors tend to welcome these actions, especially when they signal a more disciplined path forward.

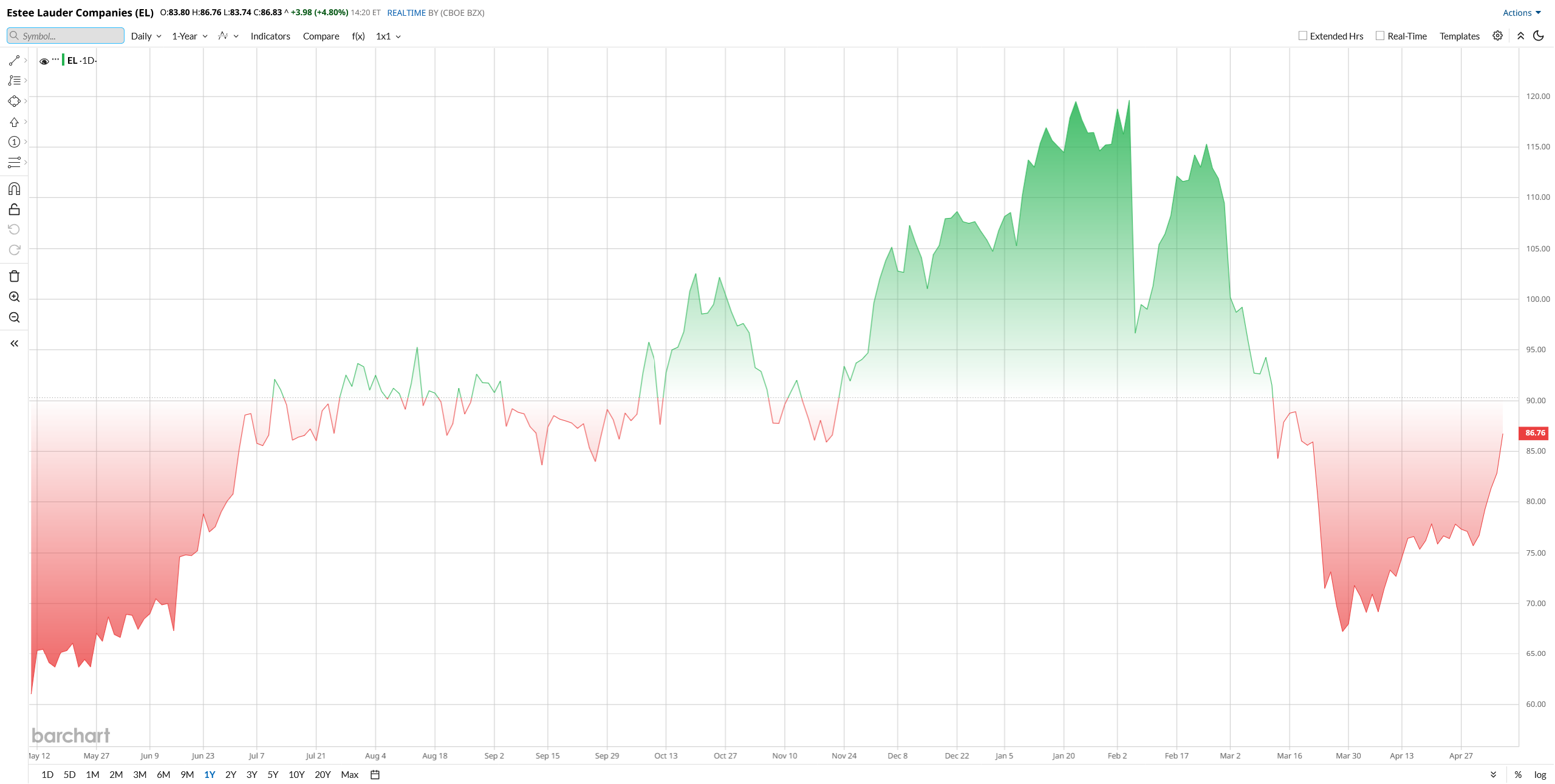

That’s precisely what’s happening with Estée Lauder Companies (EL). The beauty giant recently grabbed headlines after announcing plans to cut up to 3,000 additional jobs as part of a broader restructuring effort, bringing total expected layoffs to as many as 10,000 roles. The move, alongside a raised profit outlook, sent EL stock sharply higher, with shares jumping about 11% in premarket trading and another 5% during today's trading session.

For investors betting on a turnaround in the premium beauty space, here’s a closer look at why this aggressive restructuring push could be a pivotal moment for Estée Lauder stock.

How Did EL Stock Perform?

Estée Lauder Companies is not some niche player. This is the company behind Clinique, M.A.C., La Mer, Tom Ford, Aveda, and The Ordinary. It employs roughly 57,000 people around the world. When a company this size starts swinging the axe, Wall Street pays attention.

Recently, the company announced a full acquisition of Forest Essentials, India’s leading prestige skincare brand. It also made a minority investment in the luxury brand 111Skin. Meanwhile, the ongoing talks to merge with Spanish beauty giant Puig continue to simmer in the background.

A deal is not done, but the prospect alone adds a layer of intrigue. De La Faverie is also pushing hard into digital, forging partnerships with Amazon (AMZN) Premium Beauty, TikTok Shop, Shopify, and WPP.

The past year has been anything but boring for EL shareholders. The stock has climbed about 48% over the trailing 12 months. Year-to-date (YTD) in 2026, however, it had been down as much as 30% as of now. Investors got spooked after the February update, worried that capital spending was creeping higher just as the top-line recovery still looked fragile. Even after a solid Q1 beat, the market fixated on the capex outlook and sold the news. Then came last week’s layoff announcement, and the mood flipped fast.

After the recent bounce, Estée Lauder trades at a forward price-to-earnings multiple of around 26 times. That is roughly in line with the personal products sector median. The price-to-sales ratio sits near 2, which is also middle-of-the-pack. By these two metrics, EL does not scream cheap, but it no longer looks wildly expensive either. The market seems to be pricing in a turnaround that is still very much in progress.

The Layoff News That Changed the Narrative

On May 1, Estée Lauder Companies dropped big news that the company is expanding its restructuring program and now plans to eliminate between 9,000 and 10,000 jobs. That is up from a previous target of 7,000.

At the high end, it represents about 17.5% of the global workforce. Over 70% of the additional cuts will hit department store beauty advisors. Management is clearly betting that the future lies in digital channels like Amazon and TikTok Shop, not in the traditional cosmetics counter. Investors cheered the news.

The stock jumped as much as 10% following the news and is up almost 5% during trading today.

What the Latest Quarterly Numbers Tell Us

EL's latest quarter results gave investors plenty to chew on. Revenue came in at $3.71 billion, up 5% from a year ago and ahead of Wall Street estimates. Organic sales growth clocked in at 2%.

Skin care, the company’s biggest division, brought in $1.86 billion. That was a 3% increase year-over-year (YoY). The Estée Lauder brand showed some spark, though Clinique and Too Faced remained soft spots.

Here is where the story gets interesting. Adjusted earnings per share hit $0.91. That crushed the $0.65 analysts were expecting and marked a 40% jump from the same quarter last year. Gross margin expanded to 76.4%, up 140 basis points. Those are meaningful improvements.

Additionally, free cash flow for the trailing 12 months stood at $1.81 billion. Total cash on the balance sheet was $3.13 billion. That is a healthy cushion.

CEO Stéphane de La Faverie called fiscal 2026 a pivotal year and said the company is executing its Beauty Reimagined strategy with focus, discipline, and speed. He pointed to the expanded restructuring as a way to free up fuel for reinvestment in consumer-facing areas.

Management raised full-year guidance. Adjusted EPS is now expected to land between $2.35 and $2.45, up sharply from the prior range of $2.05 to $2.25. Revenue guidance came in at $14.9 billion, just a hair below the $15 billion consensus. For fiscal 2027, the preliminary outlook calls for 3% to 5% sales growth and operating margins in the 12.5% to 13% range.

Wall Street analysts currently expect full-year revenue of around $15 billion and adjusted EPS of about $2.39. The company’s guidance sits comfortably above those bottom-line estimates.

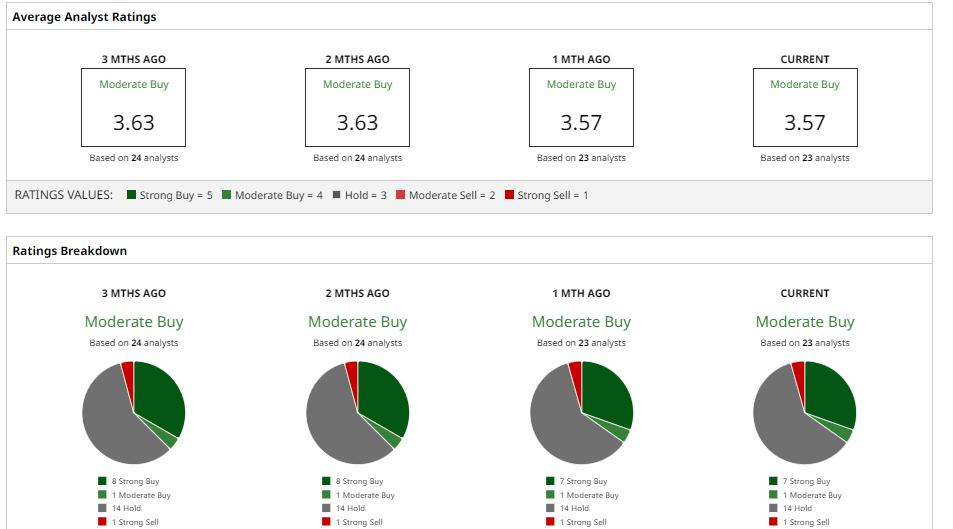

What Does the Analyst Community Think of EL Stock?

Despite the improving picture, Wall Street is not fully convinced yet. Analysts broadly agree that Estée Lauder is moving in the right direction, but they’re still waiting for clearer signs of a sustained recovery.

UBS analyst Peter Grom raised his price target to $85 from $75 while maintaining a "Neutral" rating, noting that progress is visible but not yet fully proven.

B. Riley took a more cautious stance, cutting its target to $85 from $105 and highlighting that expectations for fiscal 2027 remain high, particularly around a recovery in China and travel retail.

Similarly, Telsey Advisory’s Dana Telsey lowered her target to $90 from $105, pointing to geopolitical uncertainty as a potential risk to consumer spending.

Overall, the consensus rating stands at “Moderate Buy,” with an average price target near $92, implying roughly 7% upside from current levels. That suggests cautious optimism, but not outright conviction.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Time to Buy: This Cheap High-Yield Dividend Stock Is Trading Near Multi-Year Lows

- With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock

- Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing.

- The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze