For the past two years, Wall Street has treated artificial intelligence like a land rush. Companies rushed to build data centers, hyperscalers ordered every GPU they could get their hands on, and investors piled into anything connected to AI infrastructure. But here's the question smart investors should be asking now: What happens after the initial buildout phase ends?

That’s where Advanced Micro Devices (AMD) may have just changed the conversation.

Its May 5 earnings report wasn’t simply another beat-and-raise quarter. It was evidence that AMD is becoming a core supplier for the next phase of AI—inference. That’s a fancy way of saying the everyday computing work AI systems perform after they’ve already been trained. And that market could end up far larger than many investors expected.

AMD’s Stock Was Already Winning Before Earnings

Even before earnings, AMD shares had been outrunning much of the market. Its stock was up roughly 65% year-to-date (YTD) entering this week, compared with a gain of about 6% for the benchmark S&P 500 ($SPX) over the same stretch.

That outperformance matters because semiconductor stocks have become brutally competitive. Investors have had no shortage of AI names to choose from, including Nvidia (NVDA), Intel (INTC), Broadcom (AVGO), and Arm Holdings (ARM).

Yet AMD keeps gaining market share.

Mercury Research data cited by Tom’s Hardware showed AMD’s server CPU market share climbed to nearly 29% by the end of 2025. That’s not “scrappy challenger” territory anymore. That’s real scale.

Then came earnings.

AMD reported first-quarter revenue of $10.25 billion, up 38% year-over-year (YoY), while adjusted earnings per share hit $1.37 versus analyst estimates near $1.29. But the real headline sat inside the data center business. Revenue surged 57% to $5.8 billion.

Regardless of how you look at it, that’s the number that changes the AMD story.

The AI Gold Rush Is Moving Into Its Next Phase

Training AI models grabbed the early headlines because companies needed enormous computing power to create systems like ChatGPT. But inference is where recurring demand lives.

Every query. Every chatbot response. Every AI-generated image. Every automated customer service interaction. Those all require compute power every single day. Lisa Su, AMD’s CEO, highlighted that trend directly during the earnings release, saying demand for “inferencing and agentic AI” is accelerating.

Surprisingly, AMD also raised its long-term outlook for the server CPU market dramatically. The company now expects the market to grow more than 35% annually through 2030, versus its previous expectation of closer to 18% annual growth. That’s a massive revision.

In practical terms, AMD now believes the server CPU opportunity could exceed $120 billion by 2030.

And unlike the one-time AI training buildout, inference demand compounds over time. Multi-gigawatt AI infrastructure projects from companies like Meta Platforms (META) and partnerships tied to OpenAI suggest this spending cycle may last far longer than skeptics expected.

In short, AMD is no longer just a “second source” chipmaker standing behind Nvidia. It’s becoming a primary AI infrastructure platform.

AMD’s Valuation Still Carries Risk

Granted, none of this means AMD stock is cheap. Barchart data shows AMD trading around 104 times trailing earnings and roughly 16 times sales. The stock also trades near 62 times forward earnings with a PEG ratio close to 1.3.

That valuation leaves little room for execution mistakes. If enterprise AI spending slows, or if Nvidia widens its lead again, AMD shares could see sharp volatility. Semiconductor cycles rarely move in straight lines.

That said, AMD’s balance sheet remains healthy, with low leverage and rising profitability.

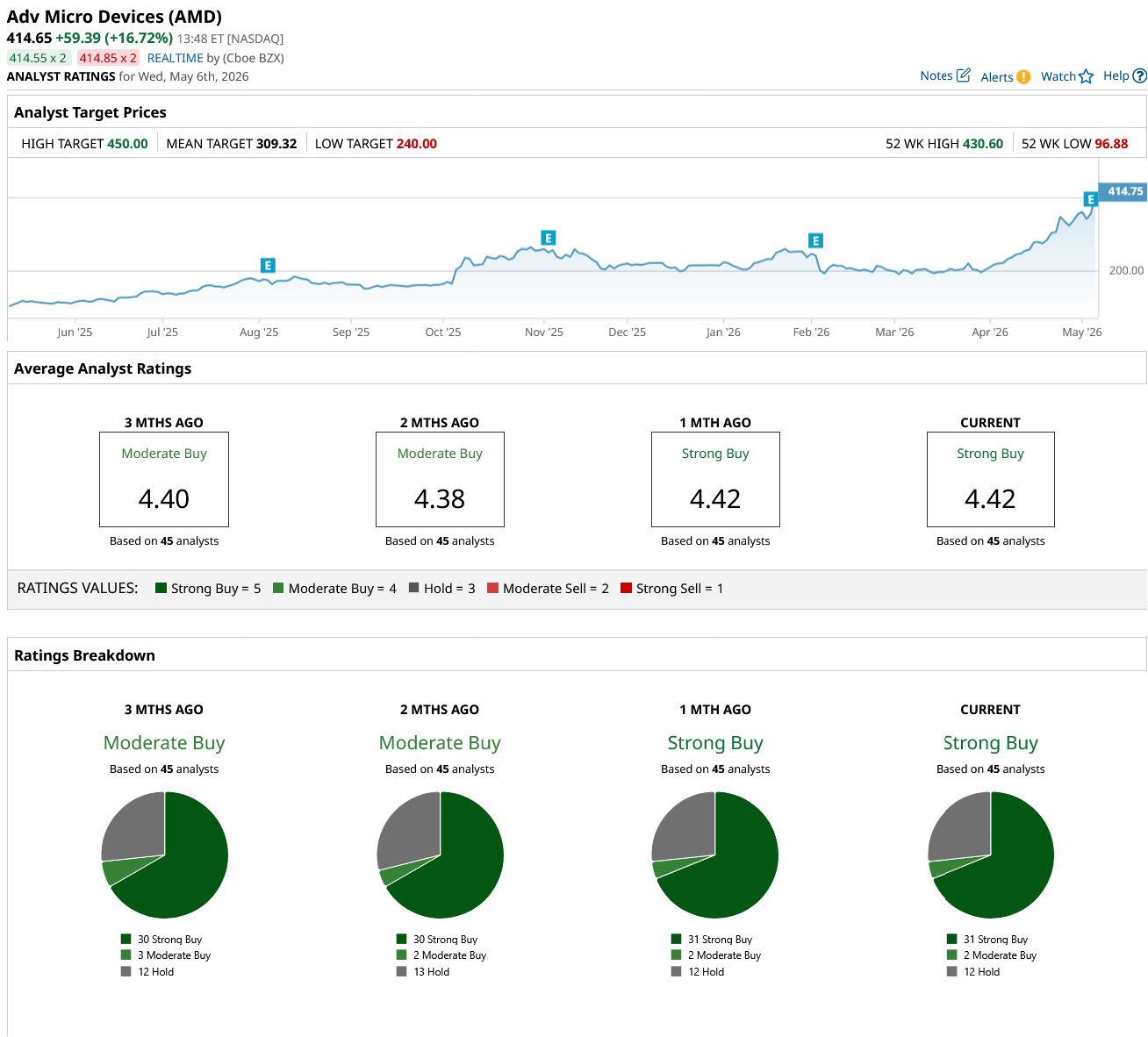

What Analysts Think About AMD Stock

Wall Street remains firmly bullish. Barchart analyst ratings confirm AMD carrying a “Strong Buy” consensus rating based on 45 analysts, with 31 "Strong Buy" ratings, two "Moderate Buy," and 12 "Hold."

Analyst price targets vary widely, which reflects both the opportunity and uncertainty surrounding AI demand. The mean price target is $309.32, with $240 on the low end and $450 on the high side. With AMD shares soaring about 17% by afternoon trading Wednesday, the stock is now fairly valued to slightly overbought, but analysts may quickly raise their targets.

Bottom Line

AMD’s latest earnings report wasn’t just strong. It clarified where the company fits in the AI economy.

The first wave of AI spending was about building models. The next wave is about running them constantly—and that’s where AMD’s server CPU and accelerator business may become a long-term growth engine.

When all is said and done, AMD looks less like a cyclical chip stock and more like a foundational AI infrastructure company. That distinction could matter for years.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Time to Buy: This Cheap High-Yield Dividend Stock Is Trading Near Multi-Year Lows

- With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock

- Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing.

- The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze